ETF Tracker StatSheet

https://theetfbully.com/2018/01/weekly-statsheet-etf-tracker-newsletter-updated-01-11-2018/

MORE RECORDS IN THE BOOKS

- Moving the markets

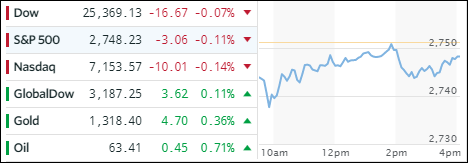

Earnings season unofficially started with a bang, as the major indexes continued their march into uncharted territory with optimism about the upcoming corporate report cards taking center stage. All 3 major indexes spiked again with consumer discretionary and energy shares leading the gains. Looking at the big picture, the S&P 500 had its best start to a year since 1987, while the Dow and Nasdaq had their best start since 1997 and 2004 respectively.

Things looked good in the ETF space I follow with green being the favorite color of the week. Leadership rotated from yesterday with Aerospace & Defense (ITA) gaining +1.54% followed by International SmallCaps (SCHC +1.22%) and International ETFs (SCHF +0.91%). The laggard of the day turned out to be MidCaps (SCHM) with +0.33%.

Interest rates presented a mixed picture with 10-year bond yield rising by 1 basis point, while the 30-year bond yield declined 6 basis points. Gold surged today and has now rallied for 5 straight weeks. Crude Oil bounced higher and the US Dollar (UUP) got spanked hard, gapped down and lost -1.04% to reach a level last seen in September when it made its 2017 low.