ETF Tracker StatSheet

A WILD WEEK, BUT S&P 500 ENDS UNCHANGED

It should come as no surprise that, based on the drubbing of the foreign currency markets, as I detailed yesterday, emerging market equities could not be far behind. That materialized today, as our emerging market ETF holding pierced its trailing sell stop and was liquidated in accordance with our sell stop discipline.

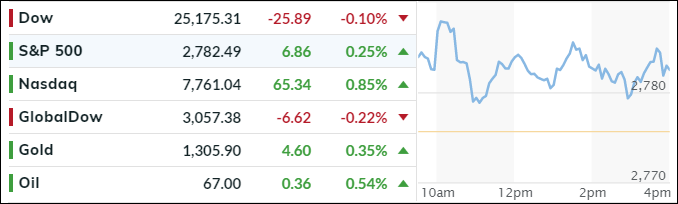

Domestically, the major indexes started in the red, as the U.S.-China trade dialog heated up with tensions escalating, but calmer heads prevailed on Wall Street, and a slow rebound ensued, which ended just short of the unchanged line.

It’s amazing that, despite the chaos not just in FX (Foreign Exchange) but also the debt and commodity arenas, the major indexes held up well with the S&P 500 closing just about even for the week, helped in part by the VIX getting crushed again.

The large banks lost, while the US Dollar had its highest weekly close since July 2017, which was exactly opposite of the Euro, which had its lowest weekly close since July 2017. Not looking too good either was the Commodity Index which, after a stellar YTD performance, was crushed this week. To me, that is just a temporary pullback since inflationary forces will continue to grow and affect the commodity sector positively.

Currently, I see two prevailing opinions regarding market direction. One is held by the smart money, represented in part by some well-known fund managers, who seem to have left equities, as this chart shows. On the other side are those, who are seeing a strong return of inflation and with it racing equity markets ending with a blow-off top sometime later this year.

Of course, along the way, there are a host of Black Swans lurking and waiting for the right moment to make an appearance. Since no one knows how this will end up playing out, we’ll continue to follow the major trends via our TTIs and execute our trailing sell stops when it becomes necessary.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}