ETF Tracker StatSheet

[Chart courtesy of MarketWatch.com]

[Chart courtesy of MarketWatch.com]

- Moving the markets

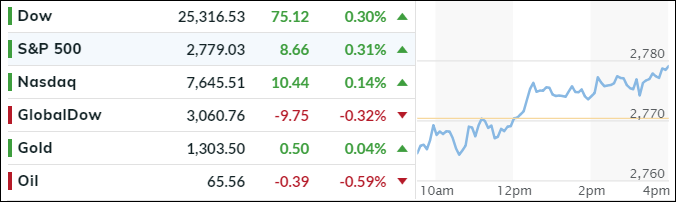

Despite a weak opening, the major indexes managed to gain some footing and climb above the unchanged line to close in the green. This performance was their strongest week in a quarter assisted by the biggest short squeeze in 4 months along with a low VIX.

Since the start of April, according to ZeroHedge, the “most shorted stocks” have dramatically outperformed the S&P 500, while the FANG stocks traded leadership roles with the financials.

I recently referred to this as climbing a wall of worry and today was no different, as tensions between the U.S. and their major allies escalated ahead of this weekend’s G7 meeting in Canada.

I was not surprised to hear that the disparity in views is so stark that this gettogether has also been referred to as G6+1. It’s politics of pretense with one author quipping “The status quo is the problem, but it can’t be touched.”

Bond yields had a wild week of their own with the 10-year attempting to break through the 3% level, but it fell short as a flash-crash pushed yields sharply lower. In the end, we closed at 2.93%, unchanged from yesterday.

The focus right now will be on the G6+1 meeting with anxiety being high to see if any agreements can be reached. If not, there is hope that at least a joint statement will make headlines.

Next week, it will be business as usual with Italian/Argentinian banking issues, along with Deutsche Bank’s attempt to find a lifeline, being front and center.

{kind=link}

{kind=link}