- Moving the markets

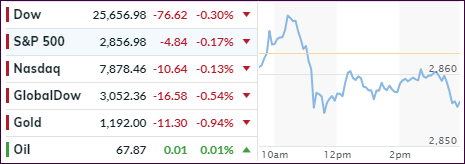

It comes as no surprise that, after yesterday’s strong run-up, the major indexes took a bit of a breather, however, they still managed to close in the green, despite dipping below the unchanged line several times during the session.

So far, it looks that this month may turn out to be the second-best August since 2009, a very interesting occurrence, especially when considering the ever widening gap between the S&P 500 and the collapse of US economic data, which is hardly awe inspiring (hat tip to ZH for these charts).

So, the markets appear to be driven by other factors, and not sound fundamentals. Today, a small assist came from a measure of consumer confidence that hit a nearly 18-year high and was an exception to the slumping data points of the recent past.

The foreign currency debacle continued today led by the Turkish lira plunging -2.35%. This escalated predominantly in the Latin American countries as this chart shows. However, the shakeup was not big enough to make the headlines nor did it affect domestic equities.

Nevertheless, after a slow start, stocks came alive during the second half of August and put in a good performance, despite this being the dog days of summer. With only 3 trading days left, let’s see if traders’ appetites remain bullish.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}