- Moving the markets

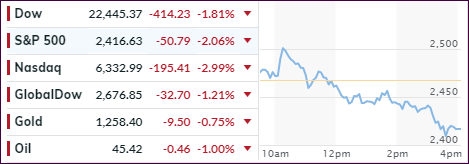

Even a Holiday shortened session wasn’t enough to give the bullish crowd some hope, as the major indexes plunged again with the S&P 500 finally dropping into bear market territory, a level defined as a 20% drop from recent highs.

Starting this mess was Treasury Secretary Mnuchin who, while on vacation, decided to call the heads of the six largest US banks on Sunday to assure them that there was plenty of liquidity in the system. He then proceeded set up a meeting with Plunge Protection Team (PPT) – on Christmas eve! Unfortunately, he also decided to tweet about it, which was akin to someone yelling “FIRE” in a crowed theater.

The fallout was immediate with the markets retreating, when a sudden rebound (PPT?) pushed the Nasdaq back above the unchanged line, before heavy selling set in, which sent the Dow down some 650 points. Good thing we had an abbreviated session, or the consequences could have been a lot worse.

As I pointed out before, this is now the worst December for the S&P 500 since the Great Depression (1931), and there are still 4 trading days left, which might create some problems for those who have not moved to the sidelines yet, as exit doors are getting increasingly crowded. You could consider this session to be a bloodbath, since volume was just about double of the recent average.

ZH noted that even the traditional safe-haven stocks were pummeled with the S&P 500 utilities index dropping as much as 4.6% intra-day, the most since August 2011, because of the continued threat of higher interest rates. That’s why cash on the sidelines never looked so good.

No one saw this market disaster coming except for our Domestic Trend Tracking Index (TTI), which generated a “Sell” effective 11/15/18. Since that moment in time, the S&P 500 has now lost -14.16% allowing all clients in my advisor practice to sidestep this financial tragedy, while the Buy-and-Hold crowd seems to end up with the short end of the stick again—for the third time this century.

Although I expect some sort of rebound make its presence felt, it will most likely only be a bounce in an ongoing bear market, which I believe has a long way to go.

I wish you a Merry Christmas!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}