ETF Tracker StatSheet

You can view the latest version here.

BANKING ON A FED RATE CUT

- Moving the markets

Yesterday’s rally continued this morning and accelerated throughout the session, as traders were now convinced that a rate cut by the Fed is a sure thing, so front running was the name of the game.

Since Fed chair Powell’s 2-day congressional testimony did not include any negatives, but rather words like the U.S. economy is in a “very good place,” traders felt invigorated that a cut was coming, so the bullish theme continued.

Even a stronger-than-expected U.S. inflation print in core producer prices could not put a dent in current enthusiasm, with further support coming from hopes the global economy will slow even more, forcing the Fed’s hand for a possible 0.5% reduction in rates.

One analyst summed it up like this:

This is one of those mornings where bad news is good news for stocks, while good news is bad news for bonds… or in other words, any news is good for stocks.

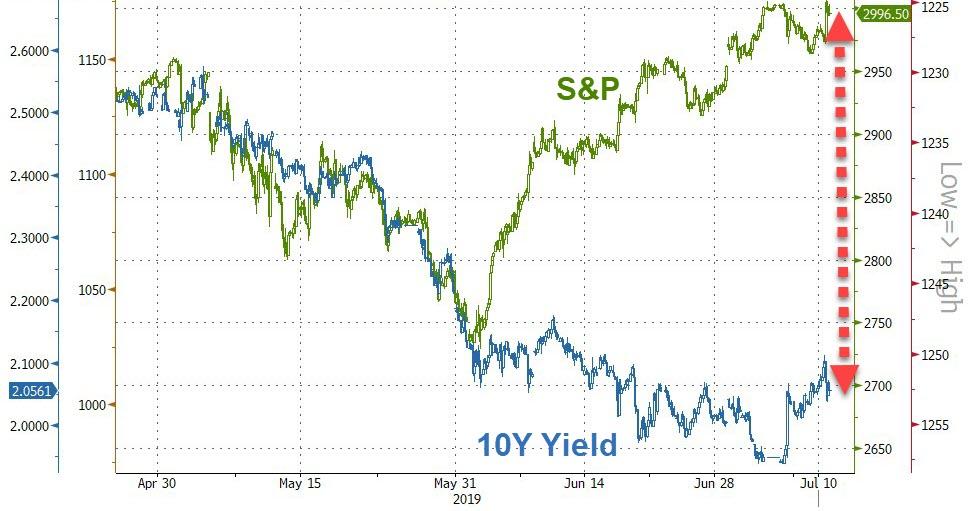

The bullish view did not carry through all investment arenas. Chinese, European and Small Caps all lost for the week. Bond yields suffered, especially in Germany where the 10-year spiked the most since the middle of 2017, as prices collapsed.

Same here in the U.S. with specifically the 30-year yield jumping to 7-week highs, as the dollar corrected back down after its surge following the payroll announcement.

Things appear very uncertain and confusing, when looking at the big picture, which led BofA to release the following statement:

“…we anticipate an “overshoot” in credit & equity prices in coming months, followed by an overshoot in gold (US$ devaluation) before big H2 top in asset prices (as bond bubble pops & policy impotence visible).”

That prompted ZeroHedge to update this chart, which suggests that a picture is worth a thousand words.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}