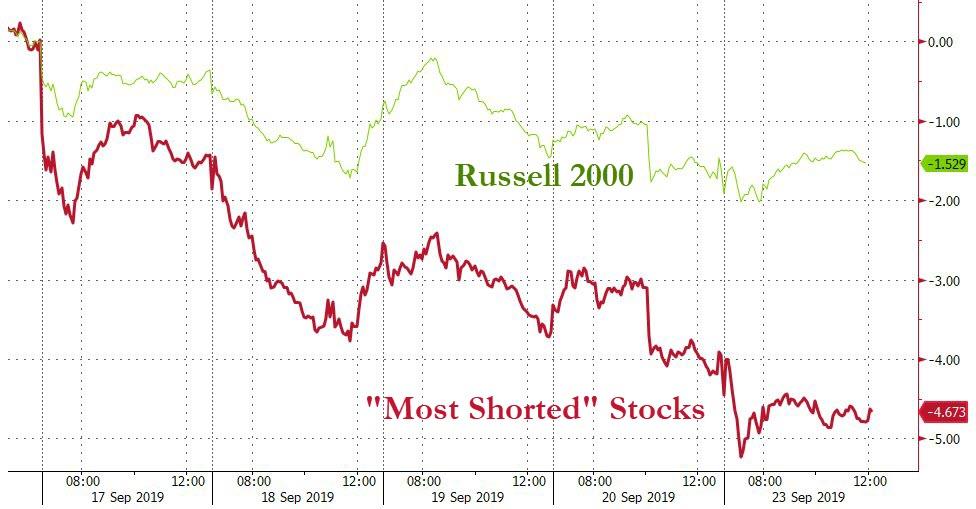

- Moving the markets

The markets were trading in the red for most of the session, as the latest trade headlines pushed equities further south and then gave traders hope that optimism is warranted.

When things looked bleak at mid-day, Reuters managed to provide the algos with some ammo to drive the indexes out of the doldrums and back up to their respective unchanged lines using the following:

- CHINA’S WANG YI SAYS HOPES BOTH SIDES CAN TAKE ‘MORE ENTHUSIASTIC MEASURES,’ REDUCE PESSIMISTIC LANGUAGE AND ACTIONS IN TRADE DISPUTE – RTRS

- CHINA’S WANG YI SAYS ‘IF EVERYONE DOES THIS, TALKS WILL NOT ONLY RESUME, BUT WILL PROCEED AND YIELD RESULTS’

Despite that effort, the unchanged lines proved to be overhead resistance, and we sold off into the close, but with only modest losses.

Adding to the negative early sentiment was the Trump Administration confirming that it’s “unlikely to extend temporary wavers to supply Huawei.” That reinforced that the US-China trade deal is simply not getting closer to an agreement, even though other headlines attempt to prove that a deal is close.

Real Estate provided some optimism when Pending Home Sales rose 2.48% YoY, which was the biggest annual jump since April 2016, but it was simply not enough firepower to restore bullish momentum.

The overnight liquidity shortage, also known as the funding disaster, keeps getting worse with the Fed as lender of last report supplying some $60 billion in liquidity after yesterday’s $92 billion.

No one has really come out to explain the source of the problem and if it might be just a quarter ending issue. MSM does not report about it, but somewhere the financial plumbing in our system has sprung a leak.

One analyst posed the thoughts that have been on my mind as well:

- It’s great that the Fed is pumping liquidity into the system, however, why were the existing operations insufficient?

- As of today, the Fed had injected $105 billion in liquidity into the Repo market, but rates were still stubbornly high. Whatever changed last week to cause the funding spikes is clearly still a problem.

If this problem is not resolved quickly but spreads even further, equity markets will eventually be negatively affected.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}