ETF Tracker StatSheet

You can view the latest version here.

SLUMPING INTO THE WEEKEND

- Moving the markets

An early 100-point gain on the Dow evaporated in a hurry and turned into a 150-point loss at one point, after a report that the White House had thrown down the gauntlet by contemplating delisting Chinese stocks from US Exchanges.

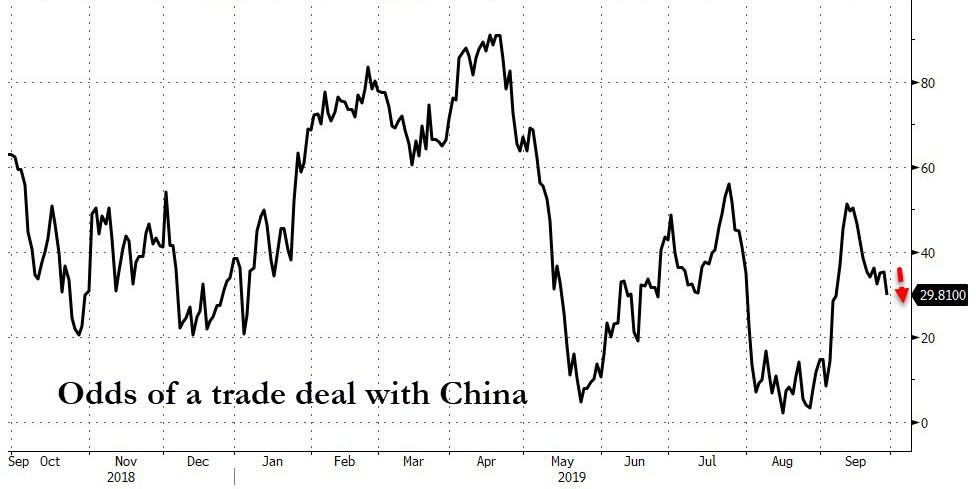

Of course, such a crackdown on capital flows does not bode well for softening the intensity of the tariff battle being waged. This news comes in the face of the warring parties having set an Oct. 10-11 date to meet to resolve their trade differences. I don’t see how this ratcheting up of tensions will be of any value but, it could be simply a negotiation ploy. In the end, the odds of a China deal slipped this week.

Economic data points were mixed with consumer spending growth showing disappointing estimates, while orders for durable goods rose 0.2% in August vs. expectations of a 0.7% decline. But the consumer sentiment was revised upwards in September from 92 to 93.2, however, the index remains on a downward trajectory.

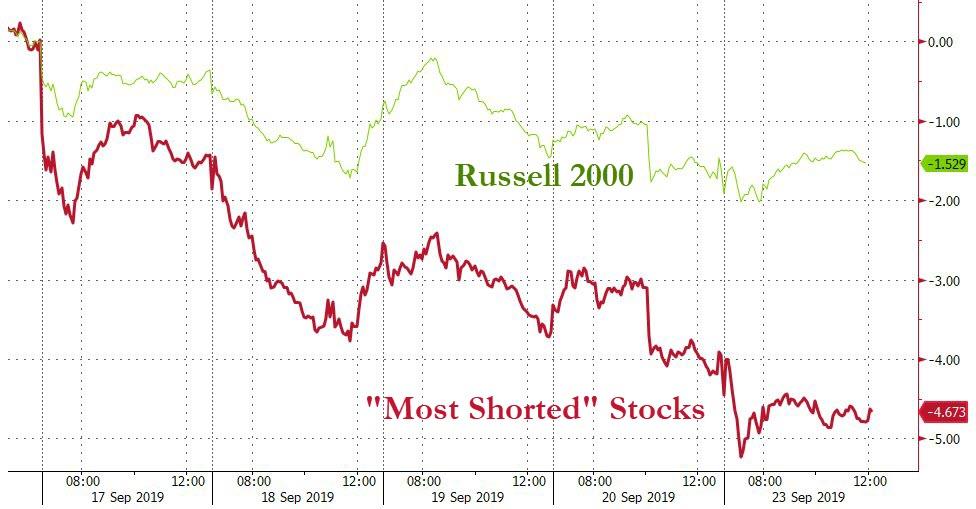

On the week, equities fell with Small Caps leading the drop and having its worst week since May 2019. As ZH pointed out, all the major indexes tested or broke below key technical levels: The Nasdaq below 50 and 100 DMA; Russell 2000 below 200 DMA; S&P testing 50 DMA.

10-year yields attempted several times to break out above the 1.70% level, but the efforts were rebuffed, and we closed the week around the 1.68% area.

This was the second losing week in a row for the S&P 500, but it’s still hanging on to a gain for the month. For sure, it looks like a very positive trade headline is needed next week to get the bulls going again.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}