- Moving the markets

Overnight, the Japanese markets painted a gloomy picture, as Tokyo pushed for a third COVID state of emergency with new cases spiking. Full-fledged lockdowns are being considered with the IOC possibly canceling this summer’s Olympics.

That gloomy mood carried over into the US markets, with major indexes opening to the downside but never managing to stage any kind of recovery. A last hour bounce reduced losses somewhat, but the overall tone remained bearish.

Even strong corporate earnings did not provide enough ammo to improve market sentiment. On a global basis, Covid cases in India followed Japan’s example, thereby questioning the much hoped for positive reopening scenario.

Airlines led the surge to lower prices, after UA reported its fifth consecutive quarterly loss. SmallCaps, which started the year with a bang, puked today with the Russell 2000 dropping below its 50-day M/A with not much support down to its 100-day M/A, according to ZH.

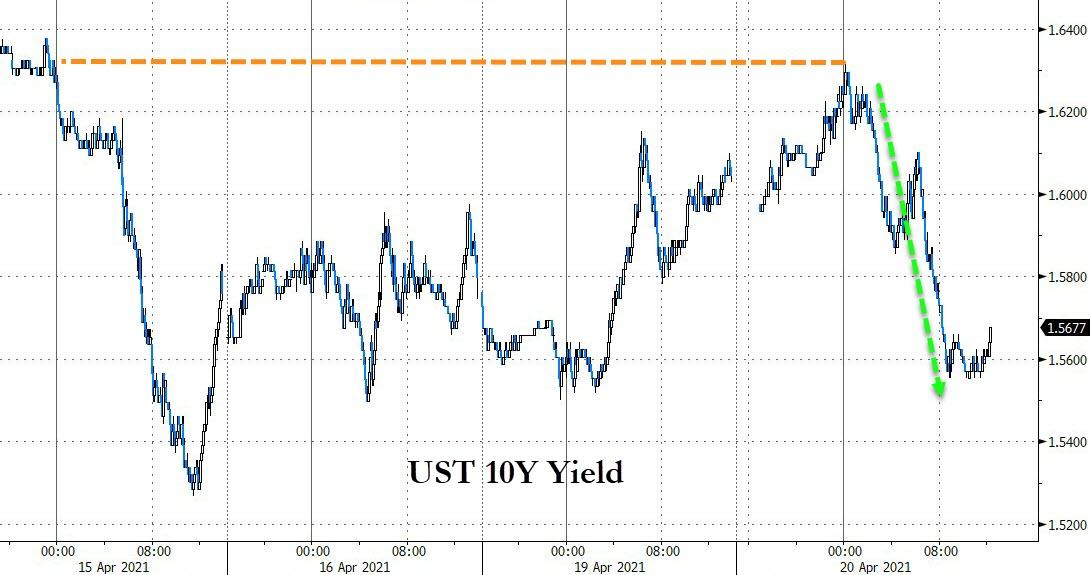

With so much uncertainty, bond prices benefited as yields slid below 1.6%, allowing Gold to add a modest 0.46%, which was one of the few green numbers we saw today. The US Dollar also rebounded from a recent steep sell off and did not affect gold negatively, which is odd.

Right now, the markets look somewhat frothy and overbought, which why we are seeing this correction. After all, we just witnessed new ATHs for the Dow and S&P 500 last Friday.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}