- Moving the markets

During the early part of today’s session, the market ping-pong continued, when the major indexes took a steep dive with the Dow down some 400 points and on pace to again wipe out the previous day’s gains.

However, a slow but steady rebound ensued with equities digging themselves out of a deep hole and scoring a green close, the second one in a row. This rebound was supported by optimism about a debt ceiling deal, causing traders to jump back into the much-neglected tech sector.

CNBC called it this way:

Stocks reversed course on news that Senate Minority Leader Mitch McConnell told a closed meeting of Republicans that he would offer a short-term debt ceiling extension later Wednesday. That would help relieve some pressure on Congress to avoid a U.S. default currently expected on Oct. 18.

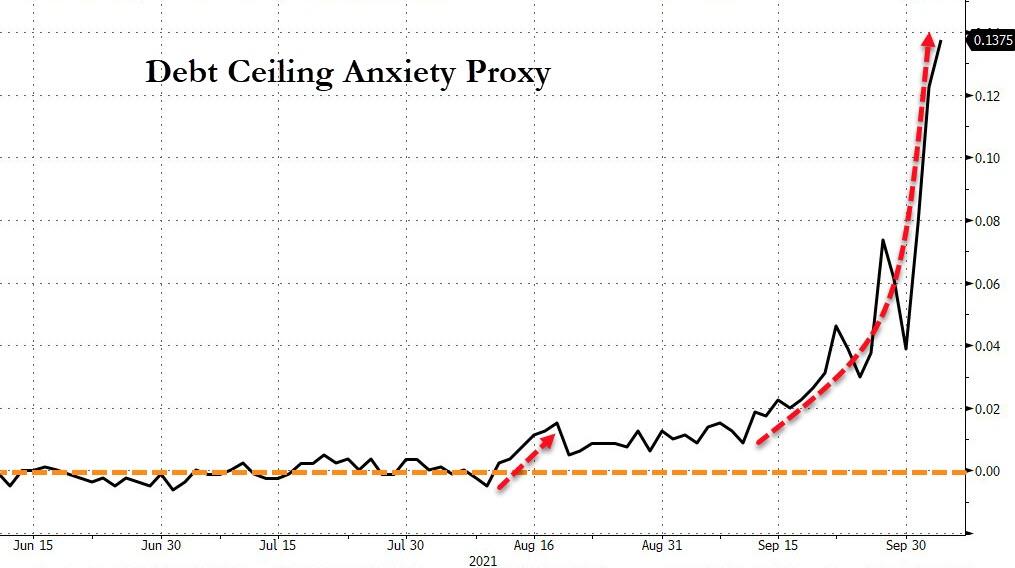

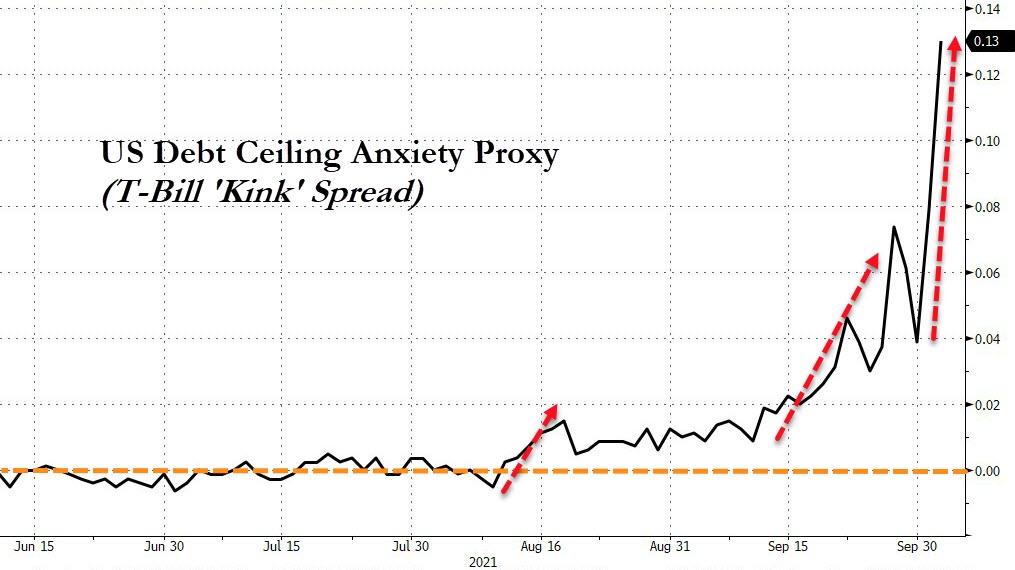

As a result, the dip was bought, despite nagging concerns about risings interest rates, surging inflation, the state of reopening, and the debt limit being on everyone’s mind.

Bond yields spiked and then tumbled but closed higher with the 10-year ramping to almost 1.57%, before pulling back into the close and ending the day at 1.528%.

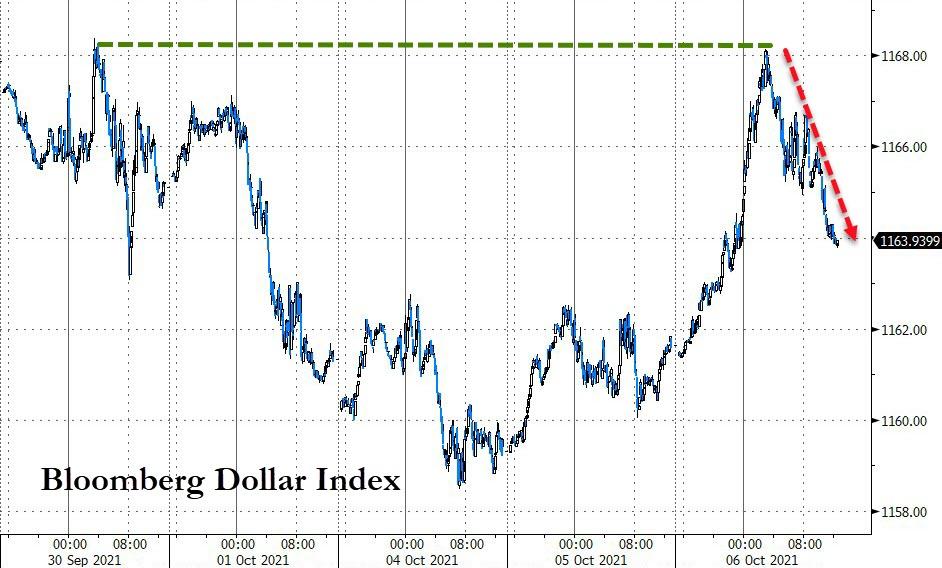

The US Dollar moved in similar fashion, first up and then down, but it also closed higher for the session.

The roller coaster ride in both, bond yields and the dollar, aided Gold for the day with the precious metal bouncing moderately and scoring a gain of 0.23%.

So far, the month of October has sure lived up to its reputation as the most volatile month of the year. And we’re only 6 days into it.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}