- Moving the market

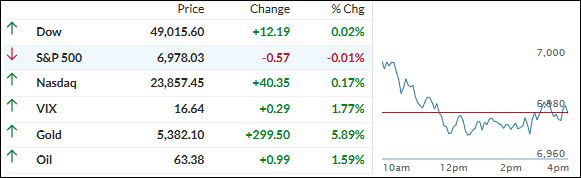

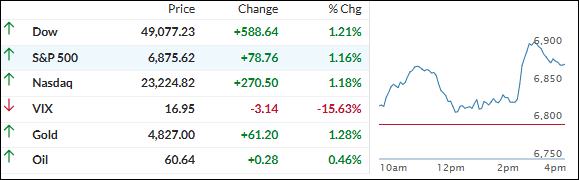

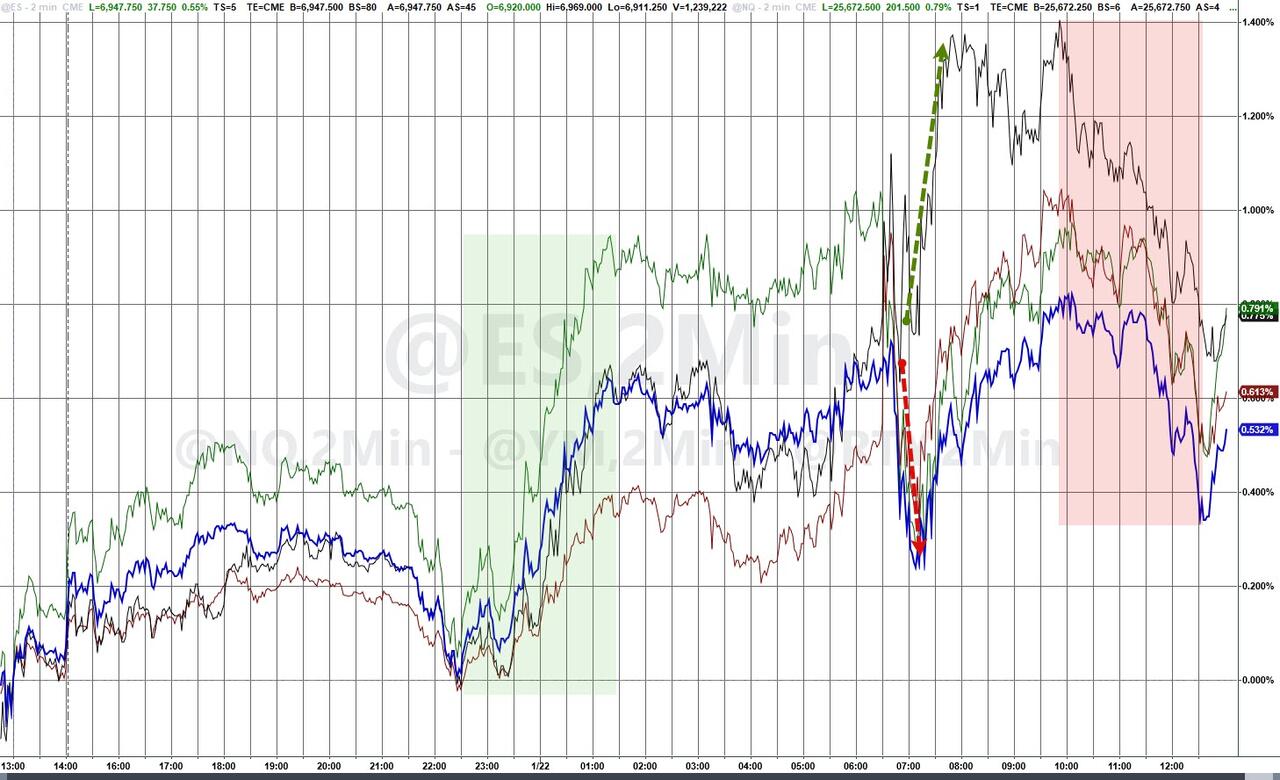

The S&P 500 finally touched 7,000 for the first time intraday—nice milestone! —but the broader rally ran out of steam by the close.

Chip stocks gave us an early boost after some upbeat earnings: Seagate soared more than 17% on strong AI data storage demand, and ASML reported record orders with solid 2026 guidance. That juiced the sector for a while, but the gains mostly faded by the end.

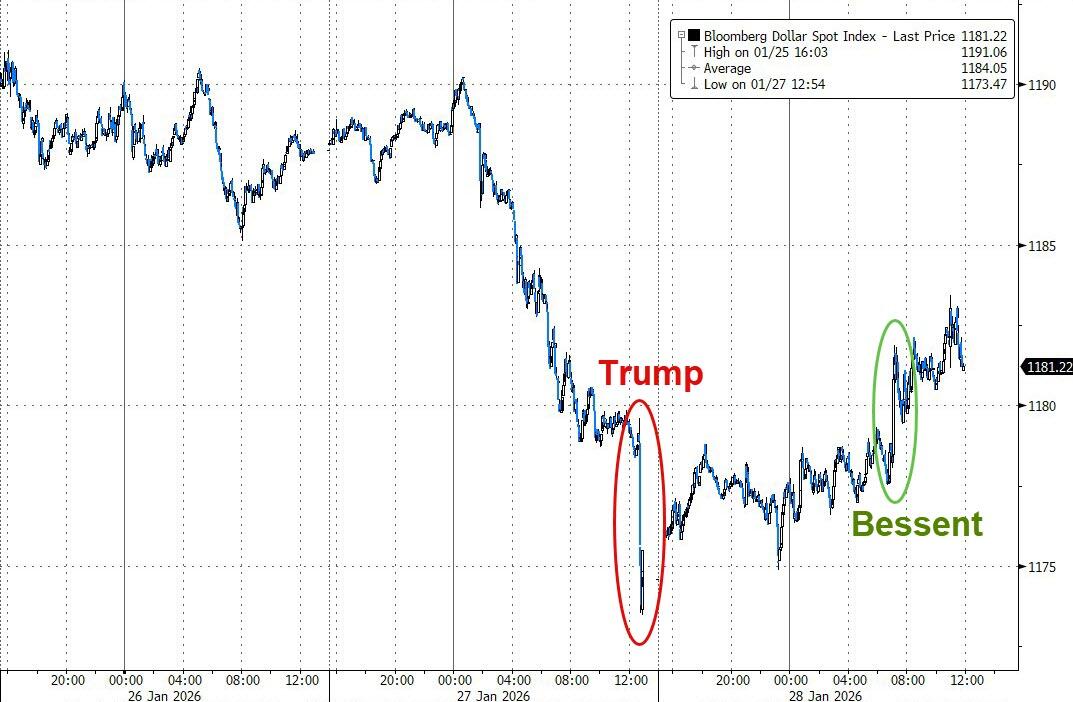

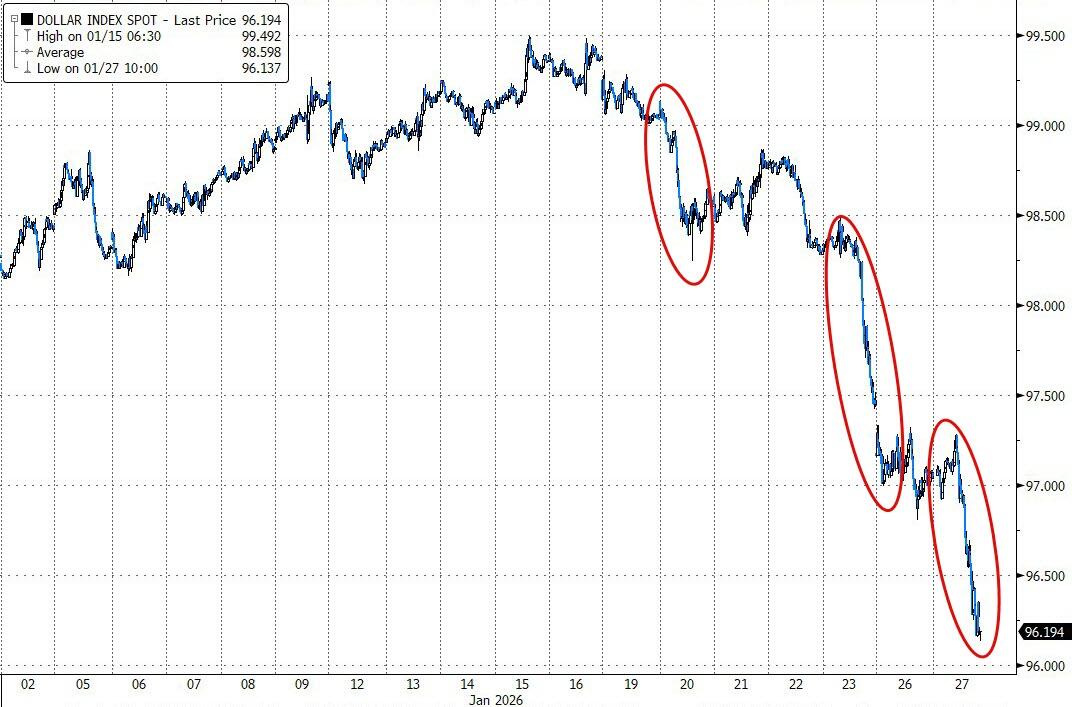

Traders were also watching the dollar after its big drop Tuesday (worst day since last April), though it clawed back a bit today.

The macro picture still looks decent—growth holding up, labor market soft but stable, inflation above the Fed’s target—so there wasn’t much case for an immediate rate cut.

The Fed held steady as expected, and Chair Powell’s comments didn’t drop any big surprises, so markets basically shrugged.

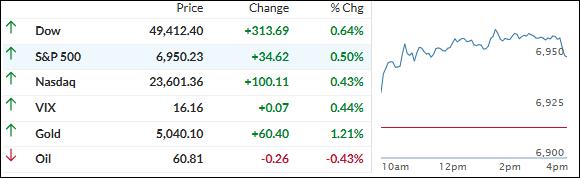

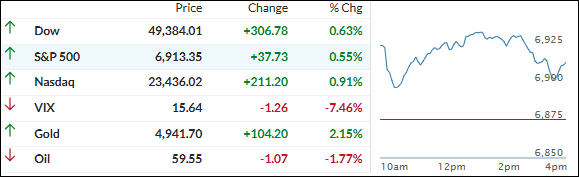

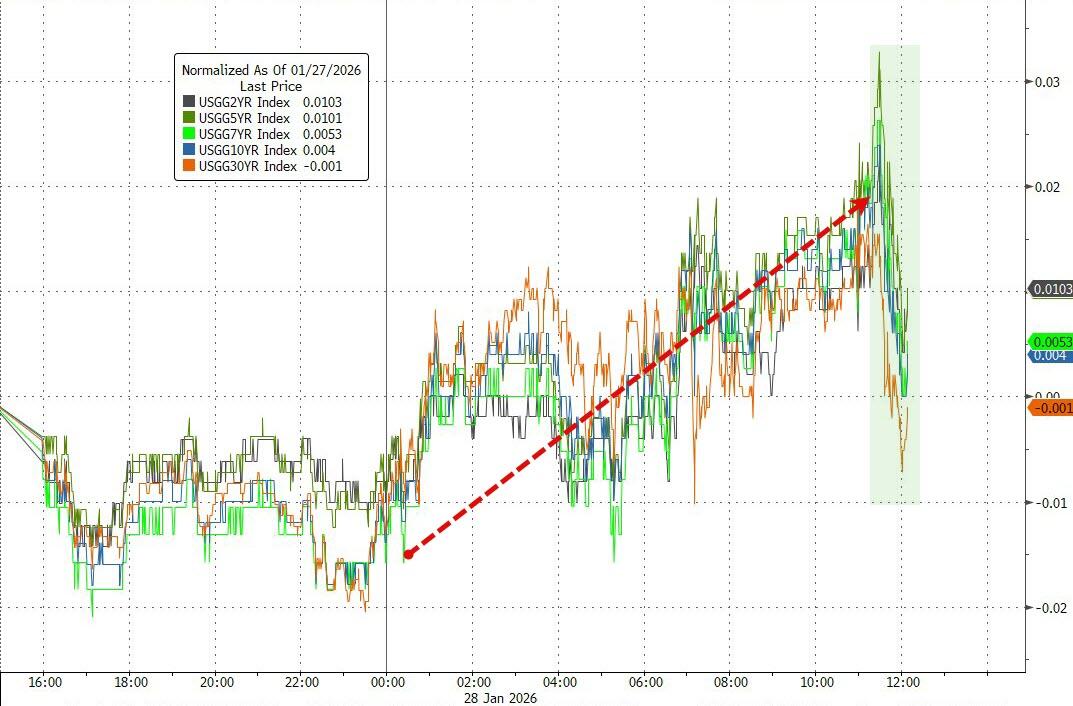

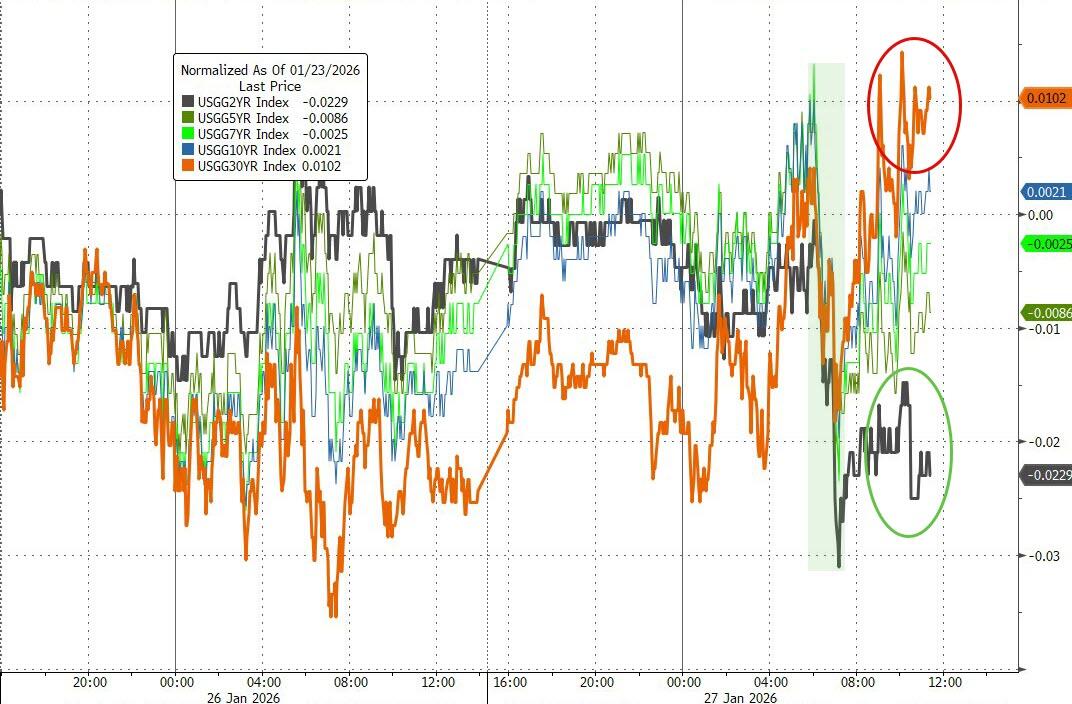

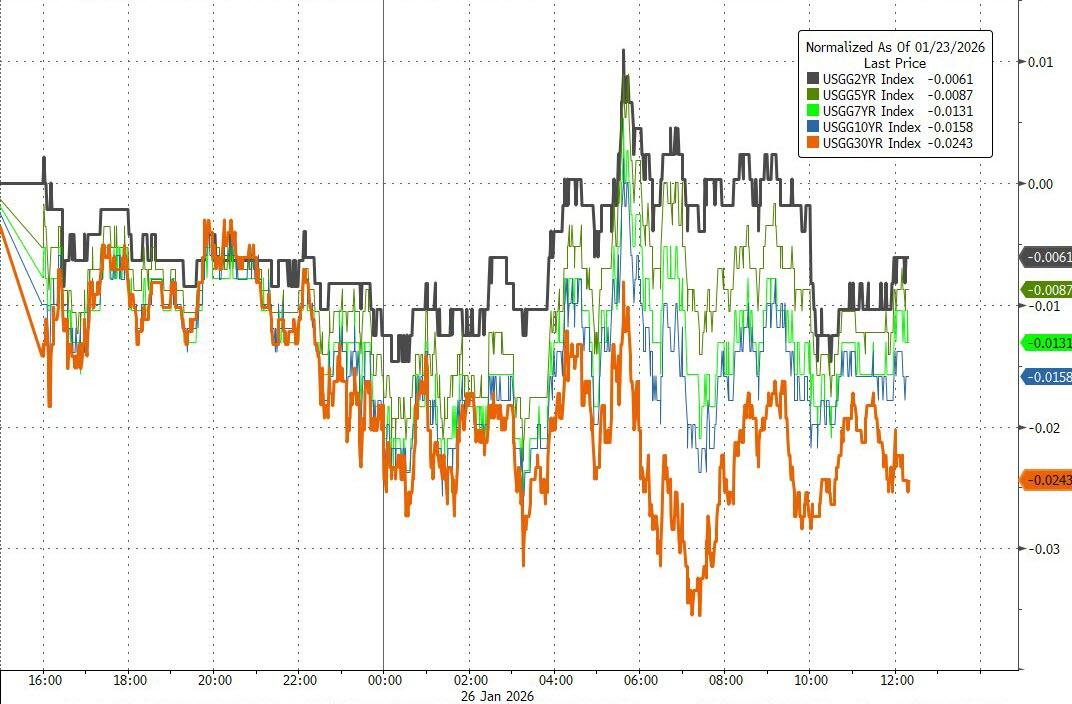

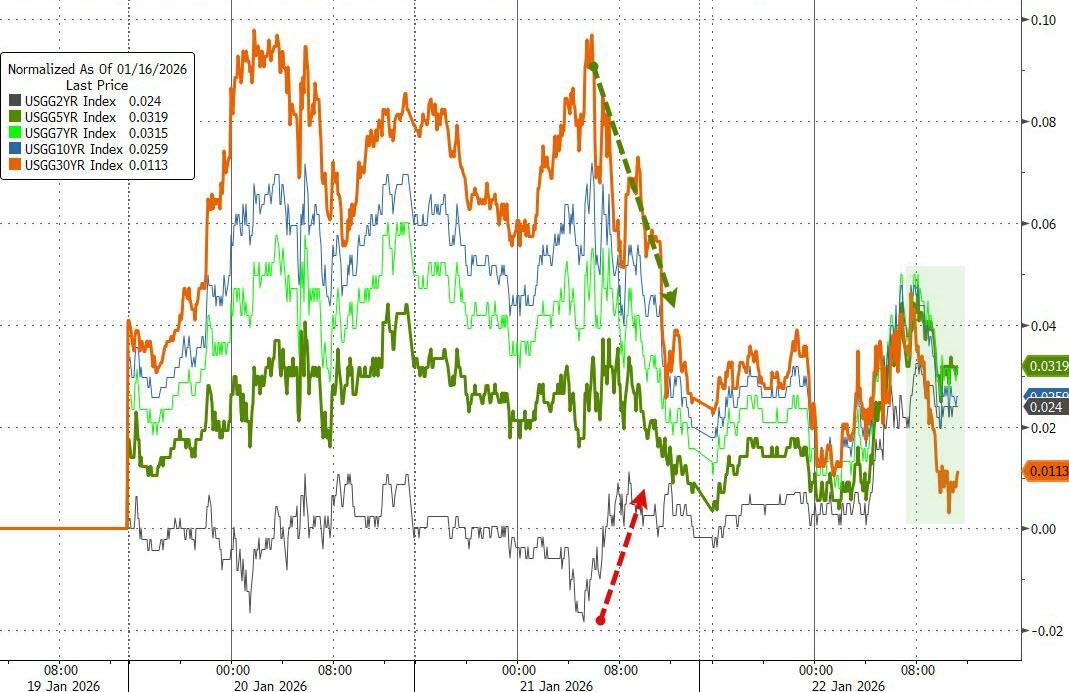

In the end, the major indexes closed near flat, with only the Nasdaq squeaking out a tiny gain. Bond yields were all over the place, rate-cut expectations dipped, but the dollar showed some life.

The real action?

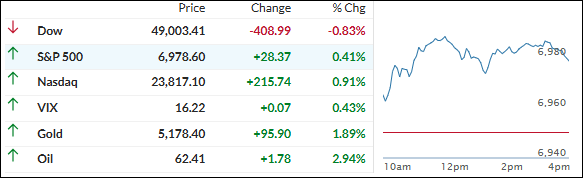

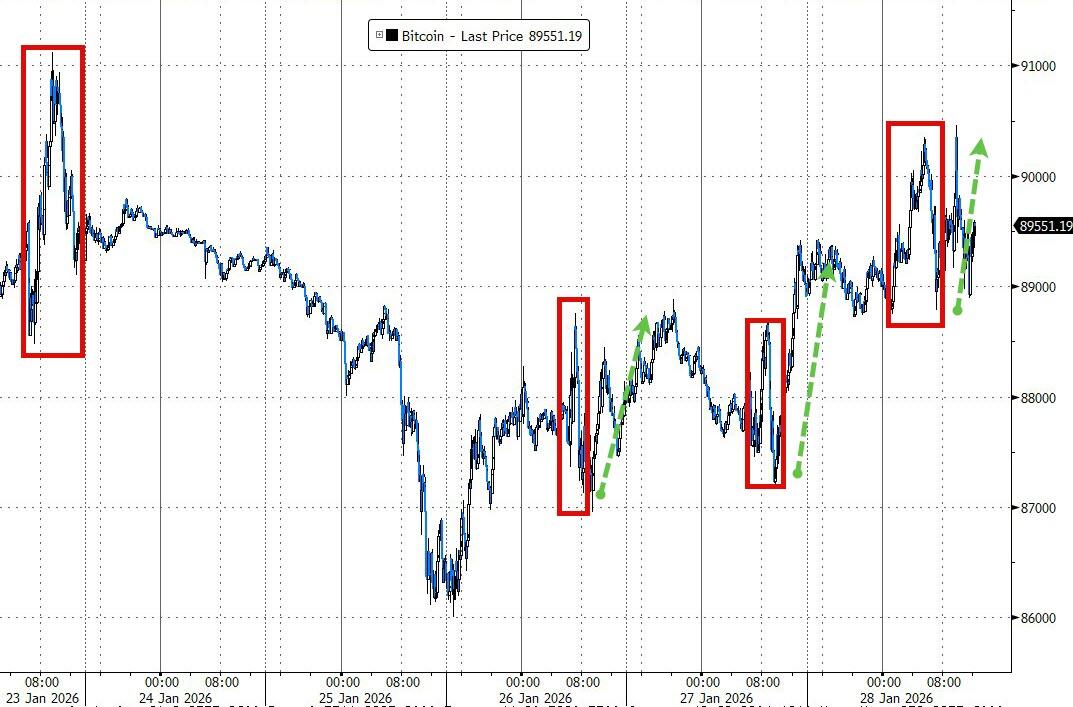

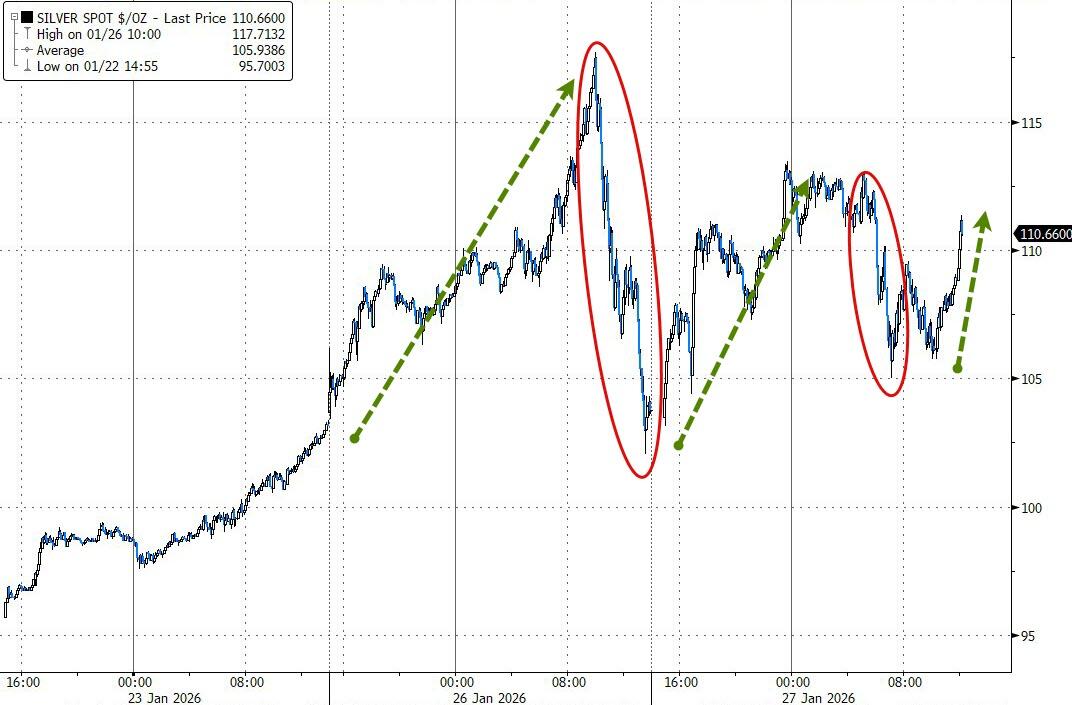

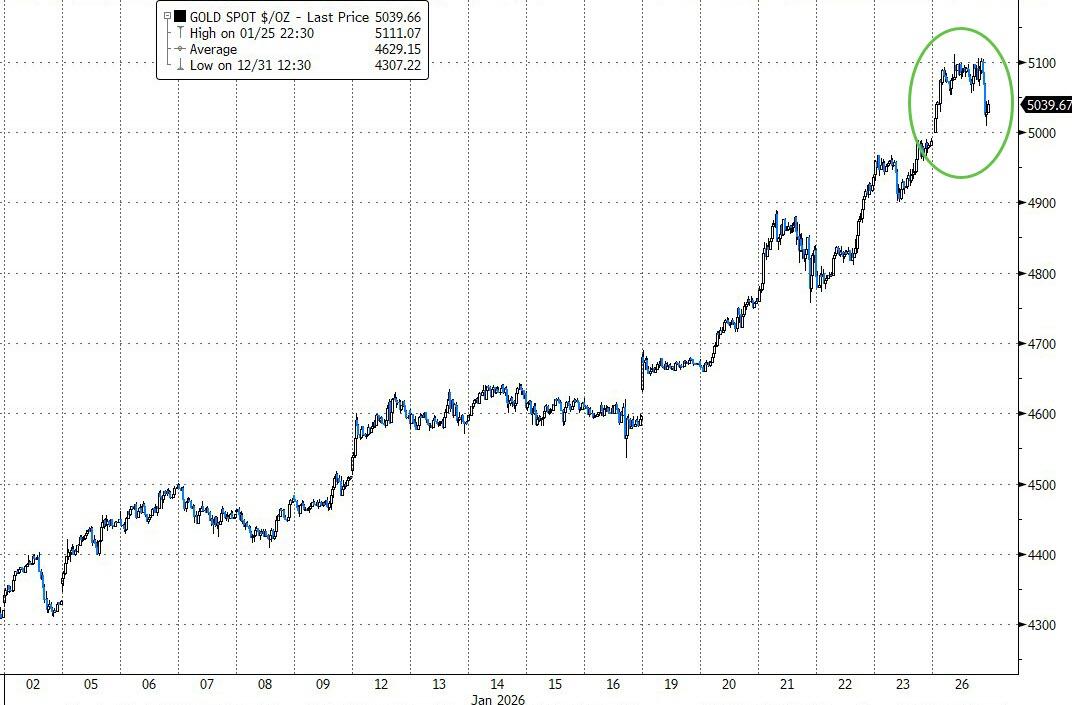

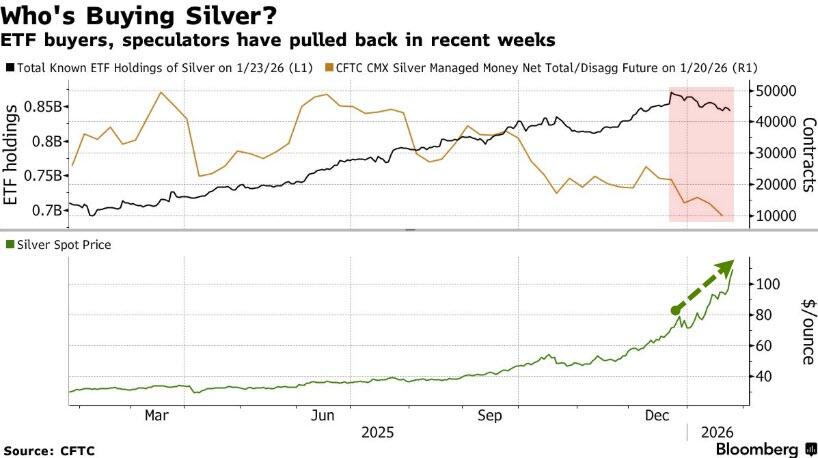

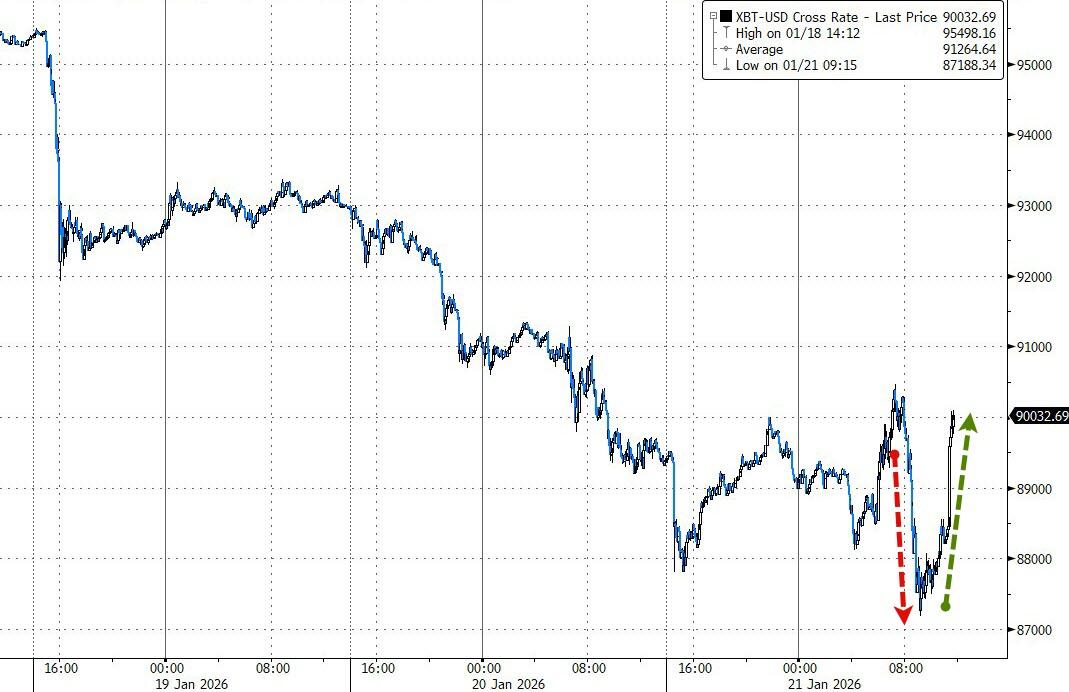

Precious metals crushed it again—gold ETF and silver ETF both surged over 3.8%, gold topped $5,300, and silver chopped around but closed near $115. Bitcoin followed suit and climbed back above $90K.

After the Fed passed on a cut and stocks faded but metals keep holding strong, does this feel like a classic “no news is bad news” reaction… or a healthy reminder that hard assets are still doing the heavy lifting in this environment?

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}