[Chart courtesy of MarketWatch.com]

- Moving the market

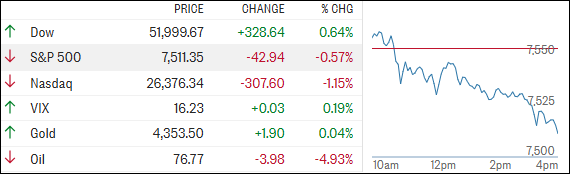

The S&P 500 started the day pretty flat, while the Dow was still riding the momentum from its fresh record close in the previous session, helped by optimism around a potential U.S.–Iran deal.

One of the biggest stories was SpaceX, which kept its post-IPO hype going with another 10% jump. The move briefly pushed its market cap past both Microsoft and Amazon during the session—pretty wild for a company that just went public last week.

Meanwhile, oil continued to slide. Brent crude dropped about 3% to around $80 per barrel, even dipping below that level briefly for the first time since March.

Easing geopolitical tensions, including news that Pakistan and its counterpart agreed to end military operations, added to the downward pressure. There were also comments about the Strait of Hormuz reopening, which helped accelerate the drop in oil prices.

Despite the generally upbeat backdrop, investors aren’t exactly worry-free. Inflation remains the top concern for 34% of traders, while 28% are increasingly uneasy about a potential AI bubble forming.

By the closing bell, the story was mixed. The Dow managed to hold onto gains, but tech stocks struggled, dragging the S&P 500 and Nasdaq into the red.

Even falling oil prices couldn’t give tech much of a lift, though consumers may welcome some relief at the gas pump.

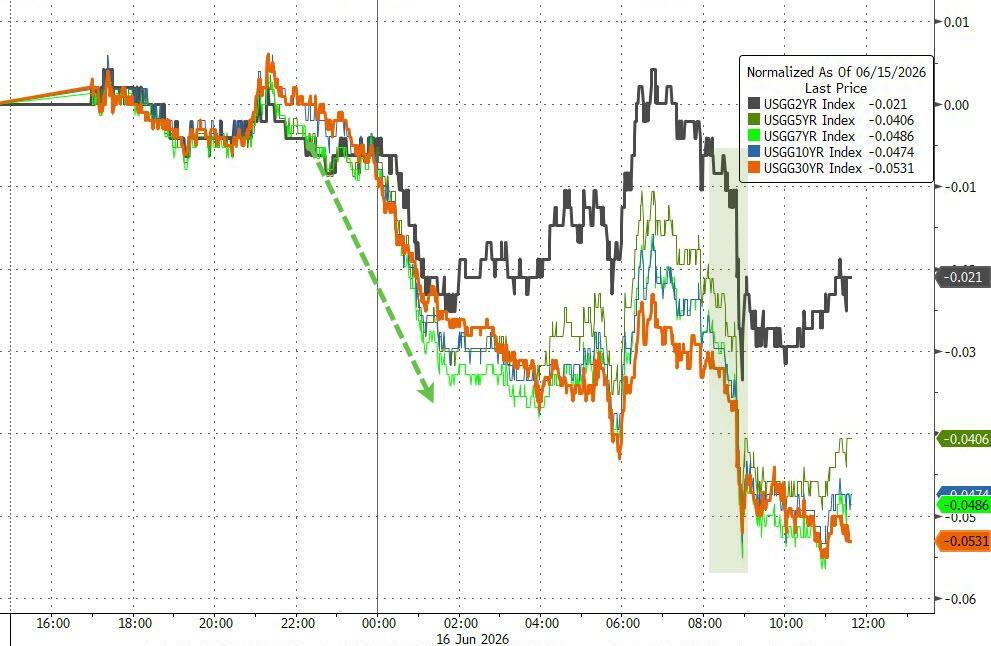

In other markets, bond yields moved lower, with the 30-year dropping well below 5% to its lowest level since April. The dollar softened, gold edged slightly higher, and Bitcoin slipped back below $66K.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Now, with the FOMC meeting up next and triple witching later this week, the big question is whether the AI-driven momentum can keep carrying the market—or if these headwinds will finally start to bite.

So, will bullish sentiment keep winning out, or are we about to see a reality check?

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

The three major indexes kicked off the day in the green, but only the Dow managed to keep the momentum going and finish with a solid gain.

Tech stocks, on the other hand, came under pressure, dragging both the S&P 500 and Nasdaq into the red by the close.

In the metals space, gold was the lone standout, ending the day higher while the rest of the sector lagged. Our TTIs mirrored the overall negative tone, pulling back moderately.

This is how we closed 06/16/2026:

Domestic TTI: +8.57% above its M/A (prior close +8.93%)—Buy signal effective 5/20/25.

International TTI: +9.50% above its M/A (prior close +9.75%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli