- Moving the markets

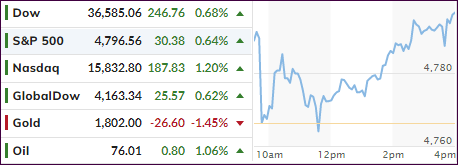

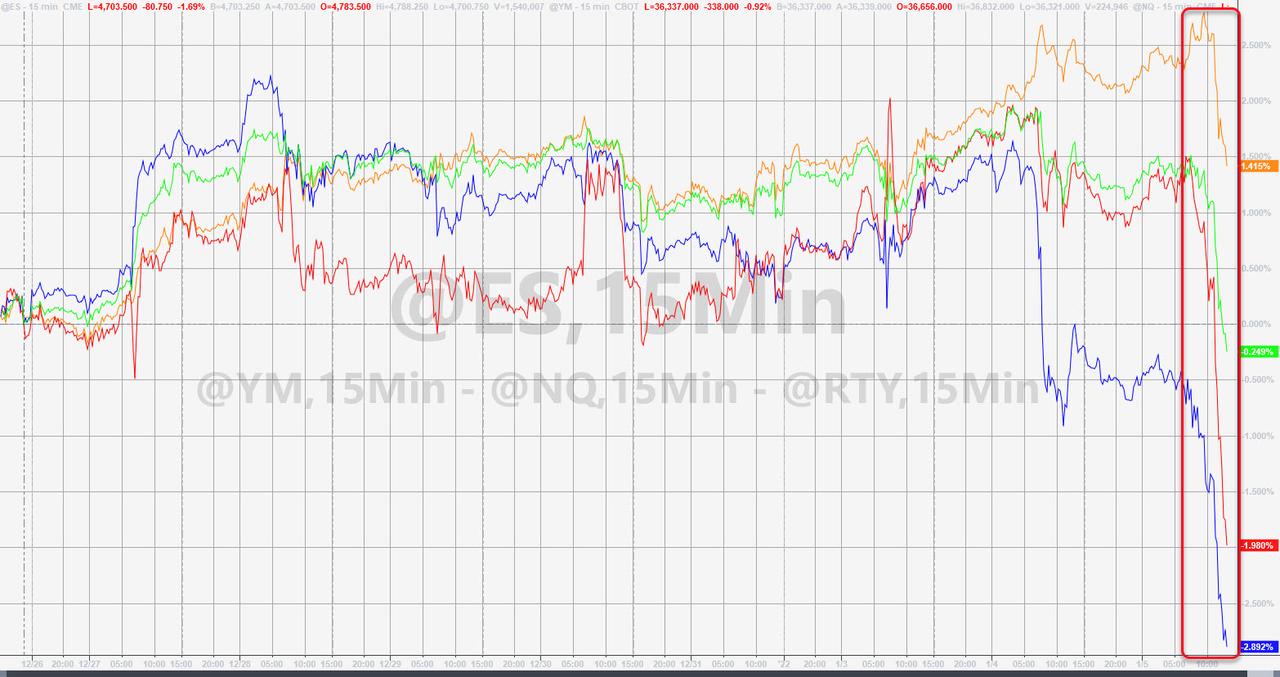

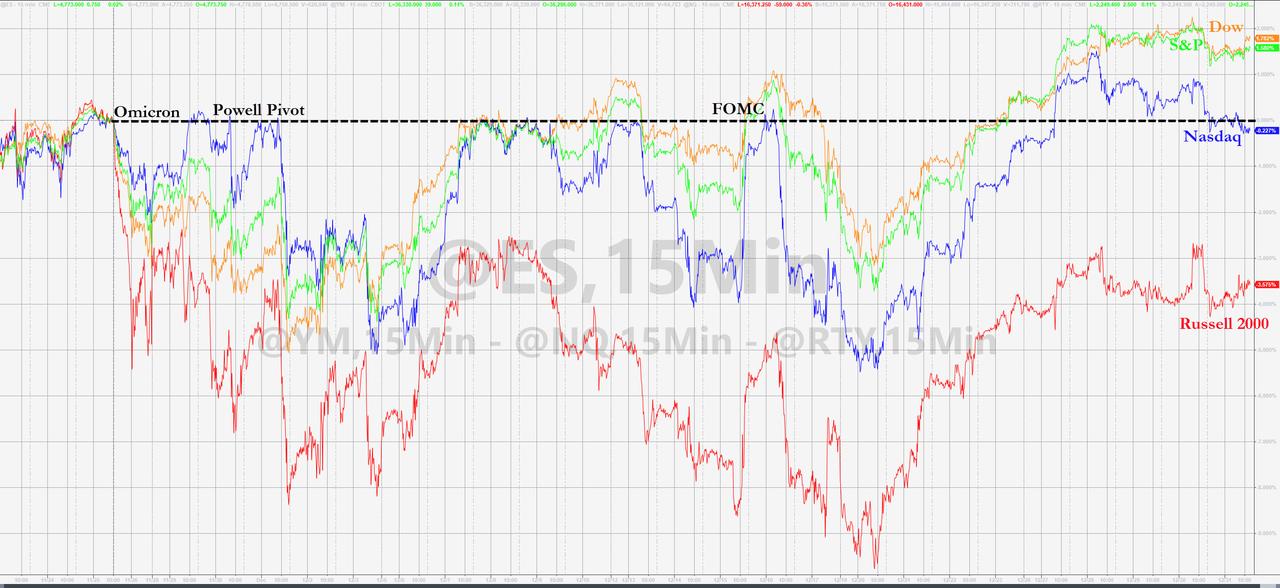

Though the Dow staged a solid rally early in the session, the S&P 500 was barely hanging on to its unchanged line, but the Nasdaq never saw any green numbers. All of this changed mid-day with the major indexes simply losing steam and dumping into the close led by the Nasdaq with a loss of -3.34%.

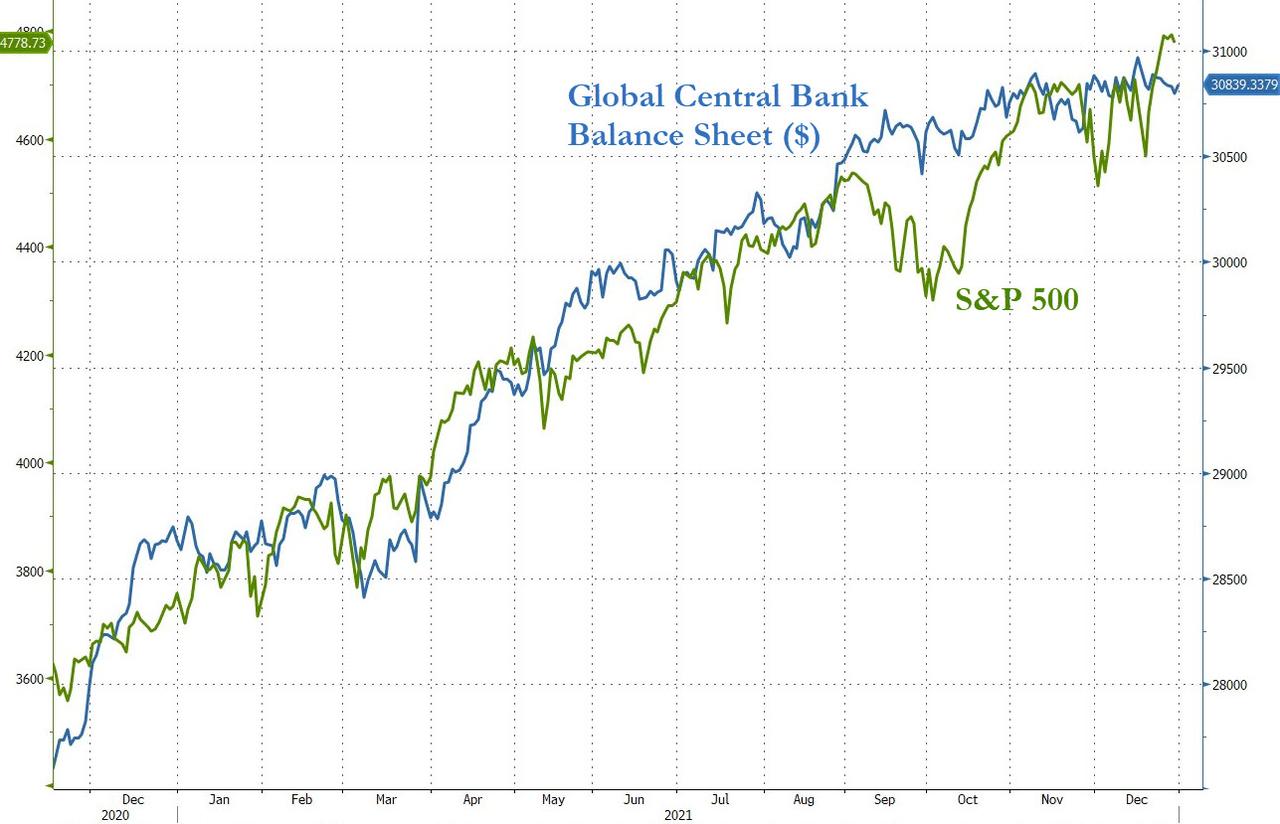

At the center of this turnaround were the minutes of the Fed’s most recent meeting, which showed members discussing a reduction of their balance sheet right after their intended rate hikes later in 2022.

MarketWatch added some color:

The Fed is tapering its bond purchases now and has already indicated to the market that it will raise rates soon after it finishes that taper in March. But the market is awaiting indications from the Fed on what it will do with its nearly $9 trillion balance sheet once it’s done increasing it. The minutes show officials to be considering shrinking the balance sheet along with raising rates as another way to remove policy accommodation.

Ouch! That was more of a hawkish view than traders had expected and down we went. Remember, the increase of the Fed’s balance sheet is and has been directly correlated with market advances, so a reversal of their policy might have an adverse effect due to a reduction in liquidity.

Adding insult to injury, then this:

“Participants generally noted that, given their individual outlooks for the economy, the labor market, and inflation, it may become warranted to increase the federal funds rate sooner or at a faster pace than participants had earlier anticipated,” the minutes stated.

In other words, higher rates and bond yields will be on deck much sooner than expected and may exact their pound of flesh from the markets. As ZeroHedge commented, as of this moment, the entire Santa Claus rally has been erased.

SmallCaps (-4.18%) and Growth (RPG, -3.81%) were hit the hardest, while value (RPV) held up the best by giving back only a modest -0.55%

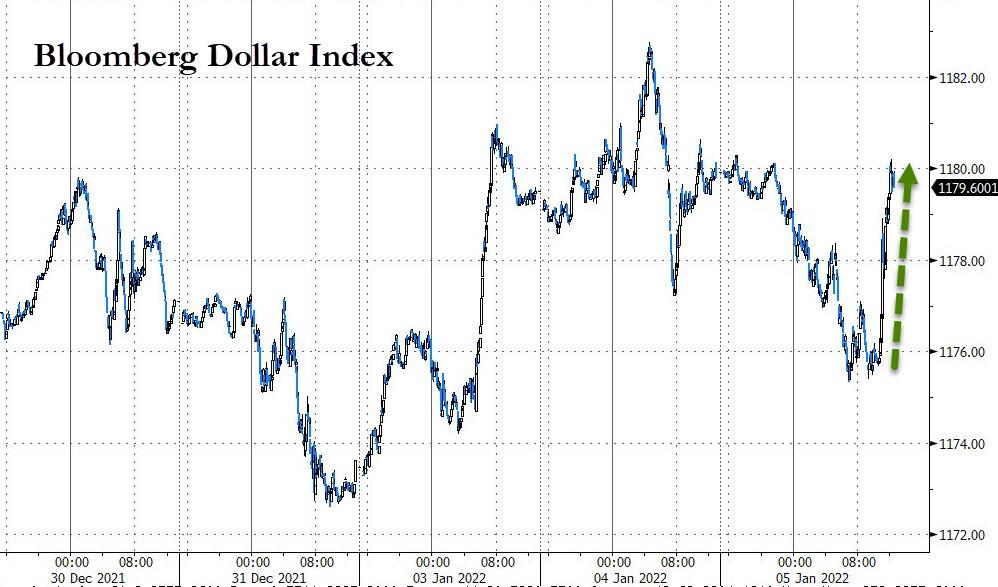

Bond yields rose with the 10-year touching the 1.7% level but closing just a tad below. The US Dollar index rallied and, even though gold held steady above its $1,800 level, it gave back a scant -0.26%.

The question in my mind is this one: How much will the markets have to drop before the Fed reverses policy again and comes to its rescue?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}