Below, please find the latest High-Volume ETF Cutline report, which shows how far above or below their respective long-term trend lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s StatSheet and includes 312 High Volume ETFs, defined as those with an average daily volume of more than $5 million, of which currently 177 (last week 205) are hovering in bullish territory. The yellow line separates those ETFs that are positioned above their trend line (%M/A) from those that have dropped below it.

In case you are not familiar with some of the terminology used in the reports, please read the Glossary of Terms. If you missed the original post about the Cutline approach, you can read it here.

After a swan dive onto the last trading day of September, a month during which the S&P 500 surrendered almost 5%, October started with a bang, after some initial choppiness was overcome.

The major indexes found upward momentum and raced ahead in unison led by the Dow with a gain of 1.43%. Lagging the threesome was the Nasdaq, but it managed to put up a decent performance by advancing 0.82%.

The primary supporting actor came in form of news about a new oral treatment for Covid 19, which boosted spirits and shares alike, with the latter ones being lifted due to exposure in those areas that benefit from the economic recovery.

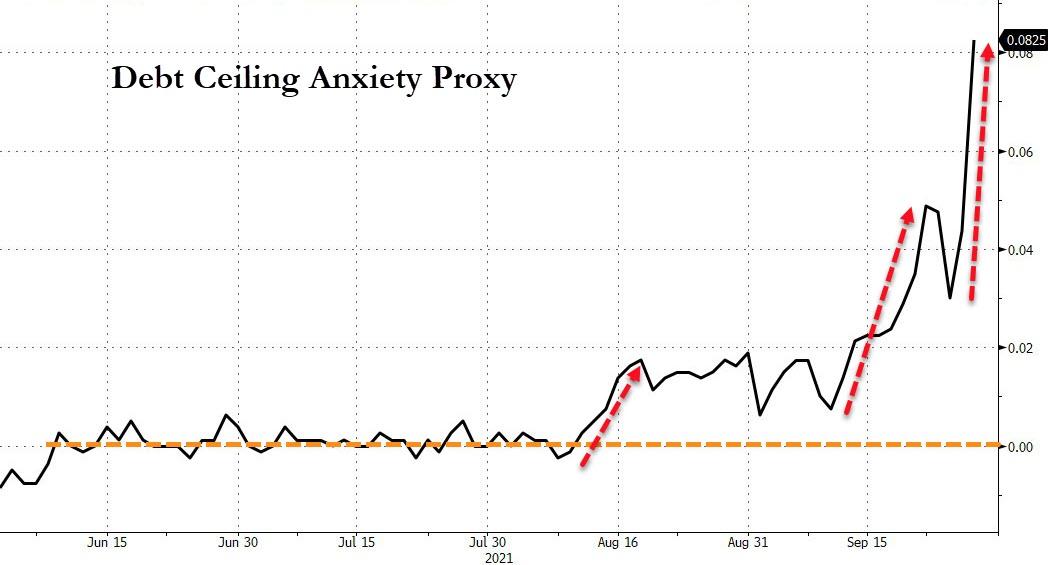

Also helping the mood was the House’s passing of a short-term appropriations bill, which will keep the government running until December 3rd, however, the debt ceiling debacle is still on deck and will have to be dealt with.

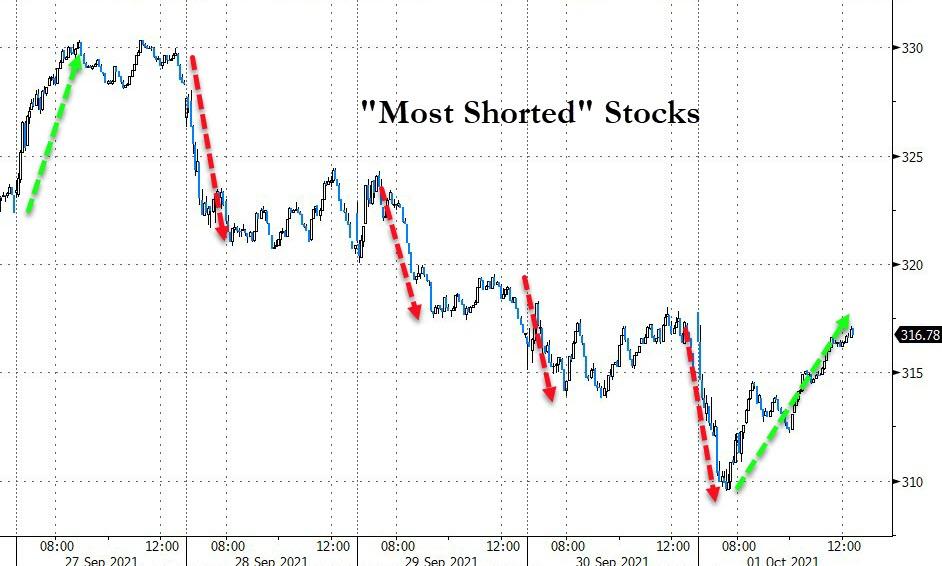

Today’s rebound could not mask the fact that this was an ugly week for equities. Most shorted stocks contributed to the selloff yet today, due to a squeeze, they helped the bounce back.

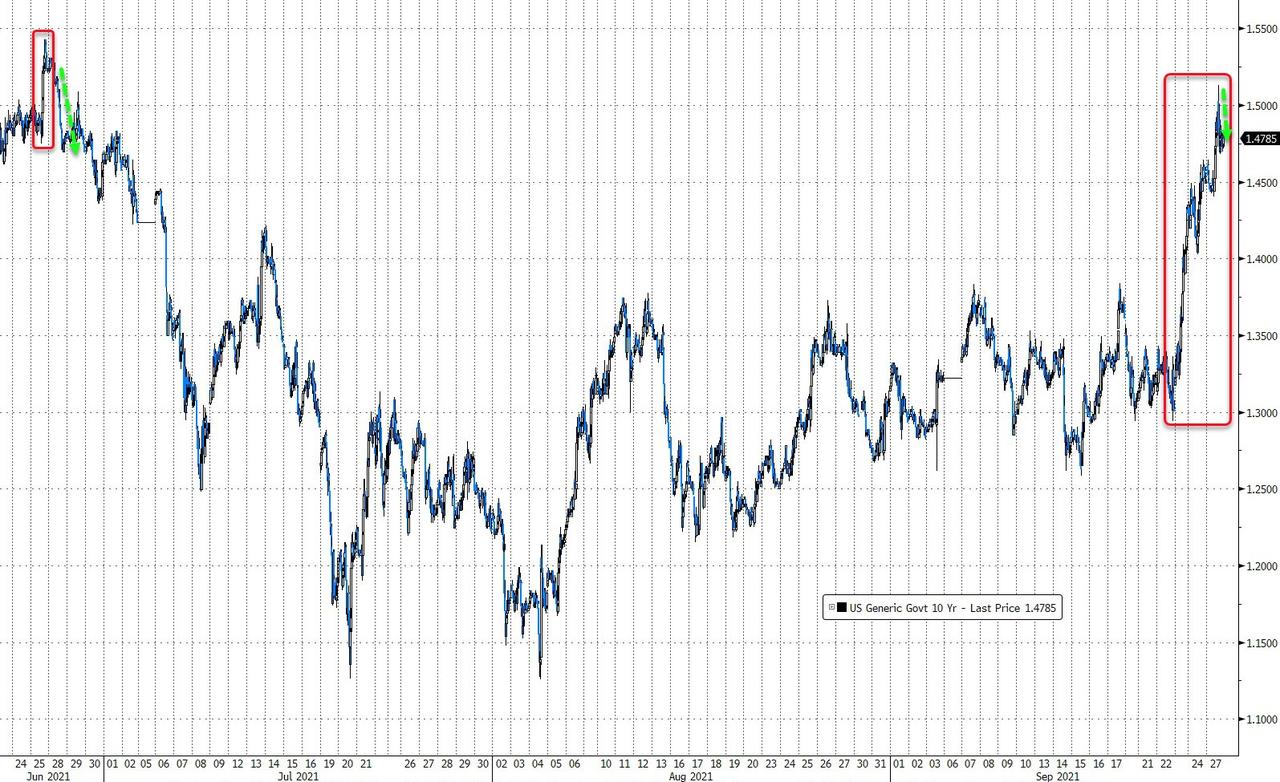

Bond yields pumped and dumped with the 10-year now back down to 1.47%, after having made a high of 1.56% only 3 days ago. The US Dollar ended the week higher, but off the high point set on Wednesday. That combination of yields dropping and the dollar retreating allowed gold to find some footing with the precious metal eking out a tiny gain of 0.19%.

Leave it up to Bloomberg via ZeroHedge to post this updated analog chart which, at least as of this moment in time, appears to be uncanny in its comparison.

ETF Data updated through Thursday, September 30, 2021

Methodology/Use of this StatSheet:

1. From the universe of over 1,800 ETFs, I have selected only those with a trading volume of over $5 million per day (HV ETFs), so that liquidity and a small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and 2), are made based on the respective TTI and its position either above or below its long-term M/A (Moving Average). A crossing of the trend line from below accompanied by some staying power above constitutes a “Buy” signal. Conversely, a clear break below the line constitutes a “Sell” signal. Additionally, I use an 8% trailing stop loss on all positions in these categories to control downside risk.

3. All other investment arenas do not have a TTI and should be traded based on the position of the individual ETF relative to its own respective trend line (%M/A). That’s why those signals are referred to as a “Selective Buy.” In other words, if an ETF crosses its own trendline to the upside, a “Buy” signal is generated. Since these areas tend to be more volatile, I recommend a wider trailing sell stop of 8%-10% depending on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

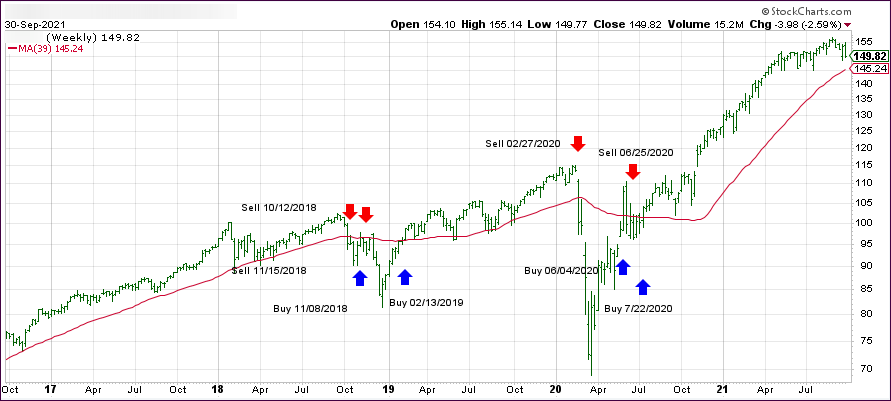

1. DOMESTIC EQUITY ETFs: BUY— since 07/22/2020

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) has now rallied above its long-term trend line (red) by +3.59% and remains in “BUY” mode as posted.

The bulls and bears were engaged in a tug-of-war session with the former seemingly storming ahead only to be pulled back down to reality by the latter. Gains came and went and, when the closing bell rang, only the Dow & S&P 500 were able to barely stay above their respective unchanged lines.

The culprit was the same as yesterday, namely bond yields, which rode the roller coaster again with the 10-year first dropping to 1.5% and then swinging higher in afternoon trading into the 1.54% area.

The Nasdaq followed this trend by being higher early on, as rates eased, but then lost altitude as yields again marched higher. As a result, the pressure was on “growth” with “value” and Small Caps benefiting.

Giving an assist to bearish sentiment was the ongoing Washington debacle with debt ceiling doubts sending questionable messages to the international community about the ability of the USA to fulfill its obligations.

Choppy and sloppy best describes today’s equity moves, as dip buyers where present during the session but absent late in the day, as equities came off their highs. It now looks like the S&P 500 is on track to score its first monthly decline since January.

Zero Hedge called it this way:

While rising bond yields, Fed tapering, the delta variant and inflation help explain that, all of those will slow profit growth after rising earnings estimates and big beats helped fuel 2021’s stock rally until now with an always-optimistic eye for the ‘recovery’ and ‘return to normal’ that now seems ever further away.

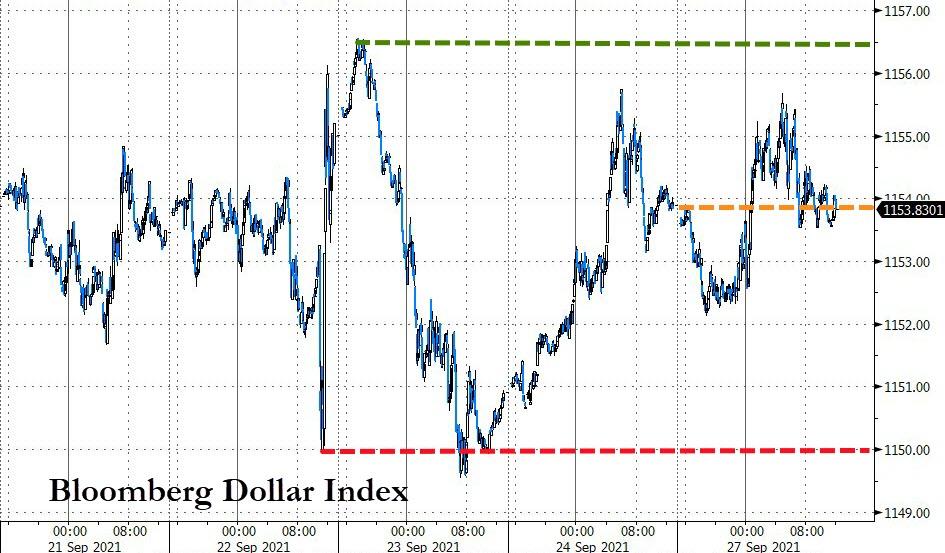

The US Dollar index, in the face of higher bond yields, continued its northerly path by registering its biggest 2-day jump since June, and it seems to be closing this September on a high note, just as it did in 2020.

Again, higher bond yields and a rallying dollar combined to take the starch out of Gold which, despite a mid-day rally, was not able to hold on and retreated -0.72%.

So far, the analog to 1987 is right on track, as Bloomberg’s chart shows.

There was no question that spiking bond yields were the destroyer of equity prices, with the major indexes tanking in unison right after the opening bell. A couple of rebound attempts were rebuffed, and the downward trend continued with the Nasdaq faring the worst with a loss of 2.83%.

Bond yields shot up with the 10-year touching 1.558%, its highest level since June, before retreating, while the 30-year catapulted above 2%. Amazingly, we saw the 10-year as low as 1.29% last week, and it had sunk as low as 1.13% in August. These are huge moves in that arena, which handed bond investors severe losses.

The reason for surging yields is increased conviction by traders that that the Fed will no longer talk but start tapering its $120 billion in monthly bond purchases “real soon.” What that means is that artificially suppressed rates due to tapering will now have to face the reality of a “true” market.

Added strategist Kathy Jones:

The market’s been steadily coming around to the reality that yields were awfully low relative to the fundamentals. Now the Fed is shifting, and everybody’s shifting their positions, all at once, as we tend to do.

Not helping matters was the ongoing budget showdown and the debt ceiling debacle, neither one of which exerted any positives towards the market. Uncertainty will keep a lid on any attempts to push equities higher.

Technical damage was done to the indexes, as Zero Hedge pointed out:

S&P broke back below 50DMA, testing 100DMA

Nasdaq broke back below 50DMA, testing 100DMA

Dow broke back below 50DMA and 100DMA

Russell 2000 broke back below 50DMA

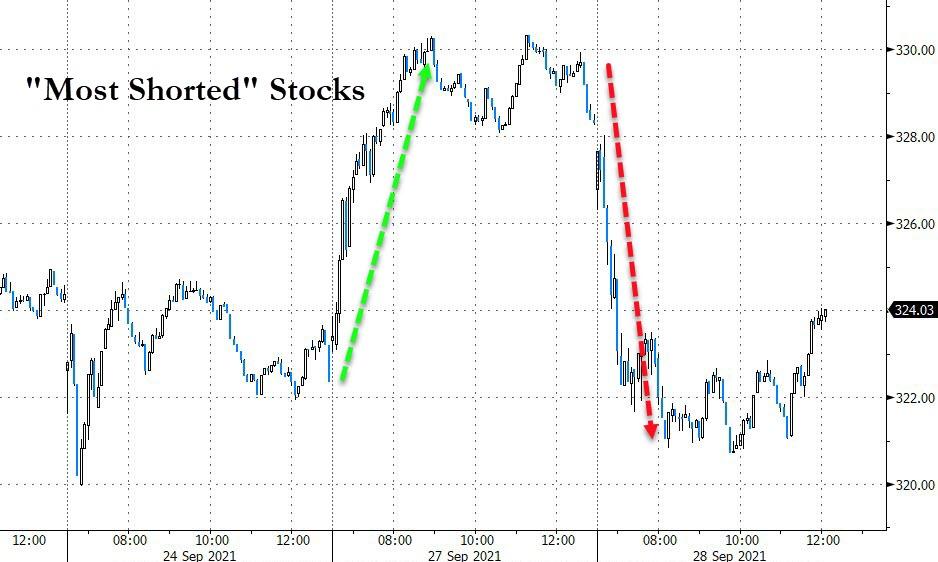

When appropriate, I mention short squeezes and how they are supporting the bullish meme. However, none of that was present today, as “the most shorted stocks” did what they are supposed to, namely head south, and consequently wiped out yesterday’s squeeze gains in the process.

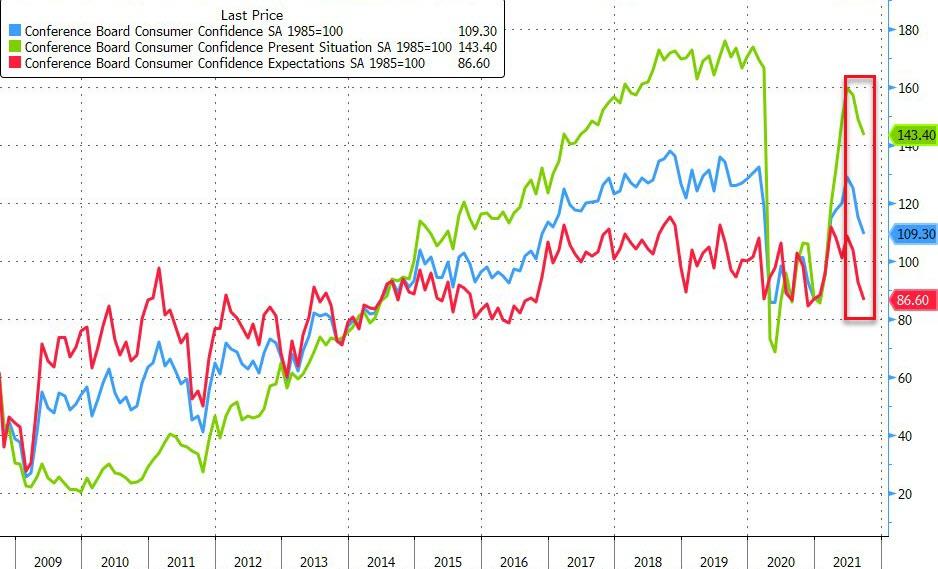

The US Dollar likes rising bond yields and continued its melt up and, during this course of action, slammed gold by over 1%. On the economic side, US Consumer Confidence plunged to 7-month lows, thus enhancing the sour mood on Wall Street.

An early bounce faded throughout the session with only the Dow maintaining bullish tendencies, while the S&P 500 and Nasdaq drifted aimlessly below their respective unchanged lines.

The final week of a volatile September caused this divergence in the major indexes with growth/tech stocks struggling as bond yields spiked, with the 10-year briefly breaking through the 1.5% marker and reaching its highest point since June.

The US Dollar rode the roller-coaster all day but stayed range bound and closed just about unchanged. Gold gave up its early gains and dipped back to the unchanged line, as surging bond yields took the starch out from any upward momentum.

The rise in yields benefited some sectors such as the financials (XLF) and the Commodity Index (CRB), each of which added +1.36% for the day. The value ETF RPV finally showed some signs of life by gaining an impressive +2.19%, but in that sector those kinds of advances can be wiped out in a hurry, as we have witnessed this year.

This week will not only mark the end of September, but on the menu are a host of items that can push markets around in a hurry. I am talking about the ongoing US Debt ceiling/government shutdown/infrastructure bill narrative, all of which might be coming to a head by the end of this week.

As ZeroHedge pointed out tongue-in-cheek, “maybe a 20% plus drop in stocks down to the level as shown in this chart may get the warring parties to agree on something.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}