- Moving the markets

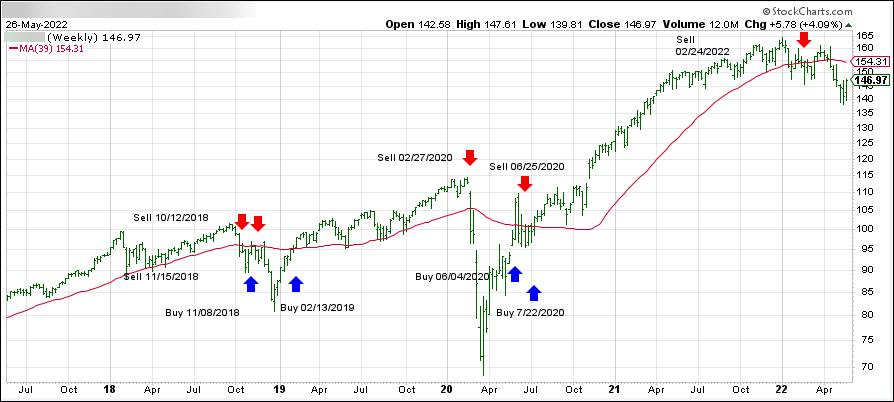

A roller-coaster month saw the S&P 500 dip into bear market territory (-20% from its recent high), before last week’s rebound rally pulled the index out of the doldrums. But that move ended today, with the major indexes simply running out of steam at the end of the session.

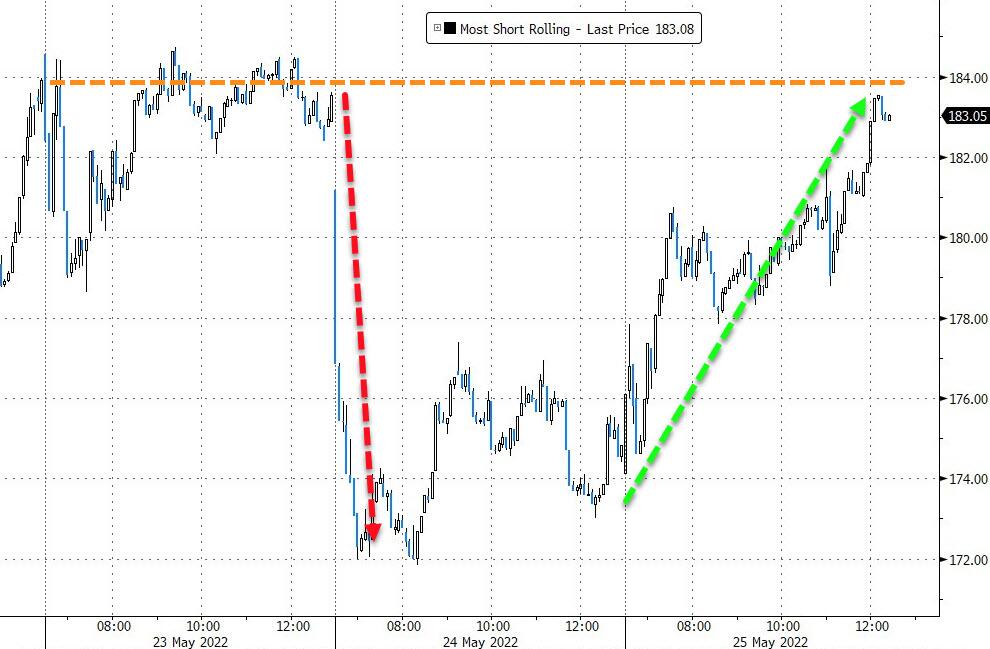

Inflation, monetary tightening and recession fears were at the center of the collapse, but a bear market rally, supported by a gigantic short-squeeze, assisted the S&P in its comeback to the breakeven point for the month.

Higher prices will be with us, as the markets took cues from the Eurozone, where inflation readings hit a record high for the seventh straight month by surging 8.1% in May. Crude oil prices contributed to today’s volatility and almost touched $120 intraday, before fading back to close at $115.

It was a “go nowhere fast” session, which ZH described like this:

30Y Bond unch-ish, S&P unch-ish, Gold unch-ish, Oil way-up, USD down, US Macro data total collapse…

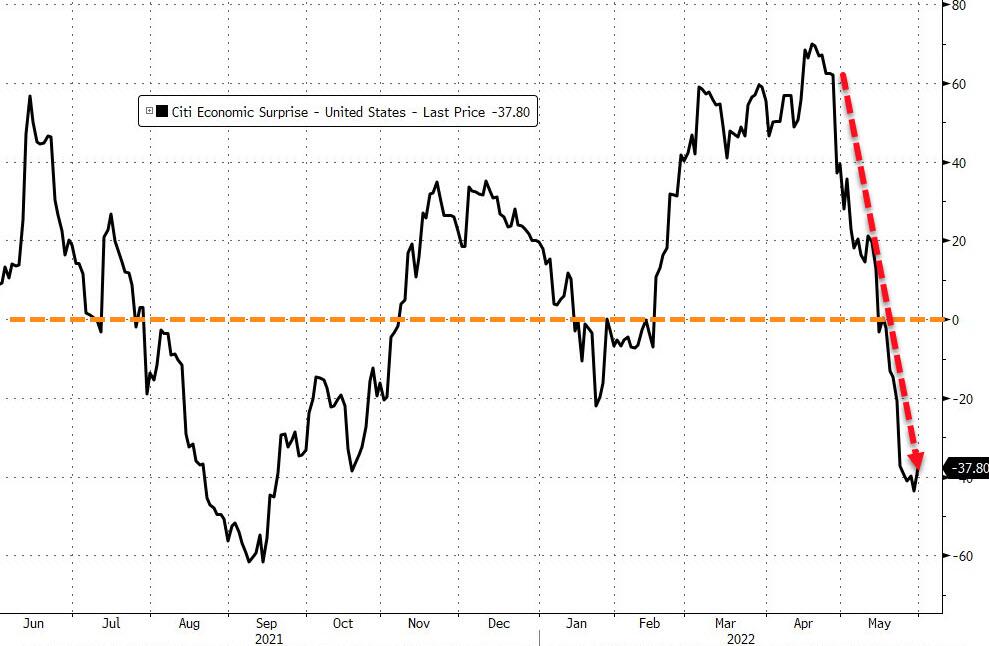

The US Macro Data collapse, outside the April 2020 crash (where the government basically shut down the entire economy), May’s 2022 fall was the worst since October 2008, when all capital markets froze up.

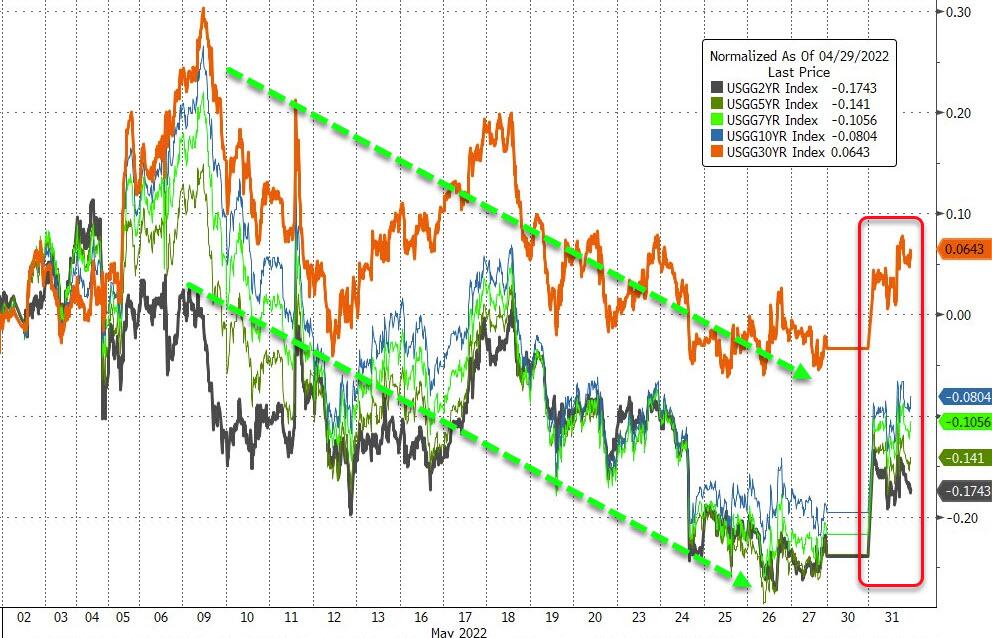

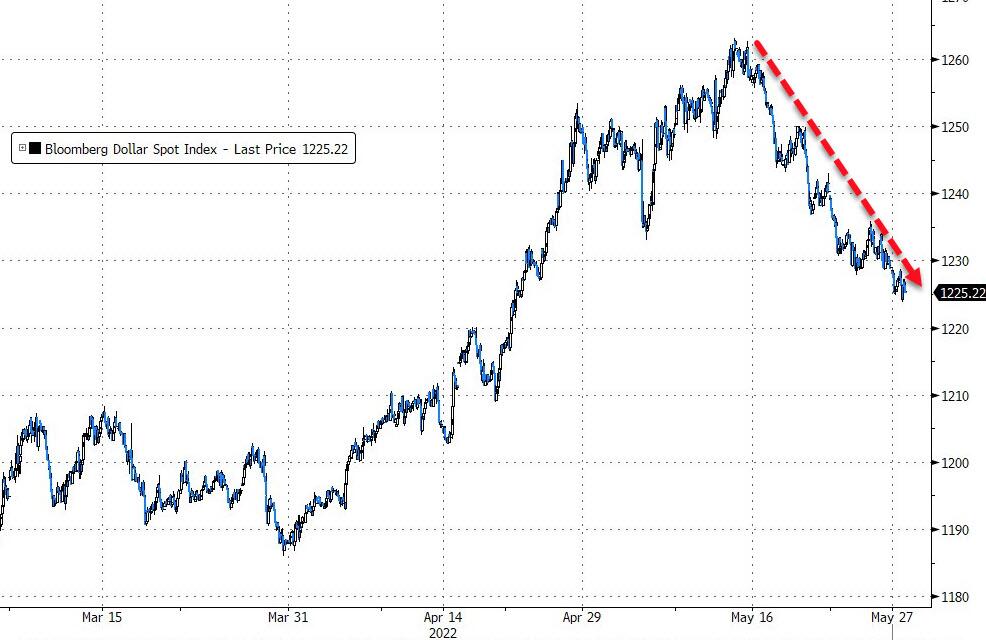

Bond yields were lower during May, as this chart by Bloomberg shows, but today’s turnaround may signal higher yields on deck again. The US Dollar slumped and saw its worst month in 2 years. Gold was down moderately for May and continues to struggle around its $1,900 level.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}