ETF Tracker StatSheet

You can view the latest version here.

WALKING BACK THE TOUGH TALK

- Moving the markets

It’s been a wild ride during the past 24 hours, since yesterday’s horrific CPI release, which indicated that we now have the highest inflation in 40 years. Not helping the markets were subsequent comments by the Fed’s mouthpiece Bullard, who called for 0.5% rate hike and an active sale of the Fed’s securities, thereby sparking panic, and helping the sell-off in the process.

Today, his remarks, which certainly added a sense of realism and urgency, were rebuked by various Fed speakers, and the media, as having been “immature” and “unprofessional.” So, damage control went into full swing and helped the major indexes early on to gain some footing, but in the end the sell-off persisted also due to war drums being beaten in the Ukraine.

{kind=link}

Added ZH:

A sudden slap to the face seemed to shock investors from their multi-month stupor, waking to the reality that The Fed is serious this time about raising rates and withdrawing liquidity. That realization, considering US equity valuations have never been higher (combined with a collapse in US consumer confidence) have many wondering just where (or if) these two lines will ever converge…

{kind=link}

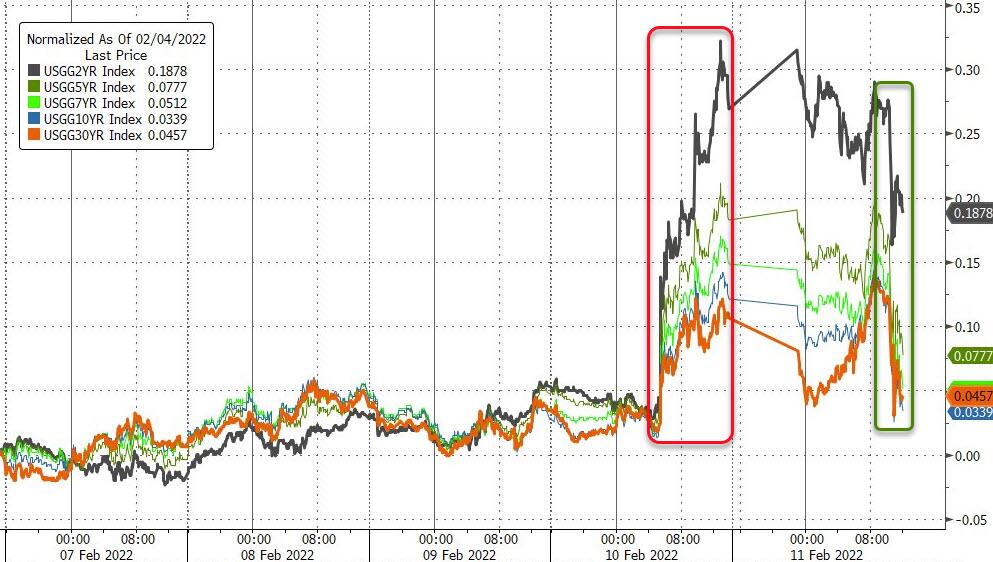

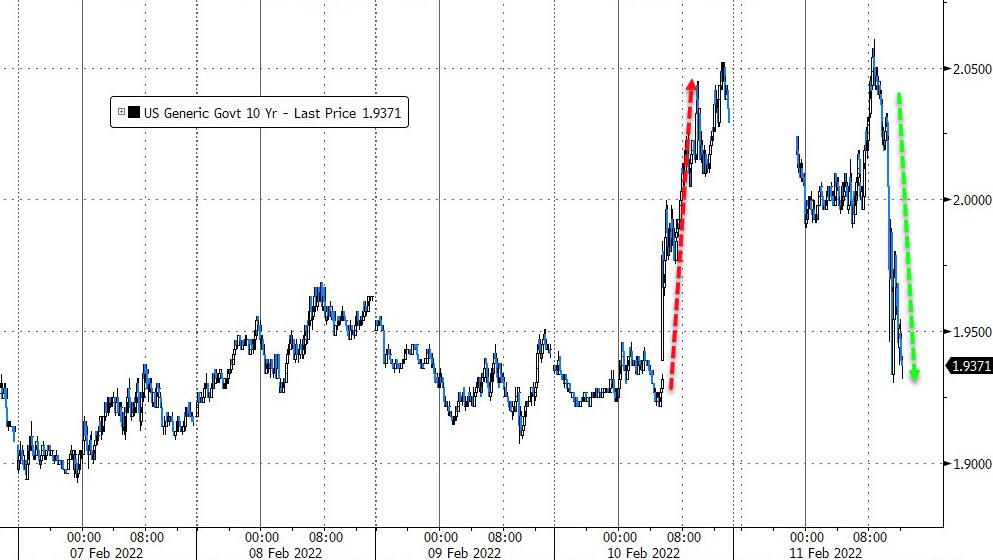

Bond yields were caught on a high speed rollercoaster with the 10-year up 15 bps yesterday and down 13 bps today, as rumors of Russia’s imminent invasion made headline news. The US Dollar rode the news cycle up and down and ended the week a tad higher.

{kind=link}

{kind=link}

{kind=link}

During all this turmoil, gold benefited and surged above the $1,860 level, its highest since Thanksgiving, according to ZeroHedge.

We are having a major power outage in my area, so I had to “wing” this report on my backup equipment.

{kind=link}

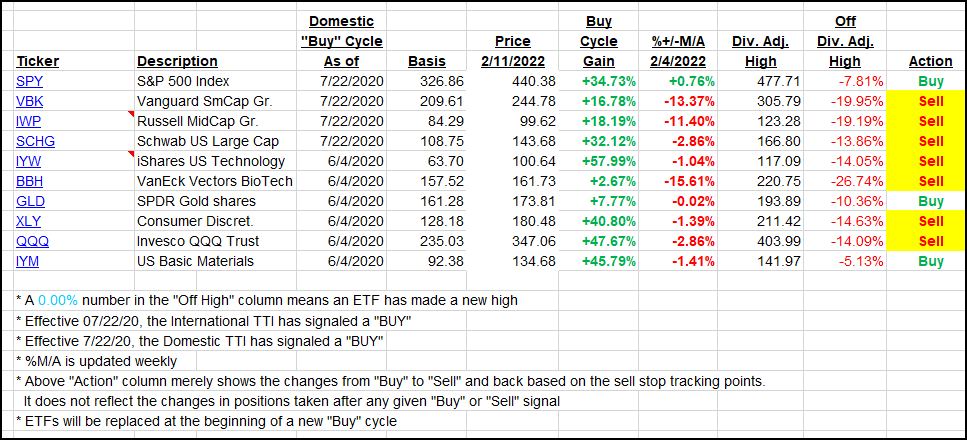

2. ETFs in the Spotlight

In case you missed the announcement and description of this section, you can read it here again.

It features some of the 10 broadly diversified domestic and sector ETFs from my HighVolume list as posted every Saturday. Furthermore, they are screened for the lowest MaxDD% number meaning they have been showing better resistance to temporary sell offs than all others over the past year.

The below table simply demonstrates the magnitude with which these ETFs are fluctuating above or below their respective individual trend lines (%+/-M/A). A break below, represented by a negative number, shows weakness, while a break above, represented by a positive percentage, shows strength.

For hundreds of ETF choices, be sure to reference Thursday’s StatSheet.

For this current domestic “Buy” cycle, here’s how some of our candidates have fared:

Click image to enlarge.

Again, the %+/-M/A column above shows the position of the various ETFs in relation to their respective long-term trend lines, while the trailing sell stops are being tracked in the “Off High” column. The “Action” column will signal a “Sell” once the -12% point has been taken out in the “Off High” column, which has replaced the prior -8% to -10% limits.

3. Trend Tracking Indexes (TTIs)

Our TTIs took a dive with the major indexes with the Domestic one now approaching a potential “Sell” signal again. If you follow along, be sure to tune in regularly.

This is how we closed 02/11/2022:

Domestic TTI: +0.58% above its M/A (prior close +2.04%)—Buy signal effective 07/22/2020.

International TTI: +4.22% above its M/A (prior close +5.12%)—Buy signal effective 07/22/2020.

Disclosure: I am obliged to inform you that I, as well as my advisory clients, own some of the ETFs listed in the above table. Furthermore, they do not represent a specific investment recommendation for you, they merely show which ETFs from the universe I track are falling within the specified guidelines.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly or get more details.

Contact Ulli