- Moving the markets

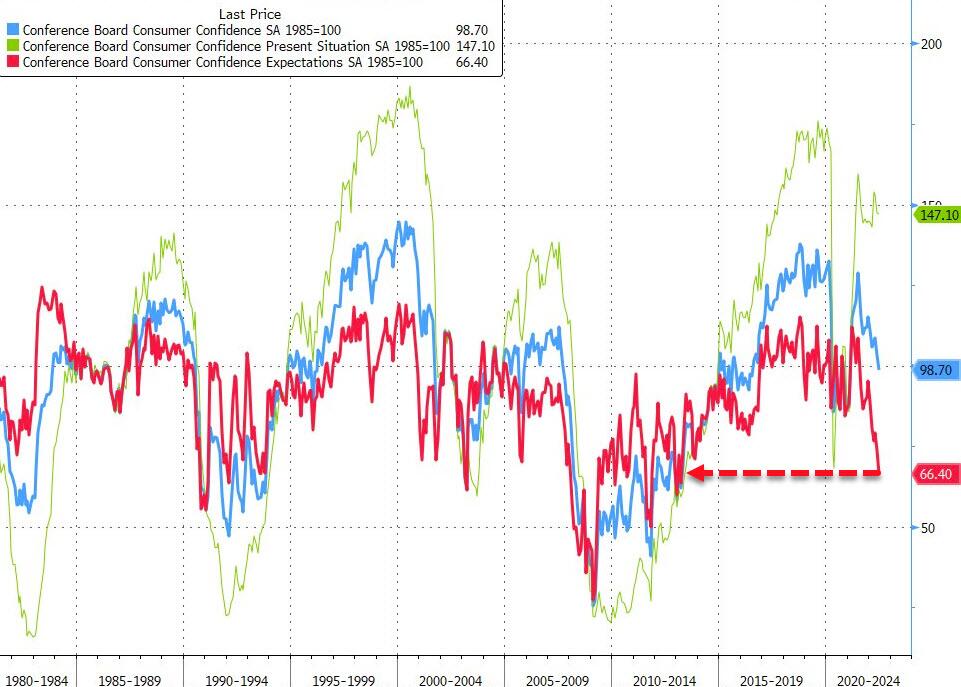

Despite an early bounce, the major indexes hit the skids due to disappointing economic data. The reversal started with the release of the Consumer Confidence Index, which crashed to a reading of 98.7 in June from a prior 103.2 vs. an expected 100.0.

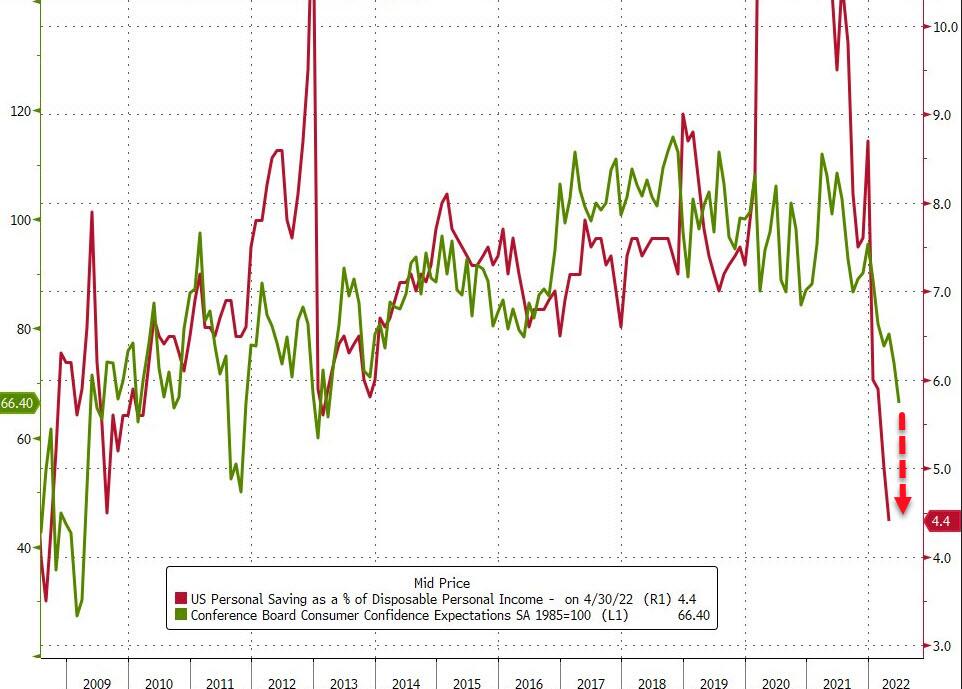

Additionally, as ZeroHedge reported, the actions of Americans, dumping their savings to afford the cost of living, suggests that Conference Board Expectations have further to fall. Finally, for the first time since 2019, “soft” survey data has dropped below “hard” real economic data, while “Hope” is getting hammered.

Ouch! None of this bodes well for our economic future, and especially for the prospect of increased earnings, and therefore stock prices, in an environment where 67% of economic growth is generated by consumers, which appear to be tapped out.

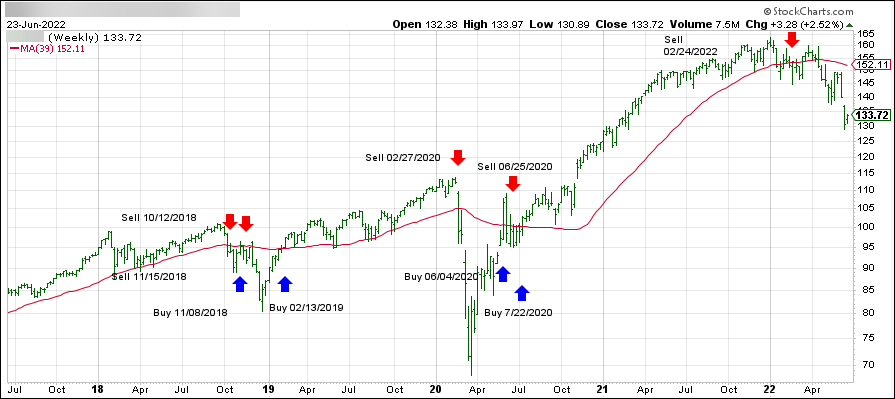

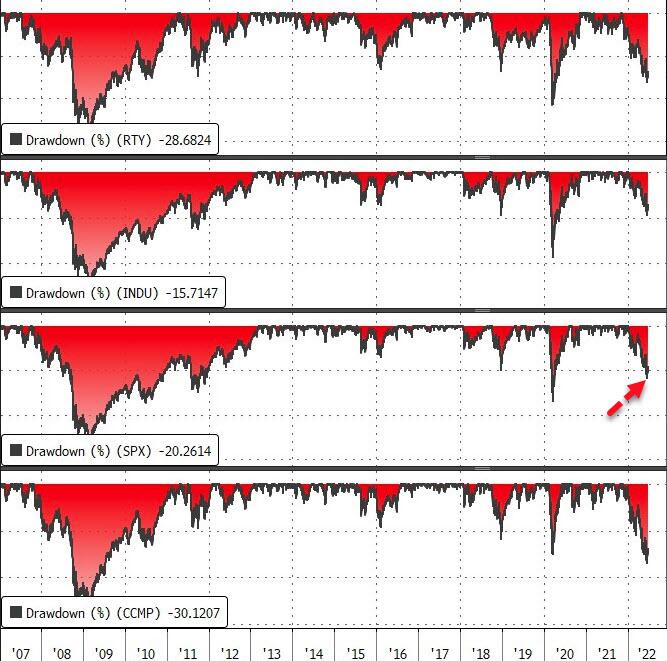

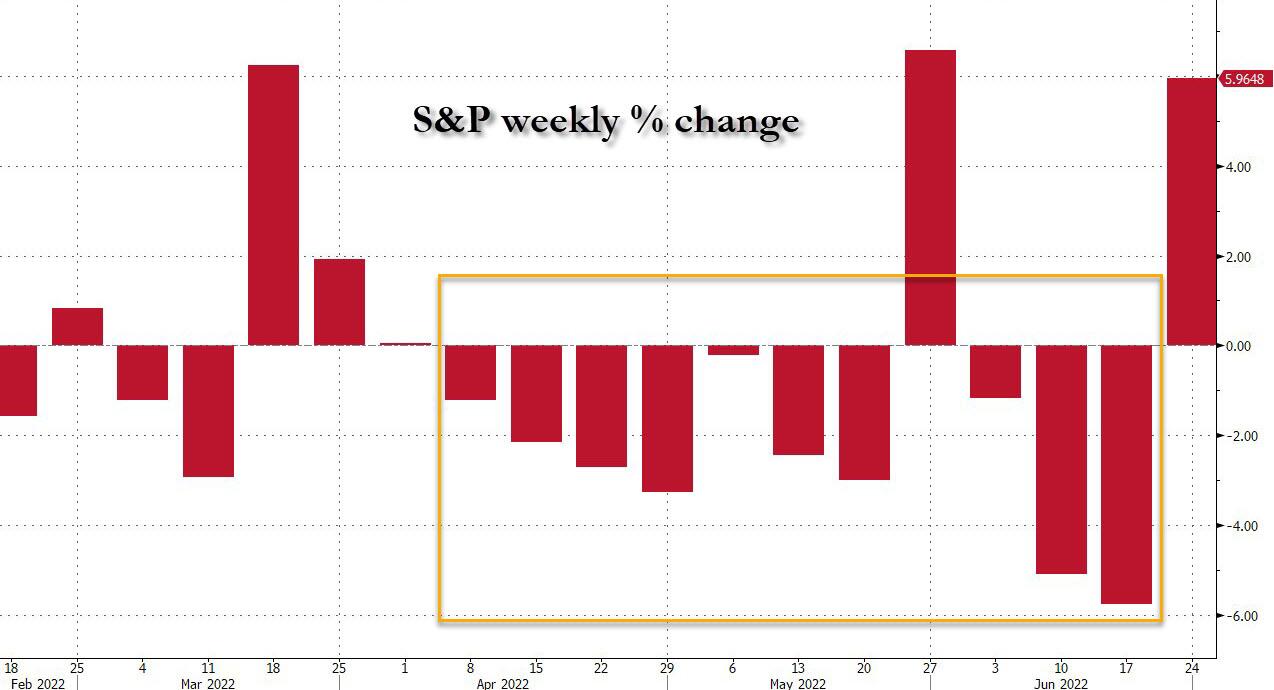

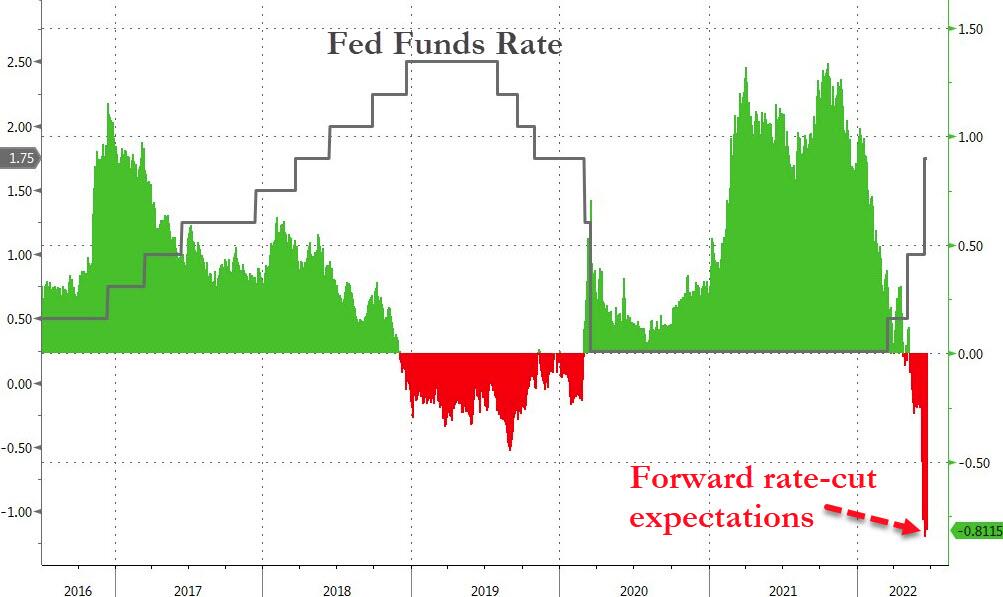

As a result, the major indexes got spanked with the S&P 500 dropping back into bear market territory, after just having climbed out of it last Friday. Hawkishness dominated the tone of the market, as rate hike expectations climbed again.

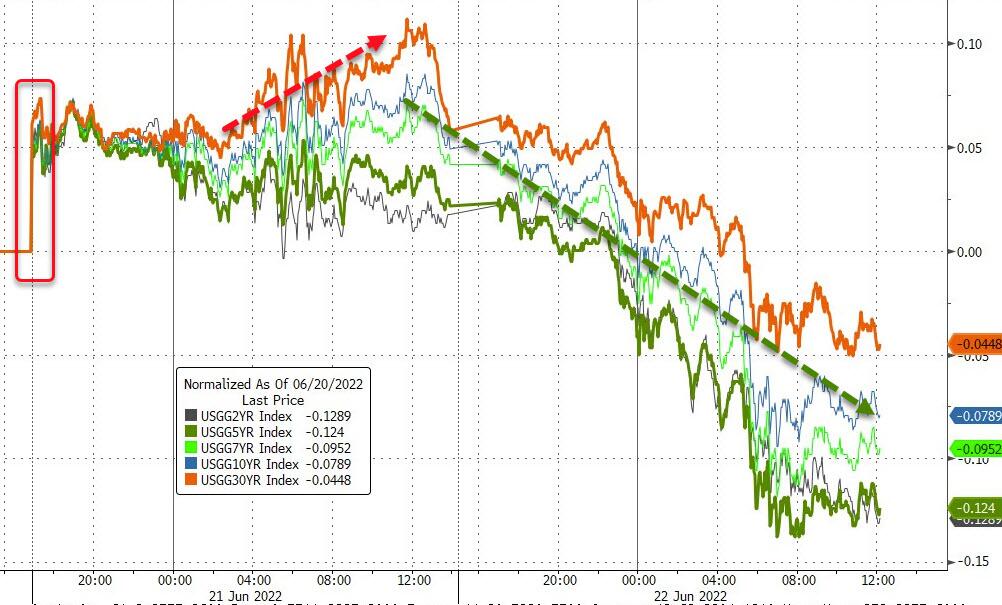

Bond yields ripped and dipped and ended the session just about unchanged, but the US Dollar recovered from its recent weakness and rallied. Gold had a great overnight session but was sold later with the precious metal dipping slightly into the red.

With two more trading days till the end of this horrific quarter, will the bulls be able to recoup some of their losses?

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}