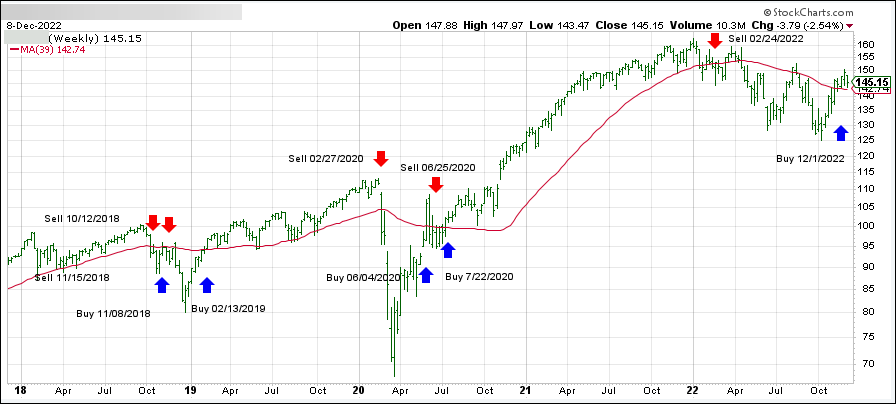

- Moving the markets

While moderate bullish sentiment dominated market direction throughout the day, traders decided to shift upward momentum into overdrive during the last hour of the session, thereby pushing equities sharply higher.

The major indexes sported solid gains in the end, indicating that tomorrow’s CPI number is expected to come in lower than had been assumed. Should that be the case, we will see the bullish theme grow stronger and provide us with the much longed-for Santa Claus rally.

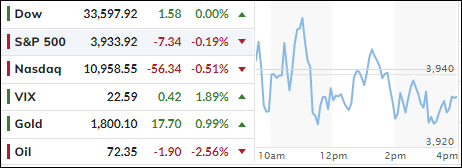

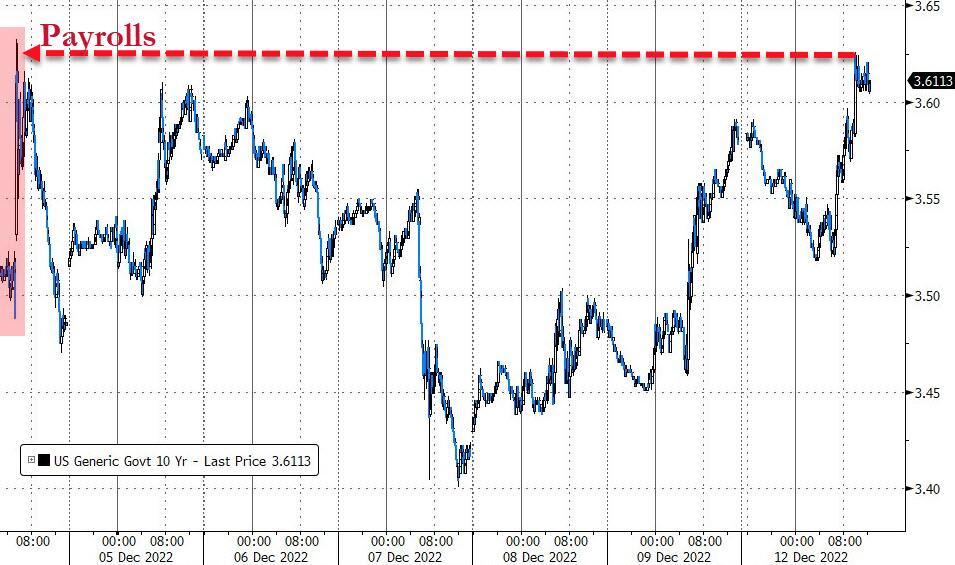

Bond yields jumped with the 10-year adding 12 bps to close at 3.62%. Rate trajectory expectations rose, as ZeroHedge pointed out, with the terminal rate now back up to 5%.

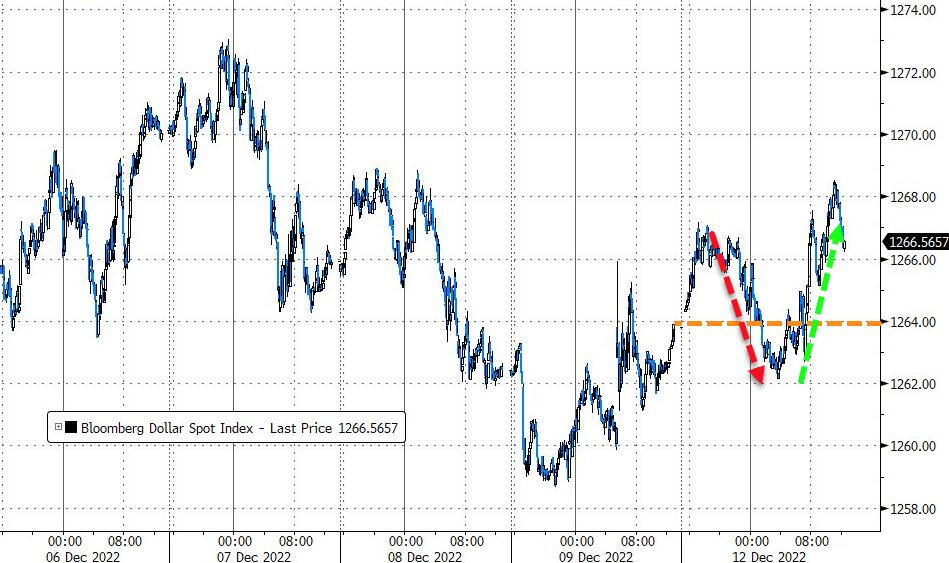

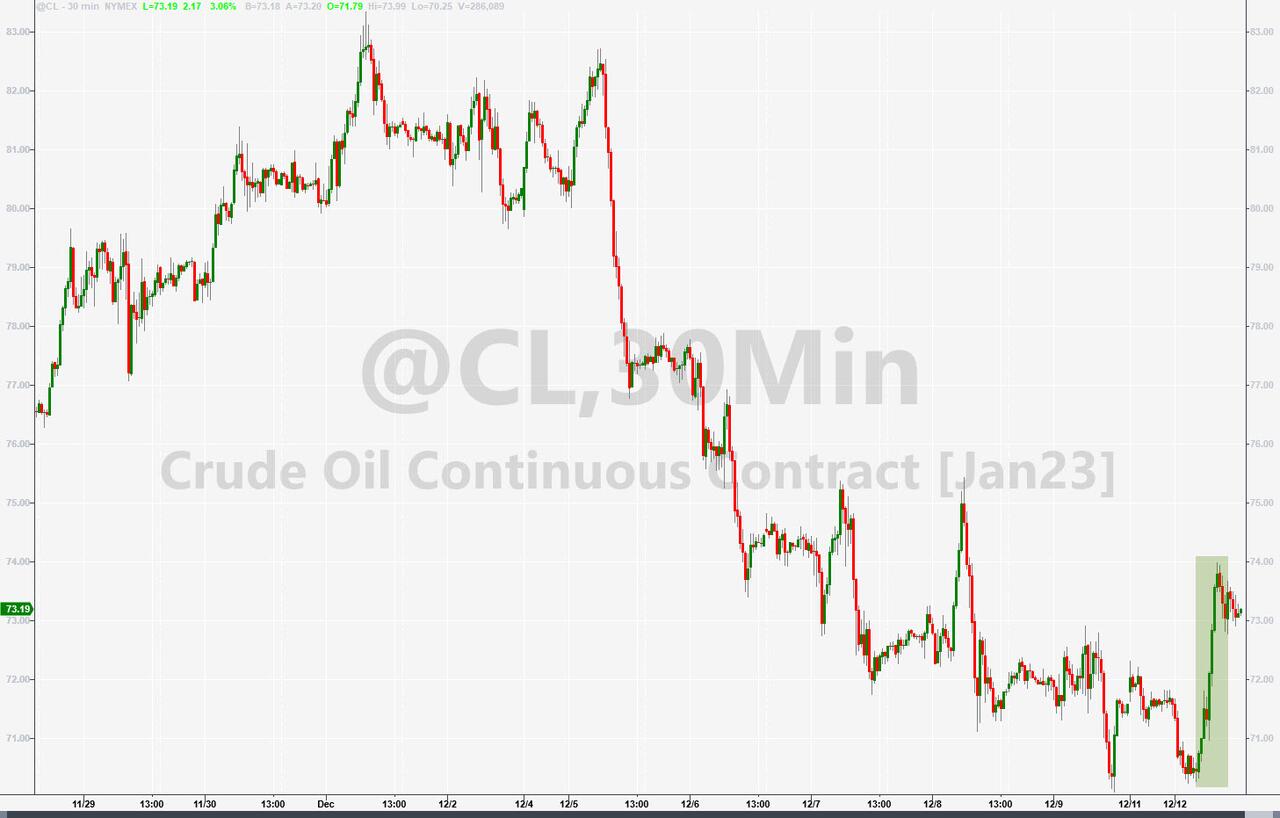

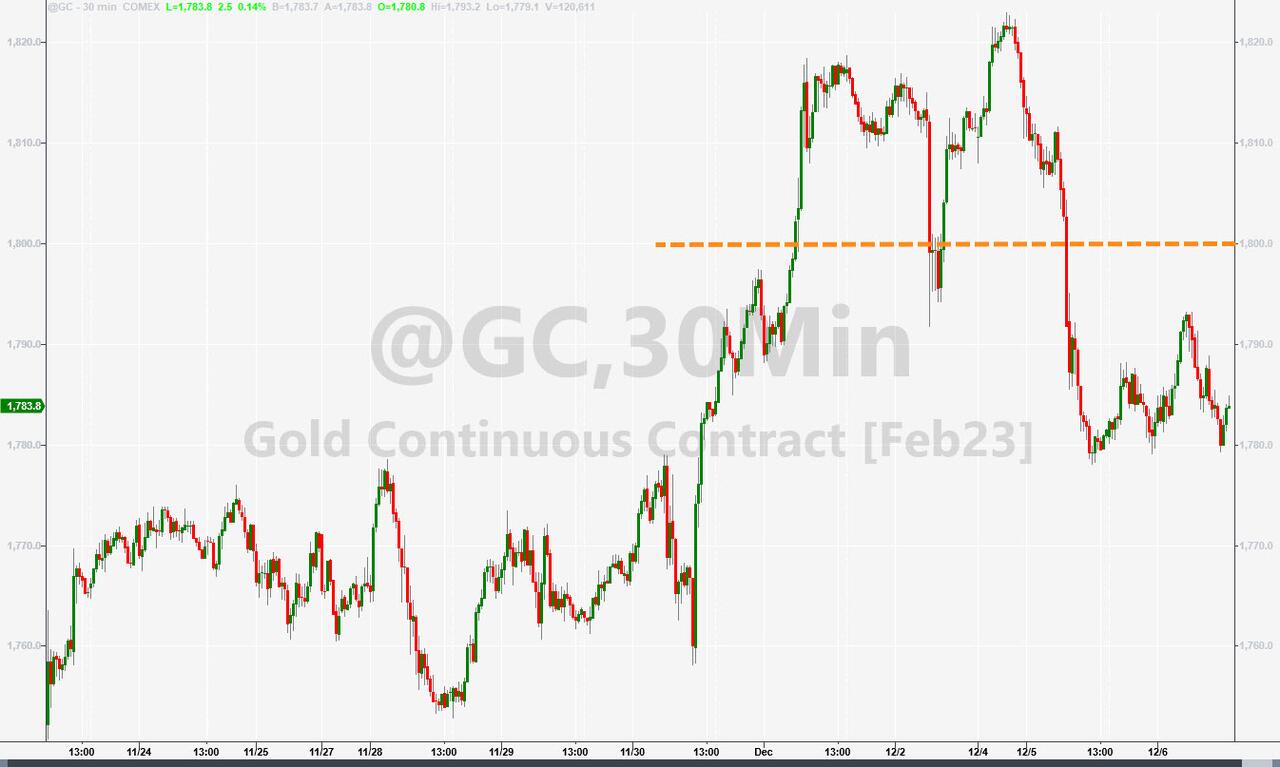

The US Dollar rode the rollercoaster but managed to eke out a small gain, Crude Oil rebounded after the recent drubbing, and Gold lost its $1,800 level by a small margin.

All eyes are on tomorrow’s CPI release and Wednesday’s FOMC meeting, after which Fed head Powell will likely again elaborate his hawkish stance—higher rates for longer—which may not go over well with the Wall Street crowd, because they have almost desperately anticipated a pause or pivot in rate policy.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}