- Moving the markets

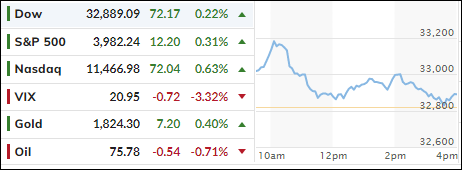

Despite a good midday effort, at which time bullish sentiment exploded to the upside, the bounce turned out to be nothing more than a head fake, with two out of the three major indexes slipping back into the red—not only for the day but for the month as well.

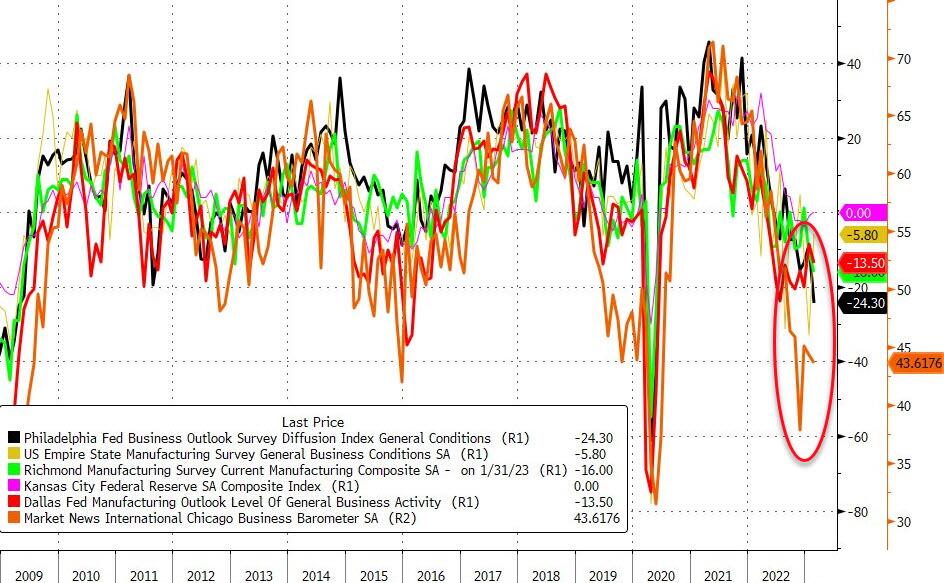

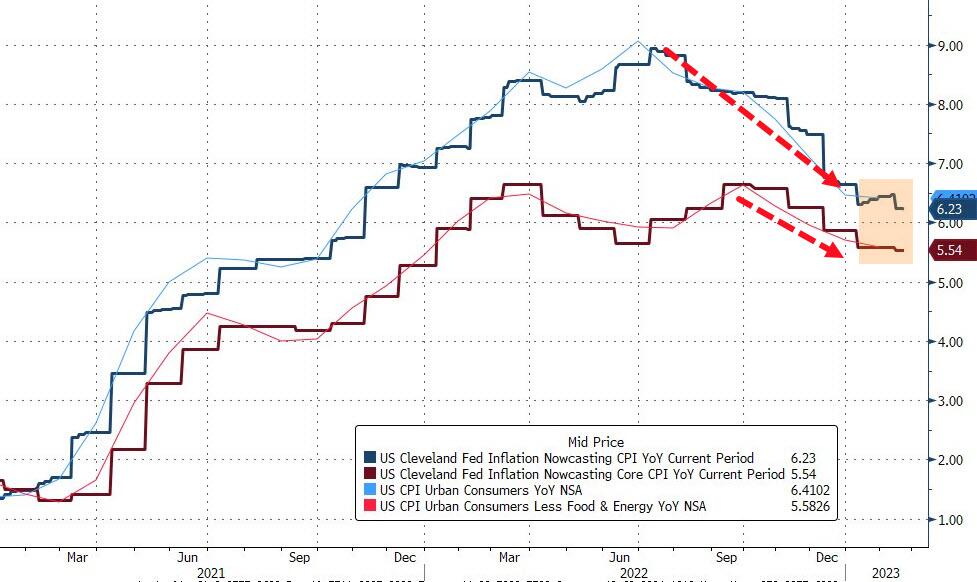

Again, economic data points were negative, with this spaghetti menu of widely followed indicators showing one thing, namely that the direction is “down” with most of them remaining in contraction mode.

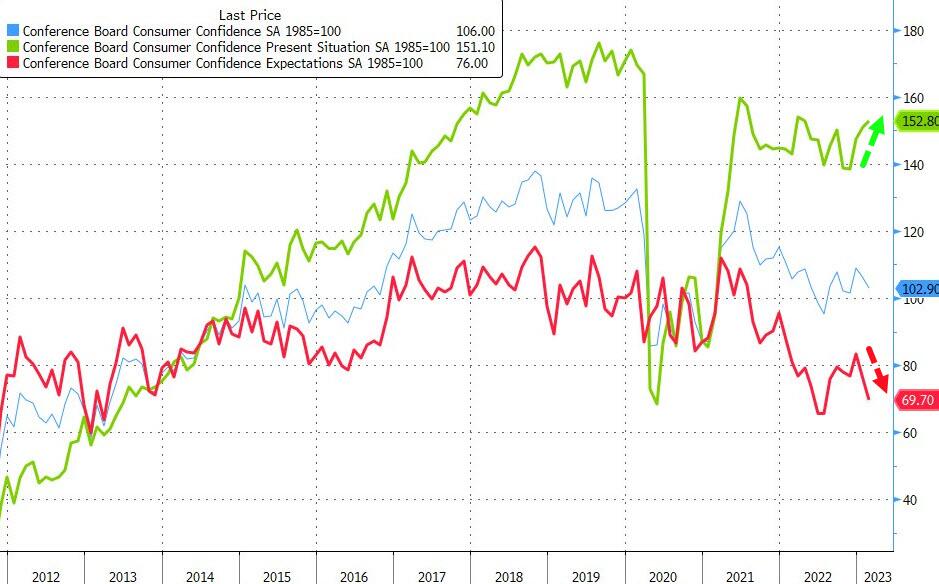

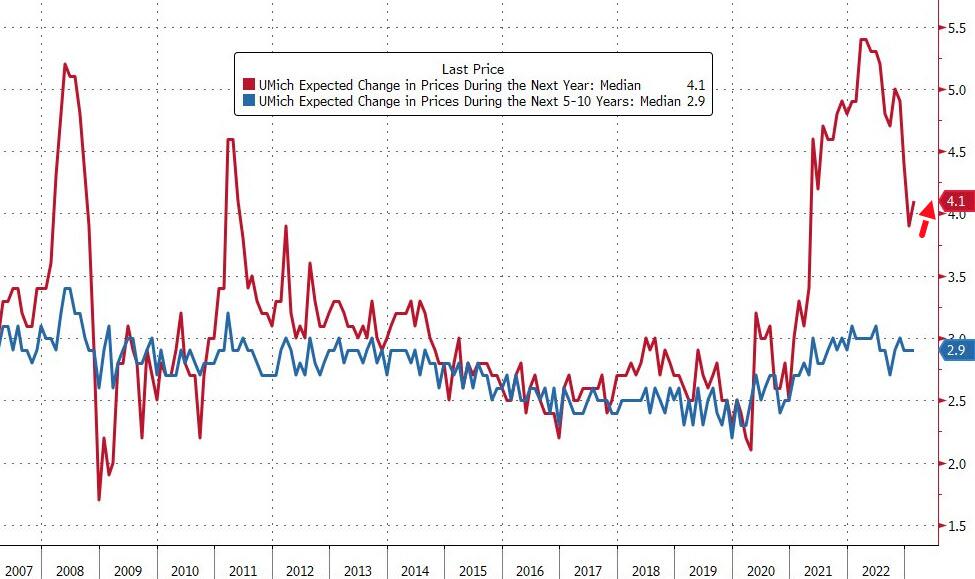

Also, US Home prices plummeted for the 6th straight month in December, which showed the annual growth to be the weakest since July 2020, as ZeroHedge pointed out. But Consumer Confidence expectations improved a tad in February, while inflation rate expectations went the other way and turned higher.

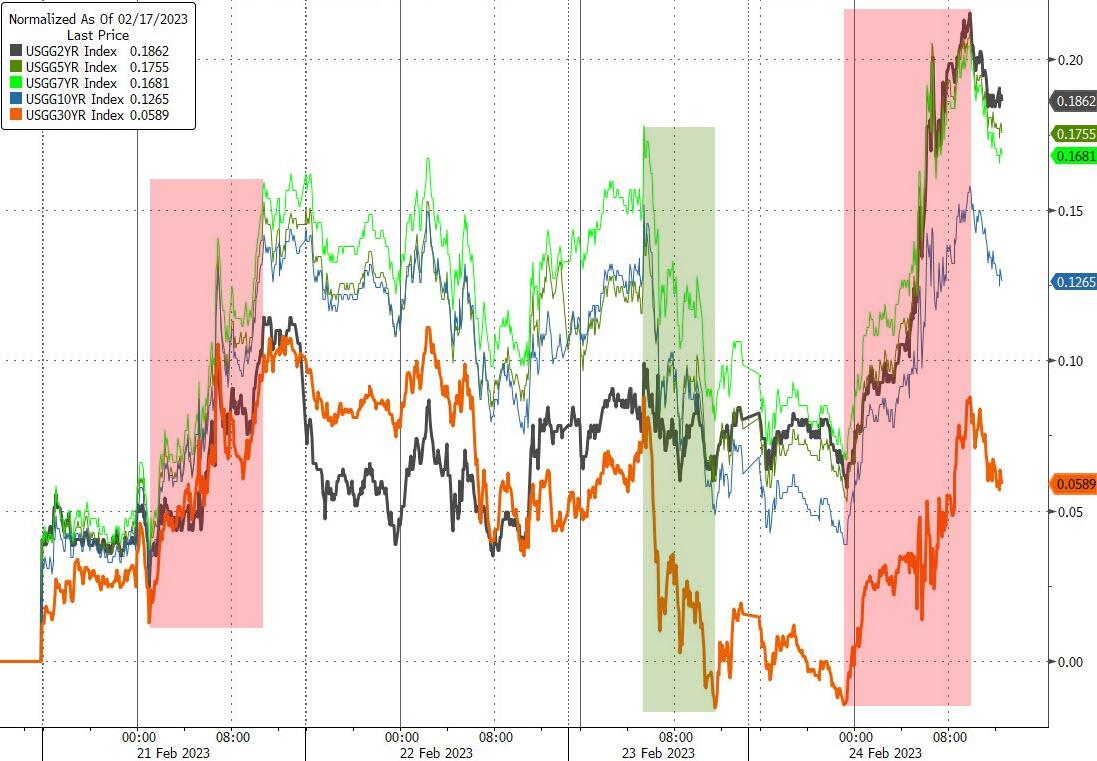

In the end, the weakness in equities can be attributed to one thing, and that is the rally in bond yields with the 2-year gaining almost 60bps, while the 30-year “only” added 30bps, both of which are huge moves and confirm that the Fed’s aggressive inflation stance continues.

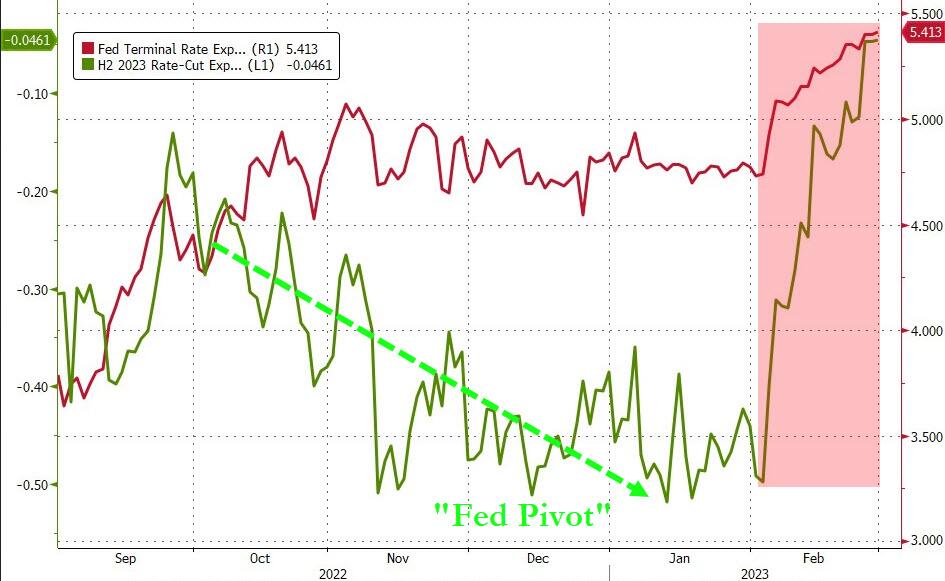

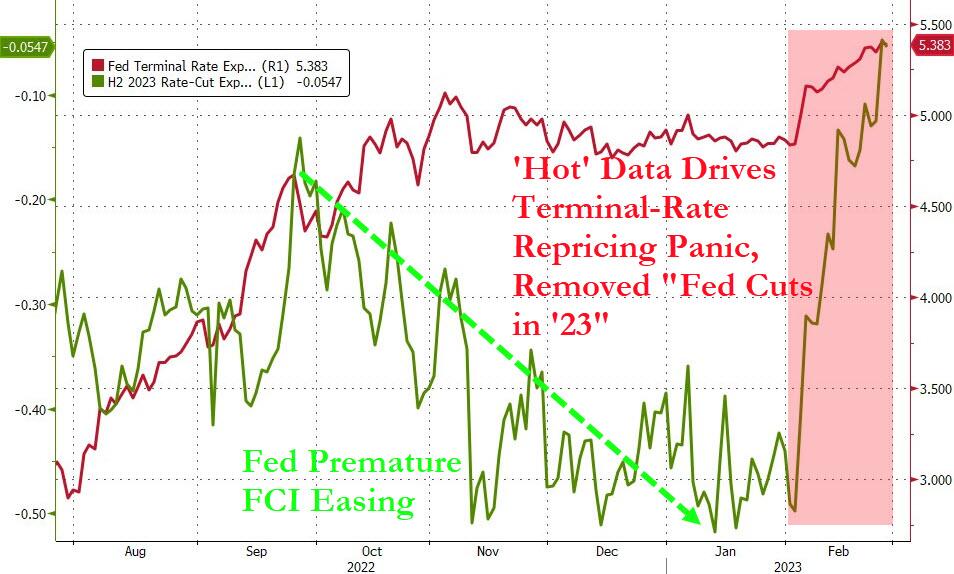

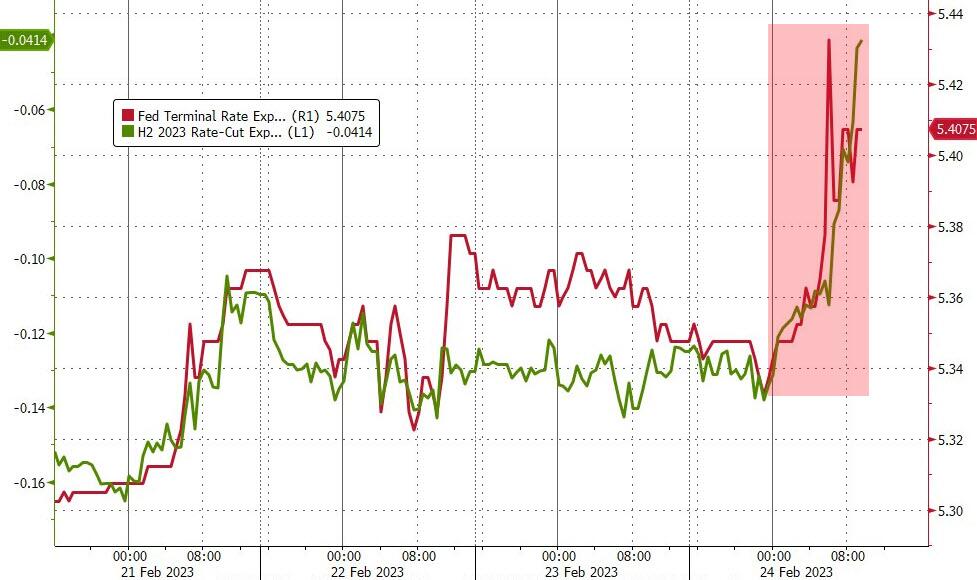

Traders had to swallow that bitter pill, which is also shown in this terminal rate expectation chart, with that number (red line) now approaching 5.5%, while rate cut expectation have simply disappeared, as the Fed pivot promoters now have joined the hawkish crowd.

While the 10-year bond yield is still struggling to break above the 4% level, all action was in the short-term 2-year yield, which broke back above its November highs to reach a point last seen in July 2007. Amazing!

The US Dollar, after struggling in January, surged with a vengeance, thanks to higher rates, and is now back in the green YTD. As a result, Gold moved the opposite way and gave back its January gains.

As we move into March, equities will have a hard time finding a bottom, as continuously higher rates will present a formidable headwind, that is if that trend continues.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}