Below, please find the latest High-Volume ETF Cutline report, which shows how far above or below their respective long-term trend lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s StatSheet and includes 312 High Volume ETFs, defined as those with an average daily volume of more than $5 million, of which currently 111 (last report: 93) are hovering in bullish territory. The yellow line separates those ETFs that are positioned above their trend line (%M/A) from those that have dropped below it.

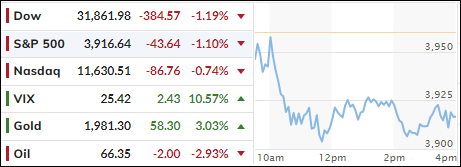

The state of the US Banking sector remains precarious, as confidence has not been restored causing the major indexes to take another dive. Maybe traders finally got the idea that, not just covering $250K of depositor’s money in a failed bank, but to make everybody whole, has unintended consequences.

After all, there are some $30 trillion deposits lingering in US banks. Does that mean, with the FDIC apparently having been pushed aside and/or put out of business, that the Fed will now cover the full monte? If so, batten down the hatches, because the subsequent inflationary impact will make your head spin.

So much for my rant…

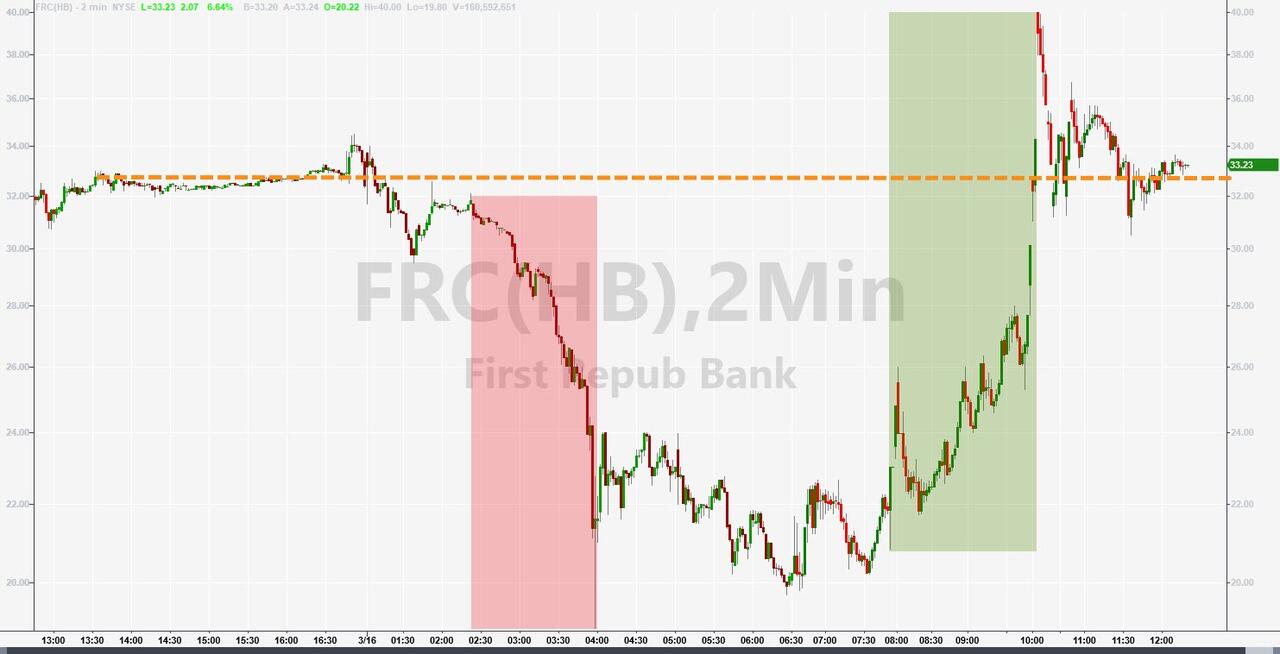

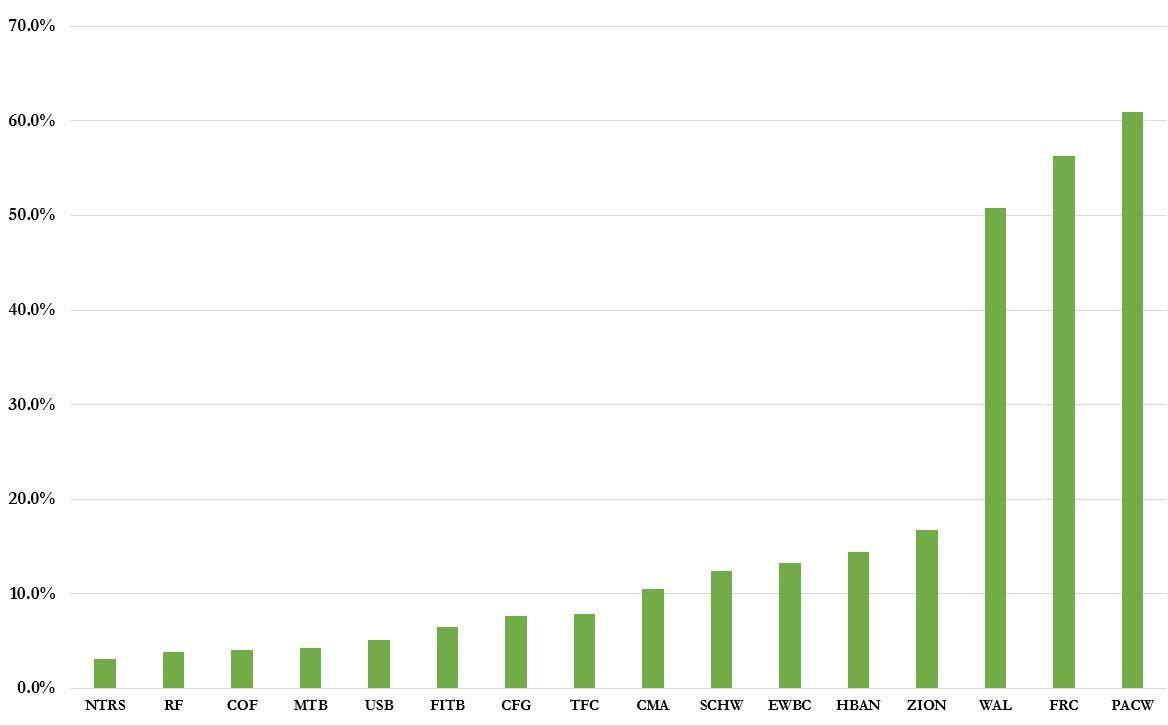

First Republic bank took another hit and dumped 32% bringing the total loss for the week to more than 70%. Looking at the bigger picture, the Regional Banking ETF (KRE) slid 6% today and is down 14% for the week.

The latest banking cockroach on deck, Credit Suisse, was down some 5% despite its promised $54 billion lifeline from Swiss National Bank. Hmm…

As I said before, these are just the first dominos to fall, since every bank is in a similar situation of sitting on big losses in their long-term bond portfolios, which got clobbered, as the Fed went on its interest hiking spree. As demand for withdrawals increases, such upside-down holdings need to be liquidated at any cost, as was the case with SVB.

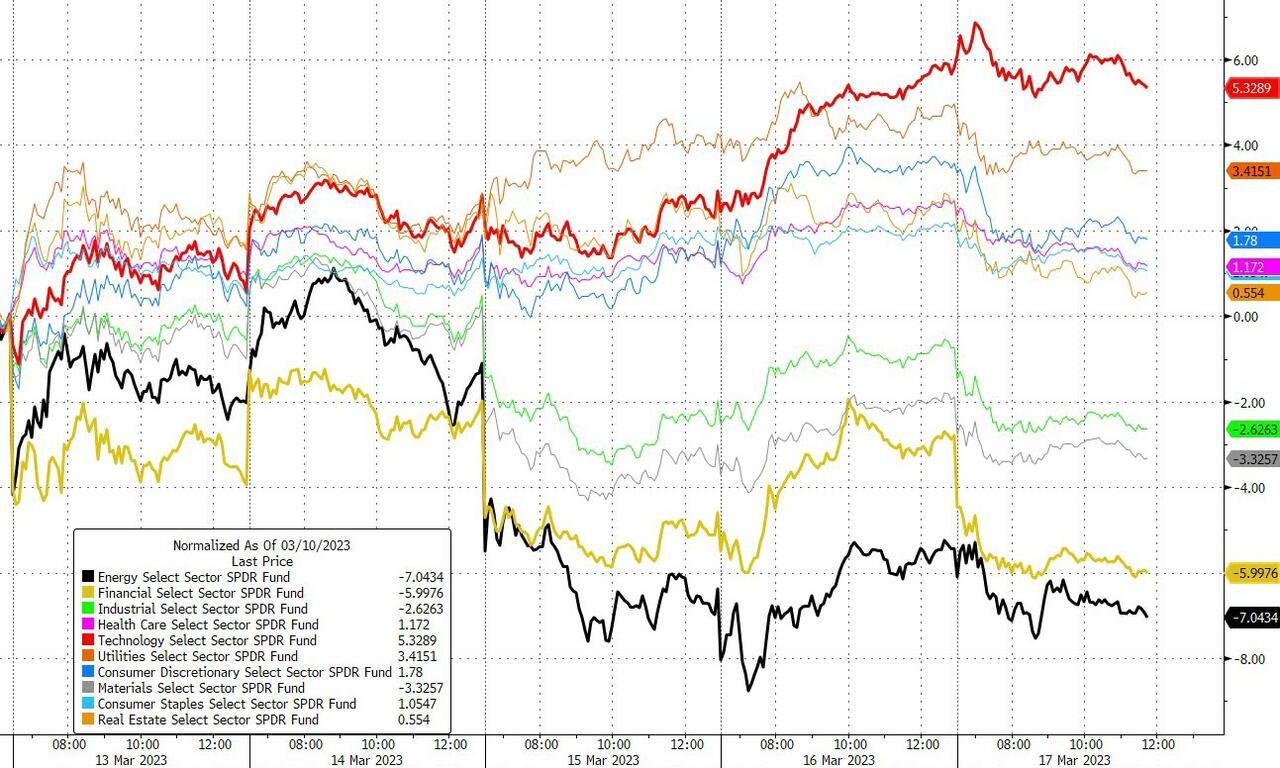

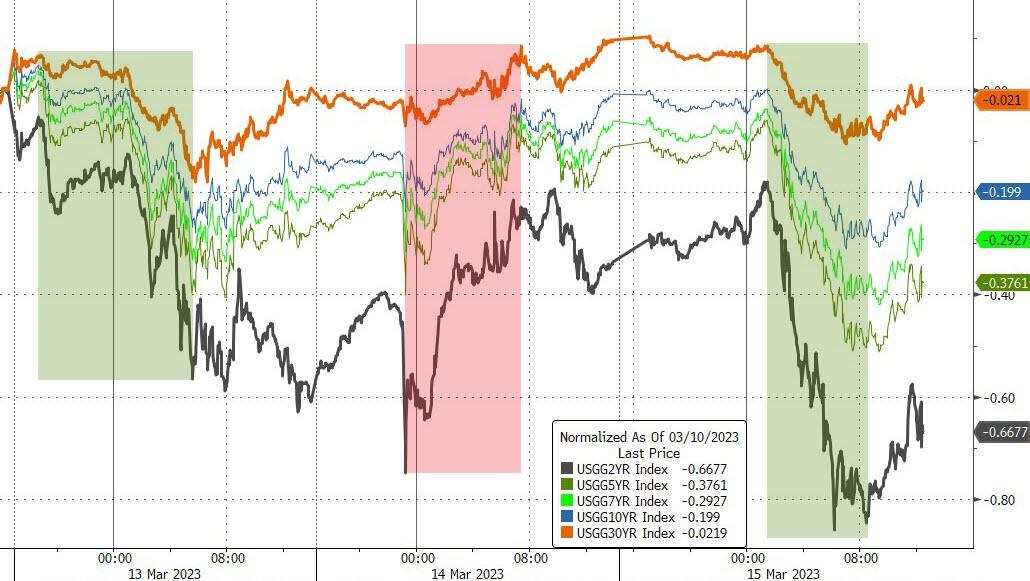

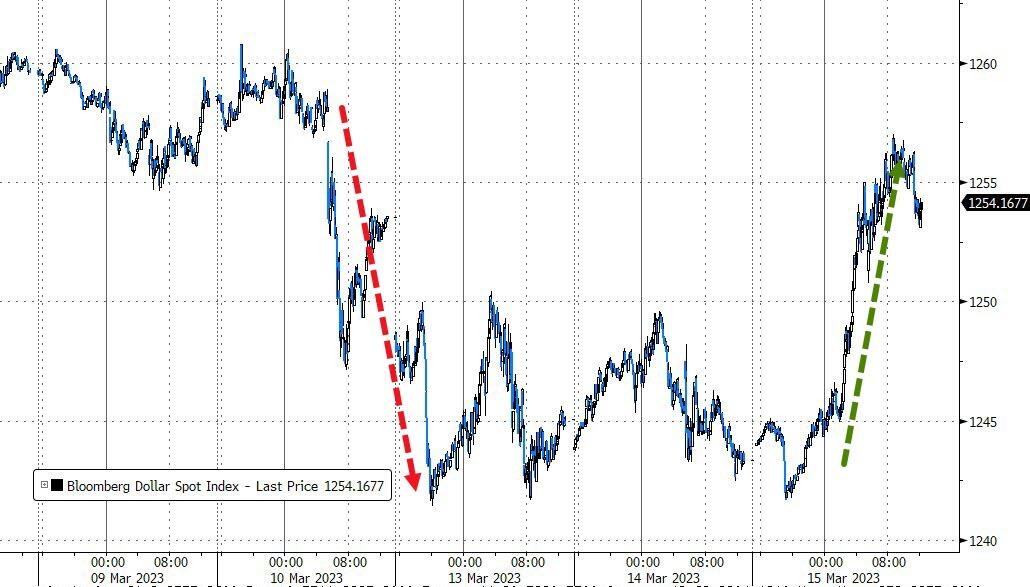

Energy and Financials were the weaklings of the week, while office REITS got slaughtered as did European bond yields. It seems that something has broken somewhere in the financial system, with worldwide impact, as even the US Dollar closed lower for the week.

This was confirmed by smart money moving into Gold, with the precious metal adding another 3% for the day. It has now reached its highest level since April 2022 and is closing in on the $2k level.

Today, we saw options expiring and, with that uncertainty out of the way, we may see a rebound next week, at least until the Fed meets on Wednesday and regales us with their latest wisdom on interest rates. That will determine if the bulls can win this current tug-of-war against the bears.

1. From the universe of over 1,800 ETFs, I have selected only those with a trading volume of over $5 million per day (HV ETFs), so that liquidity and a small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and 2), are made based on the respective TTI and its position either above or below its long-term M/A (Moving Average). A crossing of the trend line from below accompanied by some staying power above constitutes a “Buy” signal. Conversely, a clear break below the line constitutes a “Sell” signal. Additionally, I use a 12% trailing stop loss on all positions in these categories to control downside risk.

3. All other investment arenas do not have a TTI and should be traded based on the position of the individual ETF relative to its own respective trend line (%M/A). That’s why those signals are referred to as a “Selective Buy.” In other words, if an ETF crosses its own trendline to the upside, a “Buy” signal is generated. Here too, I recommend trailing sell stop of 12%, or less, depending on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

1. DOMESTIC EQUITY ETFs: BUY — since 12/01/2022

Click on chart to enlarge

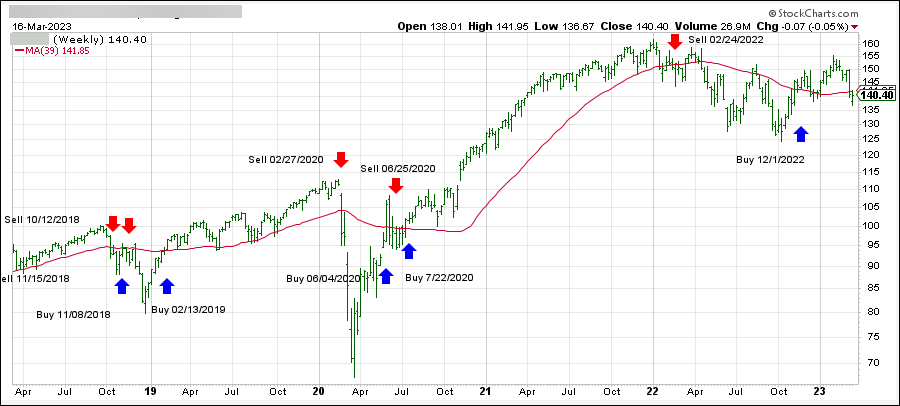

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) has reclaimed its long-term trend line (red) by -0.82% and remains in “Buy” mode for the time being.

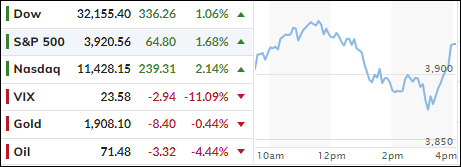

After an early dump, the major indexes shifted in reversal mode not because the banking crisis had passed but merely because a temporary fix had been found.

A consortium of 11 of the largest US Banks combined forces and agreed to a historic $30 billion unsecured deposit injection in First Republic Bank (FRC). While this is merely a band aid, and does not address how to deal with future cockroaches, it was enough to not only pull equities out of the doldrums and propel them to a solid green close, but it also wiped out FRC’s recent losses.

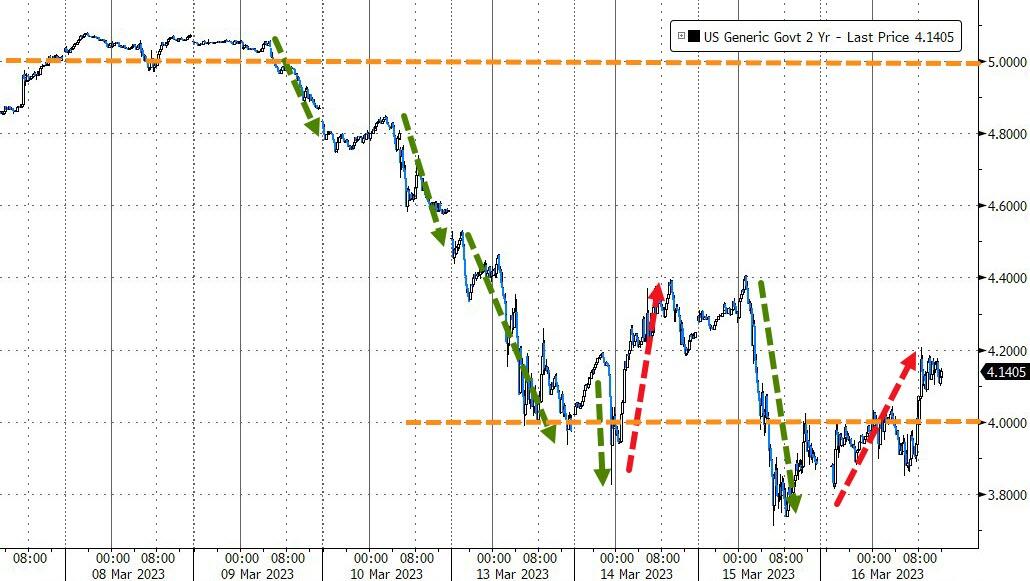

Bond yields rose with the 2-year climbing back above its 4% level. The US Dollar lost its recent upward momentum, while Gold slipped a tad but held on to its $1,900 level.

Reader Keith submitted an interesting question that might be of concern to you as well given the current banking crisis, of which we are only in the beginning stages—at least in my opinion:

Q: I’m a long-time subscriber to your daily emails and am curious if you could share with me and your readers, what you recommend as “safe,” given the crack that has started in our banking system.

Safely on the side has always meant short-term treasury notes and cash but if we have an unstable bank, where is our money safe?

A: I like to split the answer into two parts, since we are dealing with separate scenarios, namely investment risk and economic risk.

When you invest via a broker, and follow my Trend Tracking approach, you expose yourself to the fluctuations of equities and bonds. Once we receive a “Sell” signal, the objective is to eliminate “market risk,” since the downside danger has increased to a point where your portfolio could experience a serious decline. At that very moment, we are only concerned to move proceeds to the safety of a money market fund.

Economic risk comes into play when we start to see bank failures and bailouts, such as we are witnessing now, with a potential recession looming, which can affect your finances in a different way.

To protect against those uncertainties, you need to invest a portion of your assets into an area where 3rd party risk is eliminated. There are not too many choices, but I like gold and silver eagles in your own possession and not in a safety deposit box. You also should have some physical cash, in case the ATMs go down and, if you are so inclined, own some crypto currencies, but you must have them in your own private wallet and not on an exchange.

We are living in uncertain times and being prepared along these lines might help you to better deal with what might be coming at us in the future.

As I posted before, once you find a cockroach in your house, you can be assured it’s not the only one. That is akin to a banking system that got addicted to low bond yields and is now trying to deal with and operate in an environment of higher rates, which means that one banking failure can rapidly spread.

We did not have to wait too long, because today, Credit Suisse (CH), a bank with a large international presence and considerable investments in the US stock markets stumbled toward a collapse.

I had to laugh out loud when a few days ago the banking giant announced that it had found “certain material weakness in our internal control over financial reporting” for the past couple of years. One look at a long-term chart tells you that this firm has had issues for almost a decade.

Throwing gasoline on that fire was the Saudi National Bank, CH’s largest investor, by announcing they could not provide any more funding. Ouch! Swiss National Bank then stepped up to the plate stating that “they will provide liquidity, if necessary,” which stopped the bleeding for the time being.

Still, I think Silicon’s bank turmoil was only the first domino to fall, and it looks that Europe will have to deal with its own crisis, as their banking stocks crashed 7% today. For sure, this is only the beginning, and things will likely spread around the globe.

The major indexes slumped all day but managed to limit their early losses, yet the banking bailout plan still left the regionals sharply in the red since Friday.

Bond yields dropped with the 2-year dumping to its lowest since September 2022, as ZeroHedge pointed out. Fed rate-hike expectations crashed again with the markets pricing in over 100bps of rate-cuts by the end of this year.

Interesting was the divergence between the US Dollar, which rallied over 1%, while Gold also advanced but only gained 0.54%. To me, that means that traders are starting to recognize that Gold is the ultimate flight to safety when a financial system starts to deteriorate.

Traders were relieved that risk of contagion to other banks appears to have been contained, at least for the time being. I think there is more to come, since additional cockroaches are likely to be hidden and will eventually surface.

The major indexes rallied, dumped, and rebounded to score a green close with the Dow snapping a five-day losing streak. As I pointed out yesterday, the Fed and its cohorts pulled the emergency brake by promising to backstop ALL depositors in the two failed banks.

As a result, small banks soared after many of them losing some 50% during yesterday’s chaotic session. On the other hand, depositors withdrew their funds from those institutions as fast as they could and inundated large banks, which are considered to be of the “too large to fail” category.

In other words, small banks are losing deposits quickly, which ultimately may have the same effect as we’ve seen with the now defunct SVB. Still, the regional banking index KRE rebounded 2% after having dropped 12% yesterday.

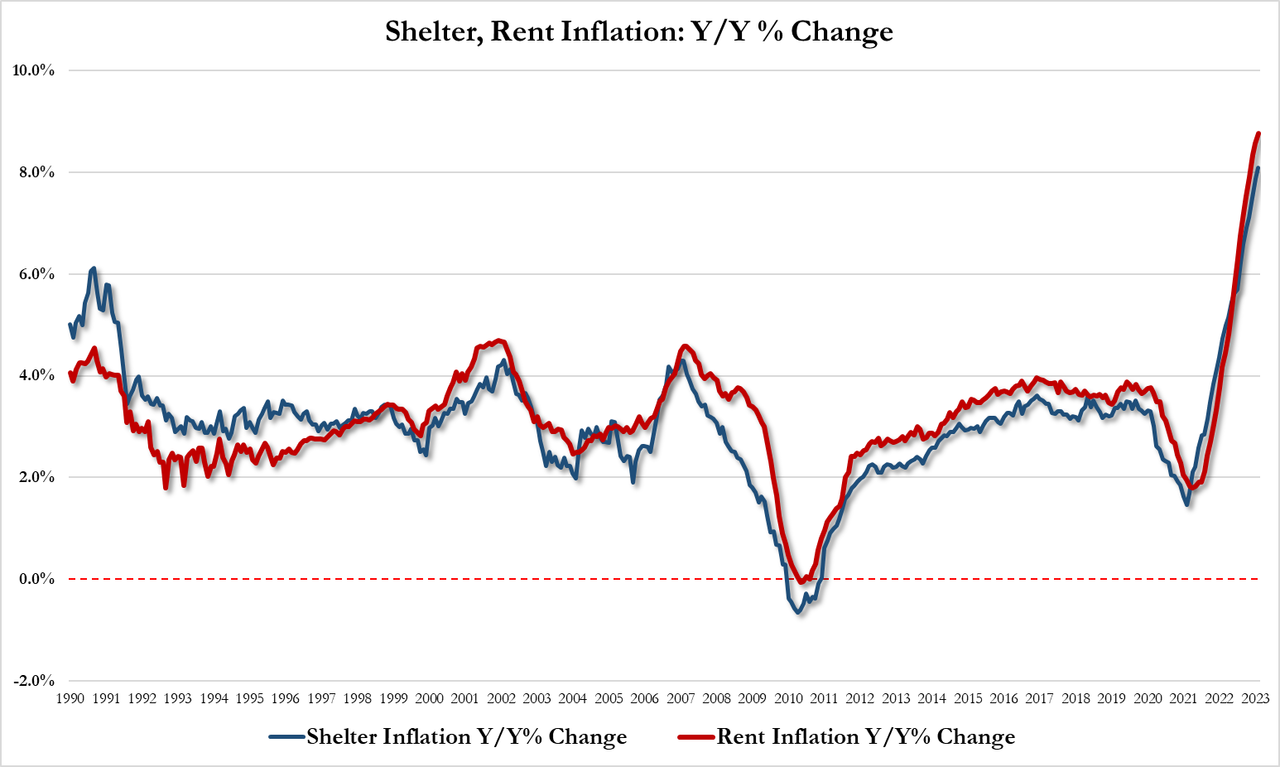

What used to be one of the most eagerly expected numbers, namely the CPI, almost moved to the backburner in view of the banking crisis. The headline CPI came in as expected (+0.4% MoM, +6.0% YoY), which is the lowest YoY reading since September 2021. The only worsening numbers were those of Shelter and Rent inflation, which printed +8.10% YoY and +8.76% YoY respectively, both of which were the highest on record.

Bond yields snapped back today, with the 2-year making the most noise. After collapsing 60bps yesterday, the yield popped some 40bps ending the session at 4.2%.

The US Dollar rode the rollercoaster and closed at the unchanged level. Gold took a breather after its recent Ramp-A-Thon, chopped aimlessly but held on to its $1,900 level.

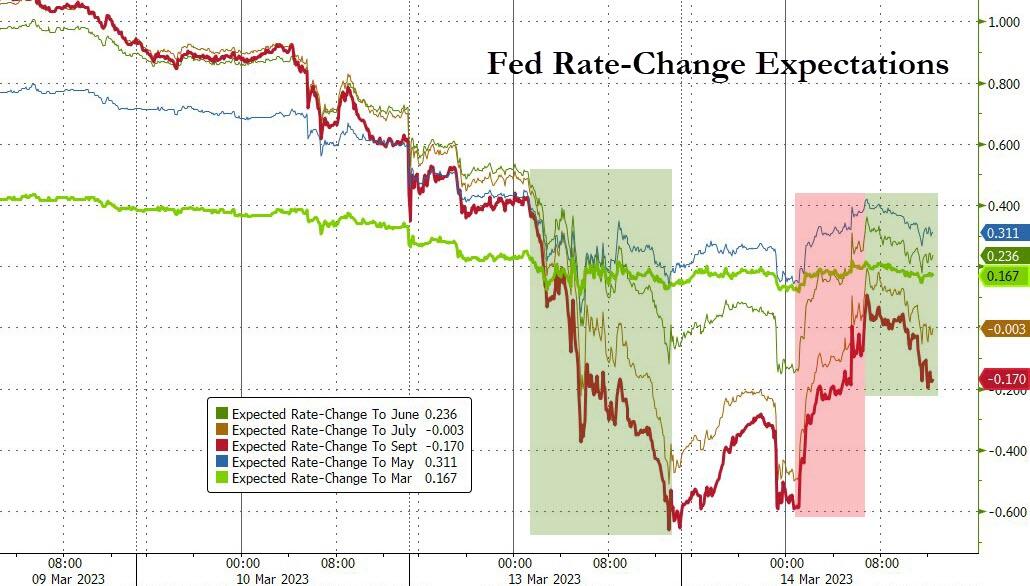

The Fed’s rate trajectory expectations swung wildly, as ZeroHedge pointed out, which means uncertainty about the Fed’s next move reigns supreme. Consensus calls for a 25bps hike when they meet next week.

If they don’t hike, and instead pause, traders will see this as an indication that the Fed has blinked or folded, and a new bull market will likely be on deck.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}