ETF Tracker StatSheet

You can view the latest version here.

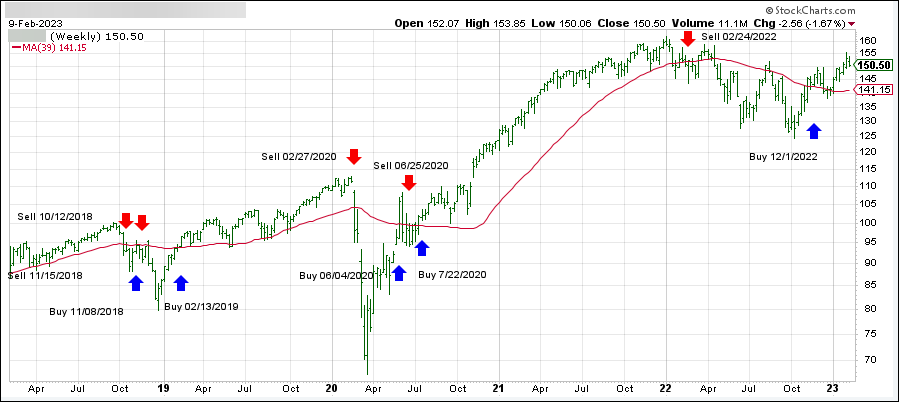

GOING NOWHERE

- Moving the markets

After yesterday’s Puke-A-Thon, the markets tried to find some footing but, while the Dow and S&P 500 managed to eke out a moderate last hour gain, the Nasdaq ended the session in the red.

Alternating between gains and losses, the major indexes closed the week in the red, with the S&P scoring its worst week since December and its first decline in 3 weeks.

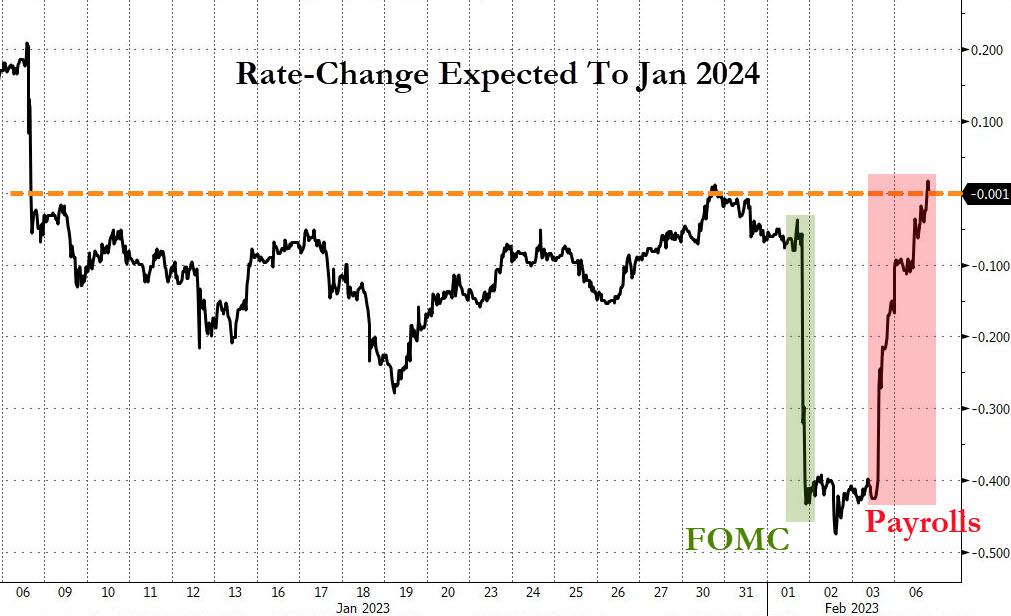

Trying to digest not only the Fed’s hawkish commentary on interest rates, but also the words spewed by various Fed mouth pieces, which all sang from the same hymn sheet, left traders uncertain as whether their dovish conviction will really hold up in the future.

To my way of thinking, the signals from the Fed were very clear, and not mixed at all, yet traders and algos alike were simply not convinced that Powell will be firm in his conviction that there would be no rate hikes this year. This left Wall Street in a state of confusion, which markets hate, hence the increase in volatility.

Not helping bullish sentiment was the latest report pointing to an underwhelming earnings season. About 70% of S&P companies have reported and 70% of those beat analysts’ expectations, which is a drop from the historical average of 79%.

ZeroHedge called it a crash of the “Fed Pivot Party,” as some data points like the Citi Economic Surprise Index rallied unexpectedly, and the Fed’s rate hike trajectory turned decidedly more hawkish, both of which created pain for stocks and bonds this week.

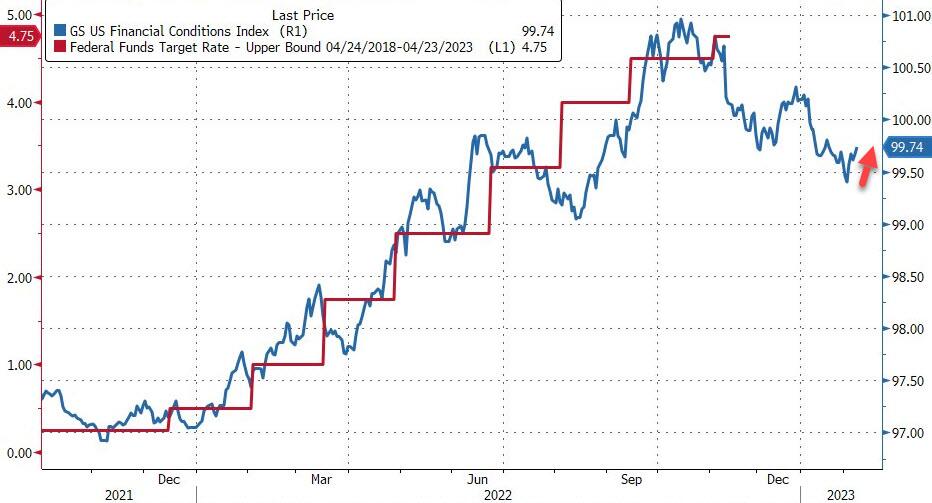

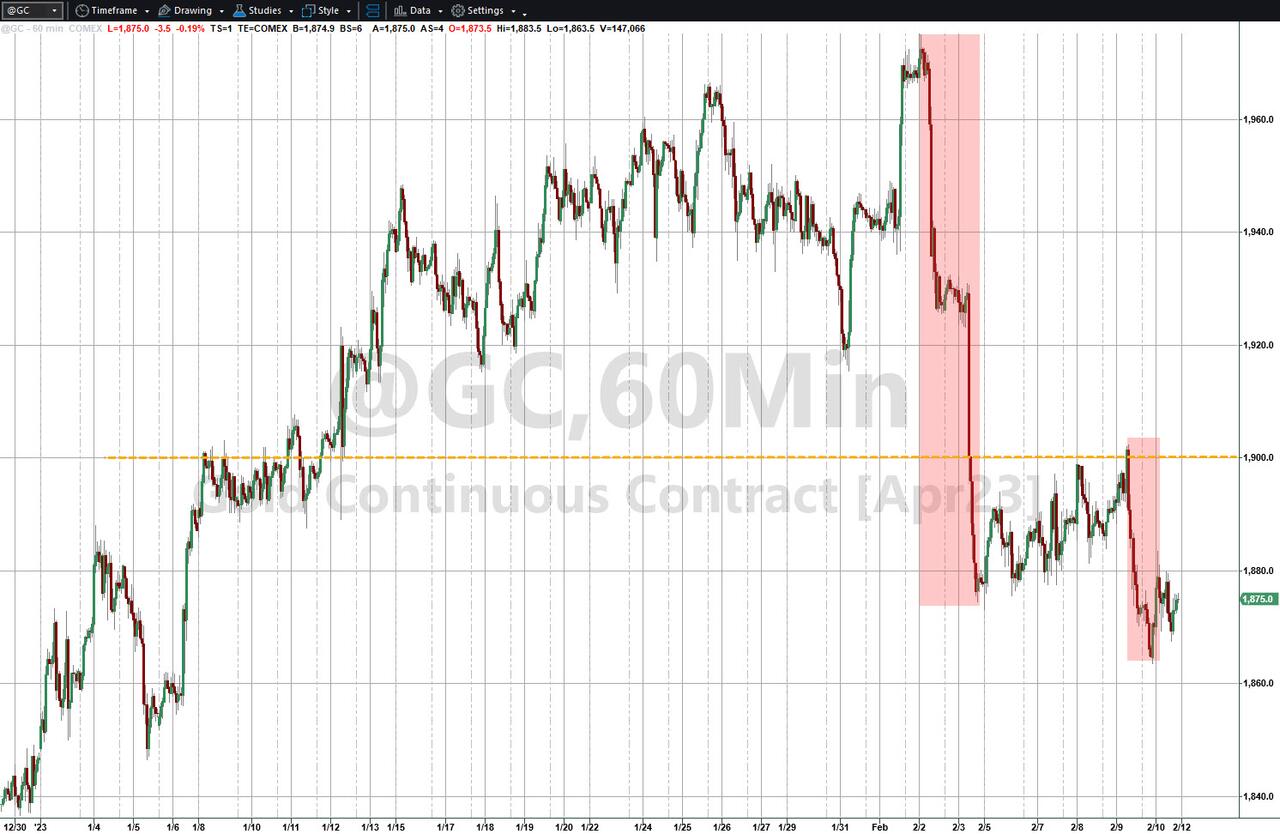

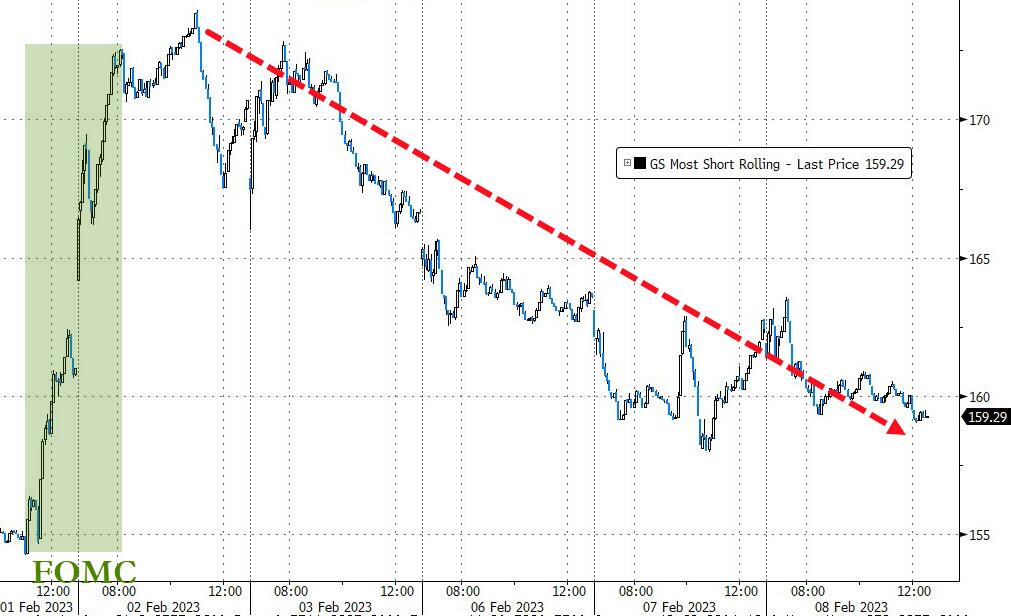

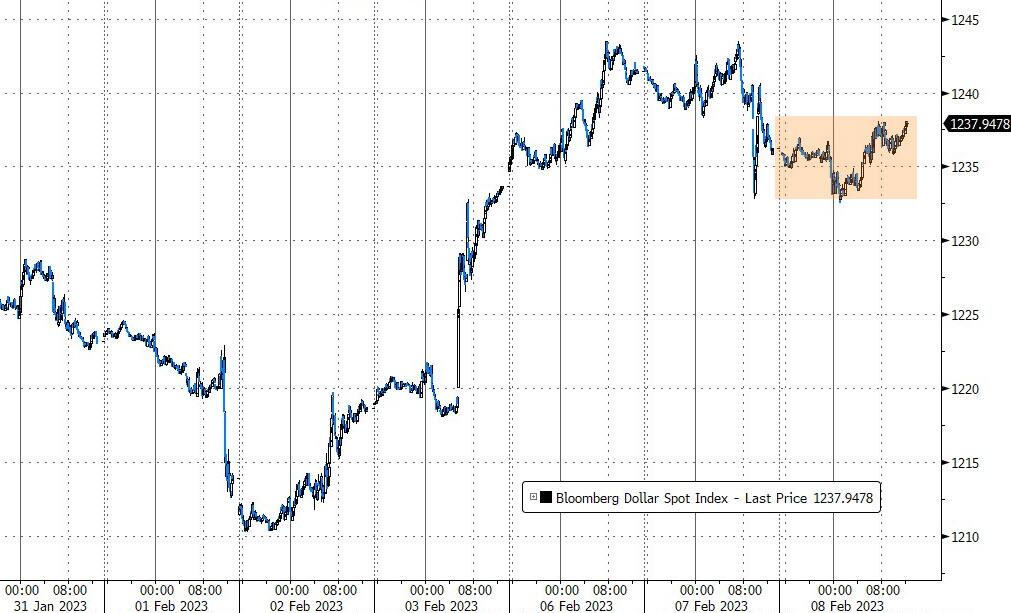

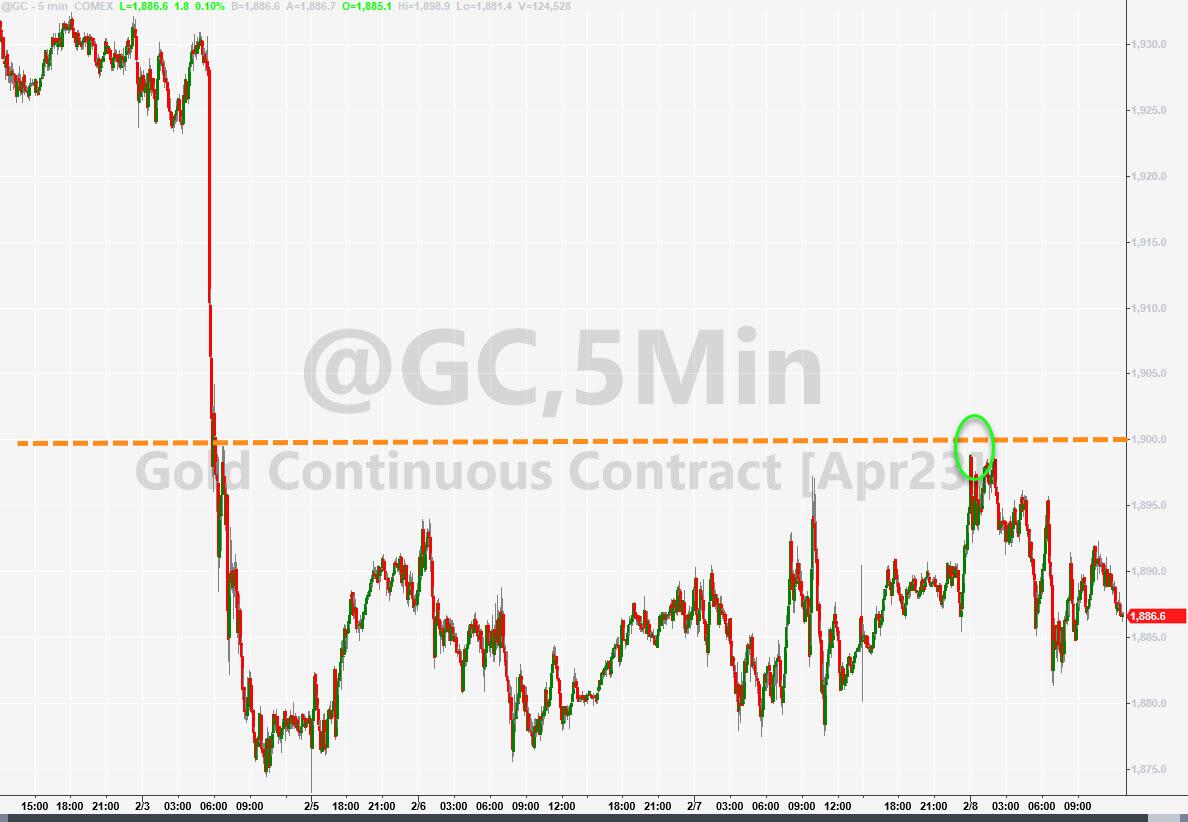

Bond yields ratcheted higher, as financial conditions tightened, causing the most shorted stocks a much needed reversal and helped the US Dollar to climb moderately for the week. Given those facts, it comes as no surprise that Gold suffered by giving up its $1,900 level.

Next week looks like more volatility is on the horizon, with the much-awaited CPI lurking on deck followed by Friday’s options expirations event.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}