- Moving the markets

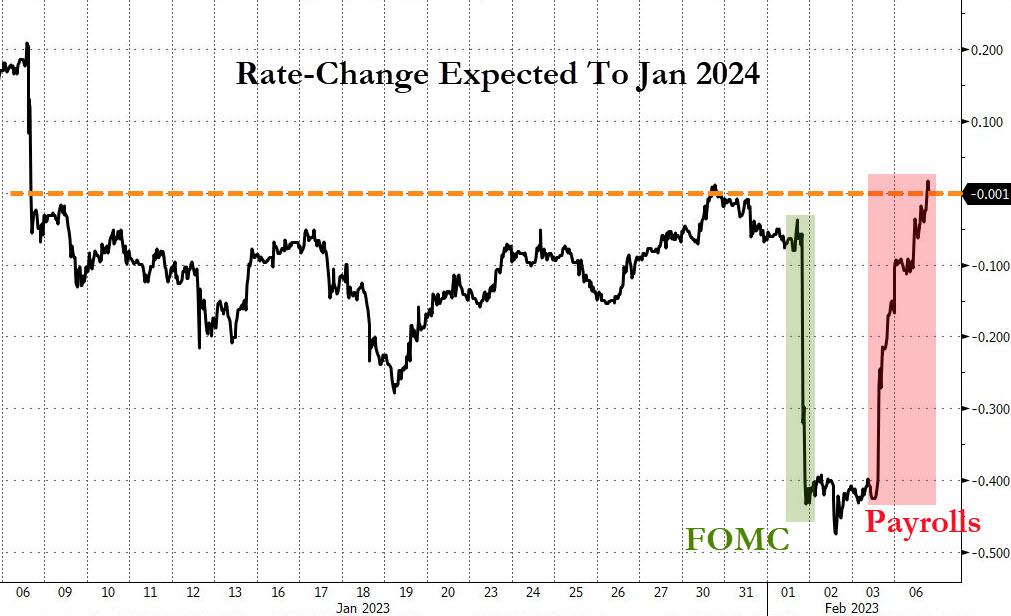

Bond yields jumped sharply with the 10-year adding some 24-basis points to end the session at 3.64%. The markets vacillated predominantly below the unchanged lines, but the major indexes managed to close off their intra-day lows. Still, rate hike expectations have exploded, as the hawkish theme remains to be the dominant one.

{kind=link}

{kind=link}

{kind=link}

Uncertainty reigned, as traders were still shaken up from Friday’s jobs report, which indicated anything but a recession. That brought into question whether the Fed is truly motivated to pause hiking rated—let alone pivot—both firmly held assumptions which formed the basis of the recent rally, the continuation of which has now become questionable.

Earnings continue to be in focus, but so far profits for S&P 500 companies are on pace to be 2.7% lower than Q4 2022, according to data provider Refinitiv. That means the tug-of-war between earnings and hawkish Fed policy continues, with all players now eagerly awaiting Powell’ speech tomorrow at the Economic Club of Washington.

The US Dollar bounced for its 3rd straight day, helped by a jump in bond yields, while Gold held on to slight gains, an impressive performance in light of the dollar’s advance.

{kind=link}

{kind=link}

Trader’s will anxiously dissect Powell’s speech tomorrow for any indication that would clarify whether hawkishness will be the monetary direction for the foreseeable future. If so, the bullish crowd may have to rethink their reckless exuberance.

2. “Buy” Cycle Suggestions

For the current Buy cycle, which started on 12/1/2022, I suggested you reference my most for ETFs selections. However, if you came on board later, you may want to look at the most current version, which is published and posted every Thursday at 6:30 pm PST.

I also recommend for you to consider your risk tolerance when making your selections by dropping down more towards the middle of the M-Index rankings, should you tend to be more risk adverse. Likewise, a partial initial exposure to the markets, say 33% to start with, will reduce your risk in case of a sudden directional turnaround.

We are living in times of great uncertainty, with economic fundamentals steadily deteriorating, which will eventually affect earnings negatively and, by association, stock prices. I can see this current Buy signal to be short lived, say to the end of the year, and would not be surprised if it ends at some point in January.

In my advisor practice, we are therefore looking for limited exposure in value, some growth and dividend ETFs. Of course, gold has been a core holding for a long time.

With all investments, I recommend the use of a trailing sell stop in the range of 8-12% to limit your downside risk.

3. Trend Tracking Indexes (TTIs)

Our TTIs slipped again as surging bond yields kept equities subdued.

This is how we closed 02/06/2023:

Domestic TTI: +7.83% above its M/A (prior close +8.59%)—Buy signal effective 12/1/2022.

International TTI: +9.20% above its M/A (prior close +10.05%)—Buy signal effective 12/1/2022.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

Contact Ulli