- Moving the markets

Traders were relieved that risk of contagion to other banks appears to have been contained, at least for the time being. I think there is more to come, since additional cockroaches are likely to be hidden and will eventually surface.

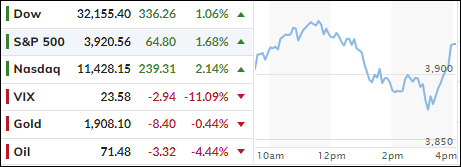

The major indexes rallied, dumped, and rebounded to score a green close with the Dow snapping a five-day losing streak. As I pointed out yesterday, the Fed and its cohorts pulled the emergency brake by promising to backstop ALL depositors in the two failed banks.

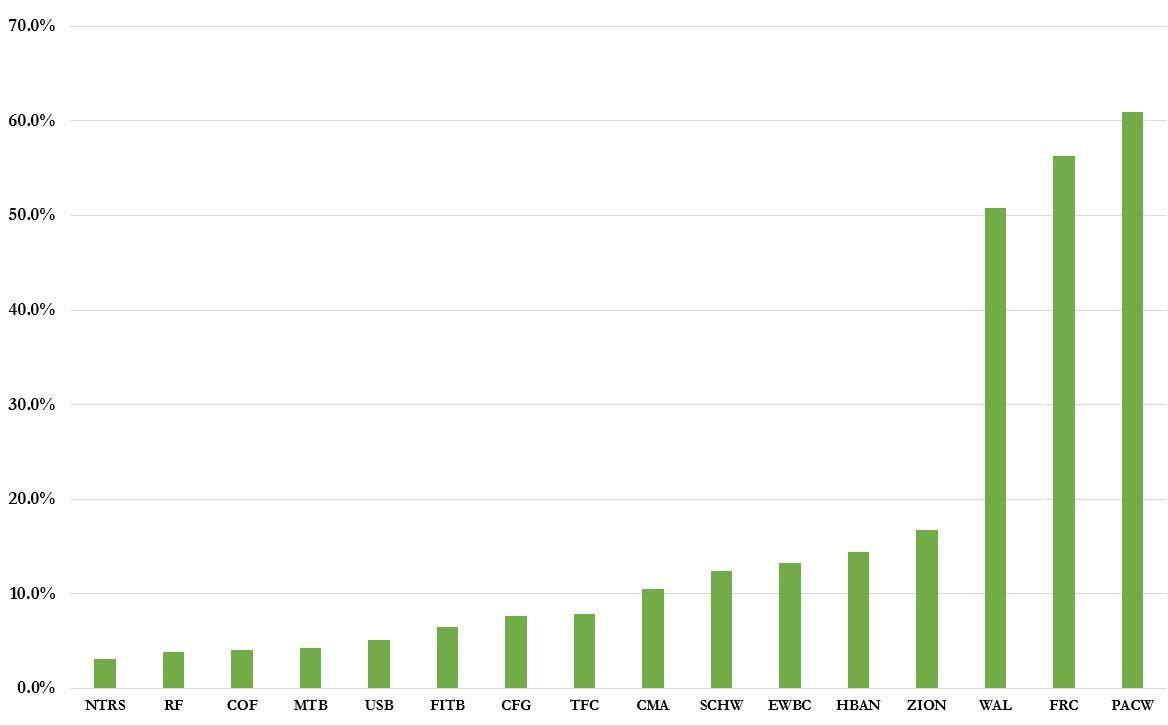

As a result, small banks soared after many of them losing some 50% during yesterday’s chaotic session. On the other hand, depositors withdrew their funds from those institutions as fast as they could and inundated large banks, which are considered to be of the “too large to fail” category.

{kind=link}

In other words, small banks are losing deposits quickly, which ultimately may have the same effect as we’ve seen with the now defunct SVB. Still, the regional banking index KRE rebounded 2% after having dropped 12% yesterday.

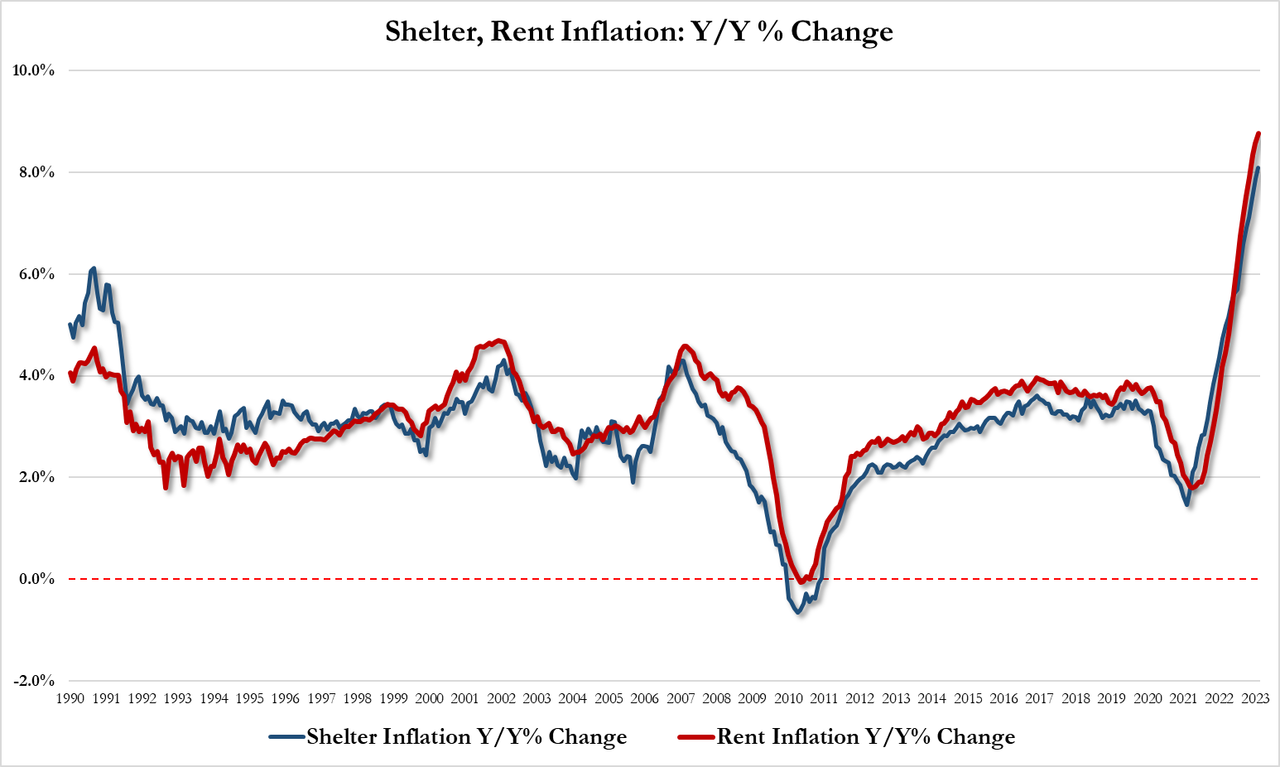

What used to be one of the most eagerly expected numbers, namely the CPI, almost moved to the backburner in view of the banking crisis. The headline CPI came in as expected (+0.4% MoM, +6.0% YoY), which is the lowest YoY reading since September 2021. The only worsening numbers were those of Shelter and Rent inflation, which printed +8.10% YoY and +8.76% YoY respectively, both of which were the highest on record.

{kind=link}

{kind=link}

Bond yields snapped back today, with the 2-year making the most noise. After collapsing 60bps yesterday, the yield popped some 40bps ending the session at 4.2%.

{kind=link}

The US Dollar rode the rollercoaster and closed at the unchanged level. Gold took a breather after its recent Ramp-A-Thon, chopped aimlessly but held on to its $1,900 level.

{kind=link}

{kind=link}

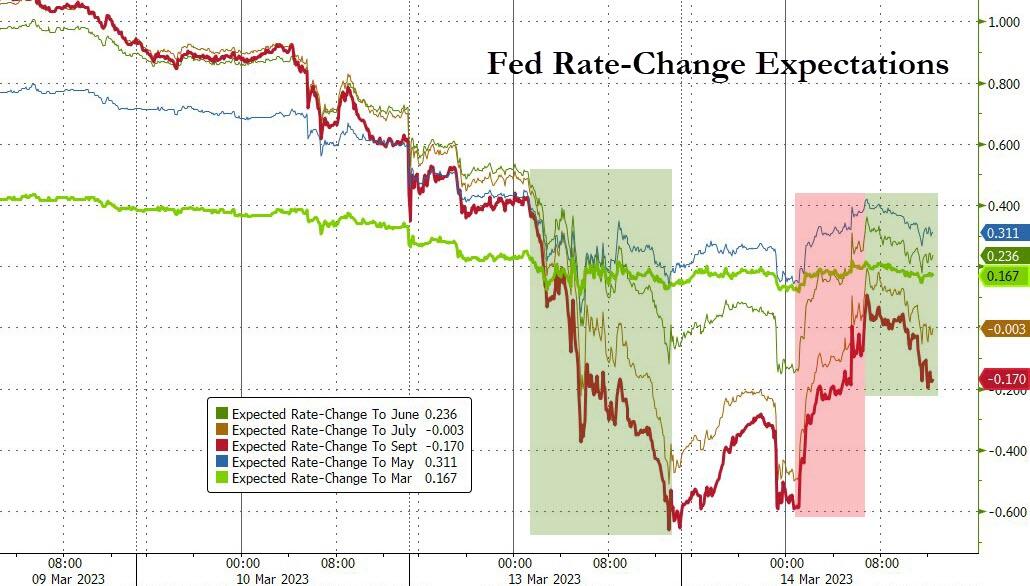

The Fed’s rate trajectory expectations swung wildly, as ZeroHedge pointed out, which means uncertainty about the Fed’s next move reigns supreme. Consensus calls for a 25bps hike when they meet next week.

{kind=link}

If they don’t hike, and instead pause, traders will see this as an indication that the Fed has blinked or folded, and a new bull market will likely be on deck.

2. “Buy” Cycle Suggestions

For the current Buy cycle, which started on 12/1/2022, I suggested you reference my then current StatSheet for ETF selections. However, if you came on board later, you may want to look at the most recent version, which is published and posted every Thursday at 6:30 pm PST.

I also recommend for you to consider your risk tolerance when making your selections by dropping down more towards the middle of the M-Index rankings, should you tend to be more risk adverse. Likewise, a partial initial exposure to the markets, say 33% to start with, will reduce your risk in case of a sudden directional turnaround.

We are living in times of great uncertainty, with economic fundamentals steadily deteriorating, which will eventually affect earnings negatively and, by association, stock prices. I can see this current Buy signal to be short lived, say to the end of the year, and would not be surprised if it ends at some point in January.

In my advisor practice, we are therefore looking for limited exposure in value, some growth and dividend ETFs. Of course, gold has been a core holding for a long time.

With all investments, I recommend the use of a trailing sell stop in the range of 8-12% to limit your downside risk.

3. Trend Tracking Indexes (TTIs)

Our TTIs reversed course and gained. The Domestic one has now moved again within striking distance of turning positive. The whipsawing of the past few days is exactly why I don’t end a “Buy” signal prematurely.

This is how we closed 03/14/2023:

Domestic TTI: -0.61% below its M/A (prior close -1.99%)—Buy signal effective 12/1/2022.

International TTI: +4.33% above its M/A (prior close +3.76%)—Buy signal effective 12/1/2022.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

Contact Ulli