- Moving the market

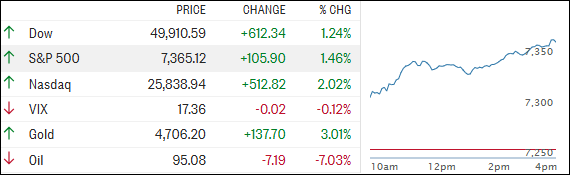

The major indexes took off right from the opening bell after reports surfaced that the U.S. and Iran are closing in on a deal to end the war.

According to Axios, sources say both sides are nearing an agreement that could finally bring the conflict to a close.

The framework reportedly includes a moratorium on nuclear enrichment, and an Iranian foreign ministry spokesperson confirmed to CNBC that Tehran is actively evaluating a U.S. proposal aimed at resolving the standoff.

Adding to the optimism, President Trump said late Tuesday that he is pausing “Project Freedom,” the U.S. plan to guide ships through the Strait of Hormuz, citing “great progress toward a complete and final agreement” in a Truth Social post.

Markets wasted no time reacting. Oil prices plunged as traders rushed to unwind war‑premium positions, with West Texas Intermediate crude falling about 5% to just above $96 per barrel.

Equities got an extra boost from earnings as well. Advanced Micro Devices surged 15% after delivering a strong first‑quarter beat and issuing an upbeat outlook for the second quarter, adding fuel to the broader tech rally.

On the macro front, the tone stayed constructive. ADP’s employment report showed the biggest monthly job gain in 14 months, reinforcing the idea that the U.S. economy remains on solid footing.

The positive momentum held into the close, with the Nasdaq leading the charge and both the Nasdaq and S&P 500 notching fresh record highs. As expected, the Magnificent Seven outperformed the S&P 493, though both groups posted healthy gains.

{kind=link}

Elsewhere, bond yields moved sideways, which pressured the dollar and allowed gold to rally sharply back toward overhead resistance.

{kind=link}

{kind=link}

{kind=link}

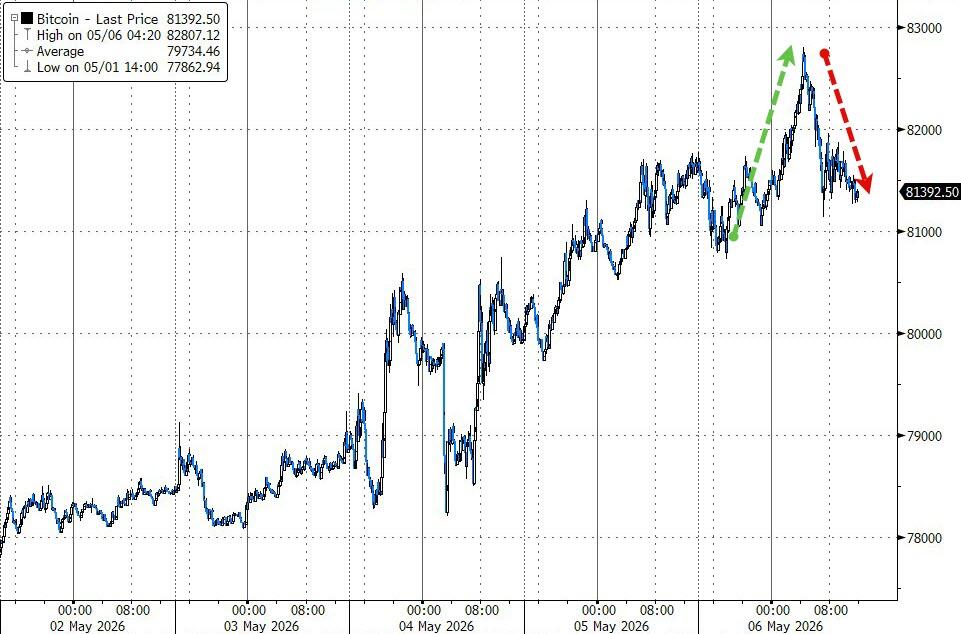

Bitcoin briefly pushed above $83,000 overnight before fading to finish the day roughly unchanged. Its recent strength continues to be supported by hefty inflows into BTC ETFs, totaling more than $1.6 billion.

{kind=link}

With stocks seemingly brushing off higher oil and rate risks and focusing squarely on earnings and economic data, the big question is: how long can this disconnect last before something gives?

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

Hopes for a potential end to the Iran war, combined with a better‑than‑expected payrolls report, were enough to spark another rally right from the opening bell.

The move had broad participation, with the wider market and the metals complex both joining in—led by a strong showing in copper.

Our TTIs jumped on board as well, with both moving higher on the day. The international TTI led the way, outpacing the domestic indicator as risk appetite improved.

This is how we closed 05/06/2026:

Domestic TTI: +6.64% above its M/A (prior close +5.80%)—Buy signal effective 5/20/25.

International TTI: +10.19% above its M/A (prior close +8.08%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli