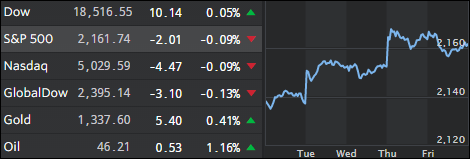

1. Moving the Markets

U.S. stocks extended their record-setting rally and closed at new all-time highs today as investors felt relief by an earnings report from Bank of America (BAC) and a failed coup attempt in Turkey over the weekend. Computer algos, as usual, engaged in a game of headline hockey as Yahoo reported BofAs “better-than-expected profit,” while the far more analytical and realistic ZeroHedge featured “Bank of America’s Profit tumbles 19%,” detailing that the EPS “Beat” was based on a surge in cost-cutting. Well, you can always put some lipstick on that pig to make sure the indexes are rallying.

In a sign of the market’s new resiliency and breakout from its 14-month trading range, it kicked off the week in the black. Last week’s terror attack in the south of France and the latest deadly killing of three U.S. police officers in Baton Rouge did not help investor sentiment, however, markets have stayed strong nonetheless.

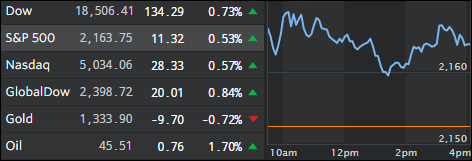

In the world of internet media, with a possible new buyer waiting in the wings, Yahoo (YHOO) delivered what most were expecting in its second quarter earnings report: lower expenses and slower growth. The company’s investors are still awaiting a potential corporate sale by the end of 2016, but the stock continues to perform well nonetheless.

Earnings season has arrived. More than 90 companies in the S&P 500 are set to report earnings this week and currently, analysts are expecting earnings in the April-thru-June period to contract 4.5%. If this contraction takes place, it would mark the fourth quarter in a row with negative profit growth. The hope on Wall Street is that the so-called “earnings recession” will end in the second quarter, paving the way for a resumption of profit growth beginning in the current quarter, which began July 1 and ends Sept. 30. Sure, more lipstick on that pig…