- Moving the markets

A sharp early dive pushed the Dow down some 250 points (thanks in part due to IBMs poor earnings report) shortly after the opening with the other major indexes seeing red numbers as well. A slow but steady recovery pulled the indexes back above their respective unchanged lines, but the gains did not hold, and we closed slightly down, a remarkable achievement given the lousy start to the session.

Throwing some cold water on the rebound was the release of the Fed minutes showing that most policy makers support the fact that interest rate hikes should continue to be implemented. Consequently, the 10-year bond yield jumped 2.5 basis points to close at 3.19%.

Economic numbers were disappointing to say the least, with the housing market showing weakness all the way around. Mortgage applications collapsed to 18-year lows, mostly due to 30-year fixed rates now exceeding 5%. Housing Starts resumed their September collapse by slumping 5.3%, while Permits disappointed because of a 18.9% breakdown in the MidWest.

Still, the markets managed to overcome the hawkish Fed minutes and poor data, but caution was the theme on Wall Street today, since volatility looks to stay with us as witnessed by this morning’s market breakdown. The positive is that most players on Wall Street still see a strong earnings season ahead supporting the bullish mood.

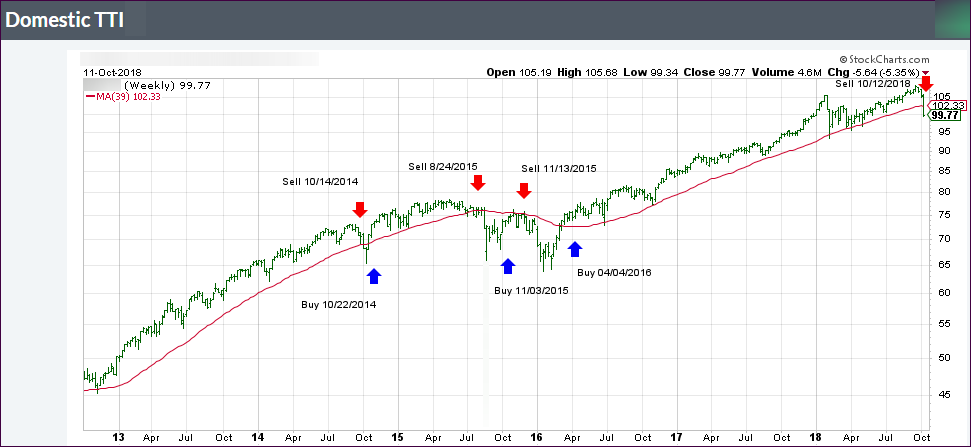

Regarding domestic major trend direction, we’re still stuck in the neutral zone. Our Domestic TTI (see section 3 below) slipped a tad but is stilling hanging on to the bullish side of the trend line by a scant +0.06%, which is hardly a position conducive to support either the bulls or the bears.

We will hold on and wait for more directional clarification and, depending on the outcome, will either add to current holdings or move all the way to cash. Right now, patience is the key to avoid any unnecessary whip-saw signals.

{kind=link}

{kind=link}

{kind=link}