- Moving the markets

Forget yesterday’s ugly close, during which the major indexes got stuck below their respective 200-day M/As indicating more pain to come on the downside. Today was a new day, where the bulls ruled for the entire session, as an upbeat earnings mood and some decent economic data (US job openings, industrial production) wiped out any bearish concerns.

At least for this session, the widely watched 200-day M/As served as a springboard to pull the indexes (except SmallCaps) out of the doldrums and back into bullish territory. While one day does not make a trend, if there is more upside follow through, we may see a resumption of the bullish theme.

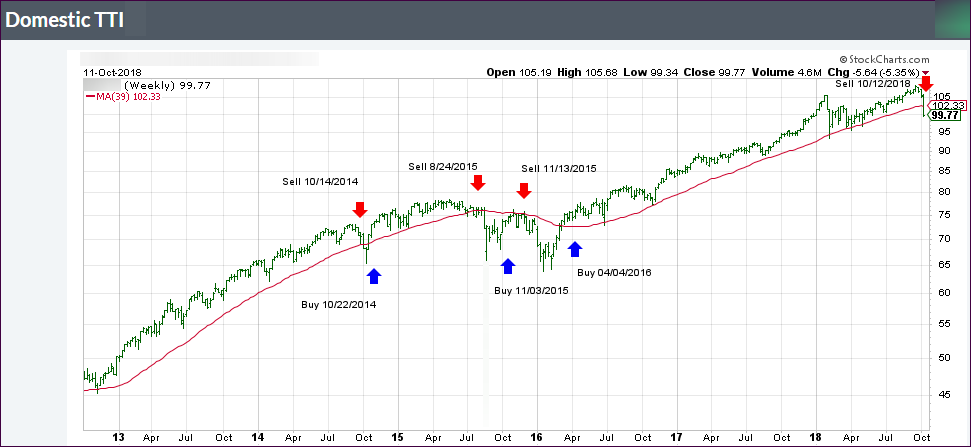

Let’s not forget that the S&P 500 had dropped sharply during last seven sessions and the Dow slipped heavily in the last four out of five, pushing our Trend Tracking Indexes (TTIs) into bear territory with the Domestic one closing below its trend line, however, without having had a chance to show any staying power. That fact prompted me to unload only a portion of our domestic holdings, while waiting for more downside confirmation.

If today is any indication, we may have experienced a whip-saw signal in the domestic arena assuming this was not a one-and-done event followed by a resumption of the recent slide and volatility. If there is some stability in the making, I will again increase our current exposure to the domestic market.

Of course, market manipulation is our constant companion and today’s assist came from the fact that today was the biggest short-squeeze day since November 2016’s post Trump election rebound, according to ZH. That violent ricochet feeds on itself as constantly rising prices force more shorts into covering their positions creating more and more buying power to propel the markets higher.

Still, for October, red remains the dominant color, and we’ll have to wait and see if this optimistic rebound has legs, with earning season just dead ahead, or will simply fade away.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}