- Moving the markets

We saw another see-saw ride on Wall Street with bulls and bears engaging in a continuous battle for domination. There were no clear winners and some of the intra-day rally attempts fell short of pushing the major indexes above their respective unchanged lines. The exception was the Nasdaq, which managed to eke out a small gain, while the S&P 500 scored its 4th straight loss.

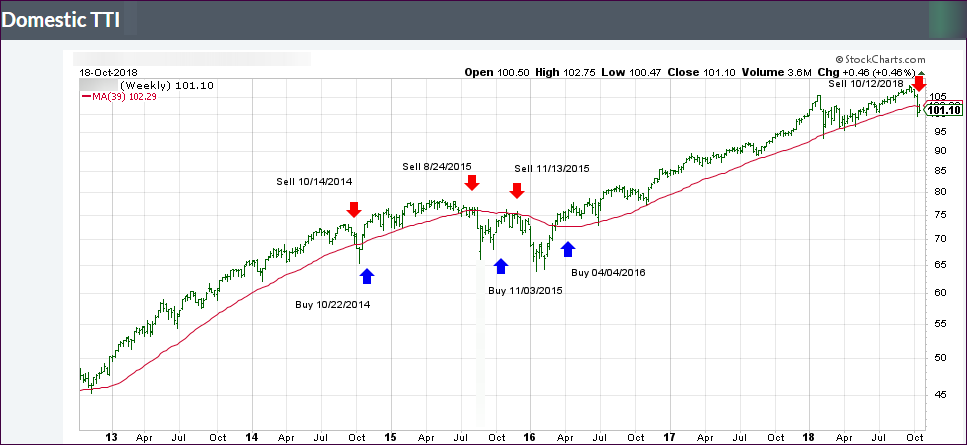

So, the tug-of-war continued, but I took the opportunity to lighten up some more on our few remaining positions, as both of our Trend Tracking Indexes (TTIs) headed deeper into bearish territory with the Domestic one now closing in on a level that requires an all-cash position regarding “broadly diversified domestic ETFs.”

We are at an inflection point where the markets can still break out either way. The only bullish component I currently see is the upcoming earnings season, which could provide a boost to the markets leaving open the question as to whether this would only be of a short-term nature or have enough strength to get our Domestic TTI back on the bullish side of the trend line.

In the meantime, this current choppiness may stay with us until a breakout occurs, either to the downside or to the upside. Right now, downside momentum seems to have the upper hand as my indicators show, along with the US Financial Conditions Index.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}