ETF Tracker StatSheet

https://theetfbully.com/2019/01/weekly-statsheet-for-the-etf-tracker-newsletter-updated-through-01-24-2019/

MAJOR INDEXES GAIN FOR THE DAY BUT PULL BACK FOR THE WEEK

[Chart courtesy of MarketWatch.com]

- Moving the markets

The markets simply ignored Intel’s poor results from yesterday, as optimism about the earnings season kept the bullish theme alive, despite reports that global growth has slowed. While this eventually will affect earnings of multi-national companies, right now, however, traders are looking past those concerns as well as disregarding the divisions in Washington or the fact that GDP may slow down to zero.

The major indexes headed higher right after the opening bell but gave back some of their early gains throughout the session. We ended up on the plus side, but the S&P 500 fell short of recovering some of its losses sustained early in the week.

Still, the headlines were anything but awe inspiring with the all-important durable goods report missing in action due to the government shut-down.

ZH had this succinct comment:

While ‘bad news’ has been signaling ‘good news’ recently (the worse the economy gets, the more dovish Powell becomes… so buy stocks?) – the circular logic of that goldilocks argument is starting to crumble as ‘hope’ has crashed in recent weeks and it is ‘hope’ that keeps the dream alive (e.g., in the short term, economic weakness is bullish for stocks; but in the longer-term, ‘hope’ remains that a dovish Fed will lift the economy and everything will be awesome and the economy will catch up to stocks).

The death of hope… the spread between ‘soft’ survey data and ‘hard’ real economic data has collapsed – removing ‘hope’ from the equation…

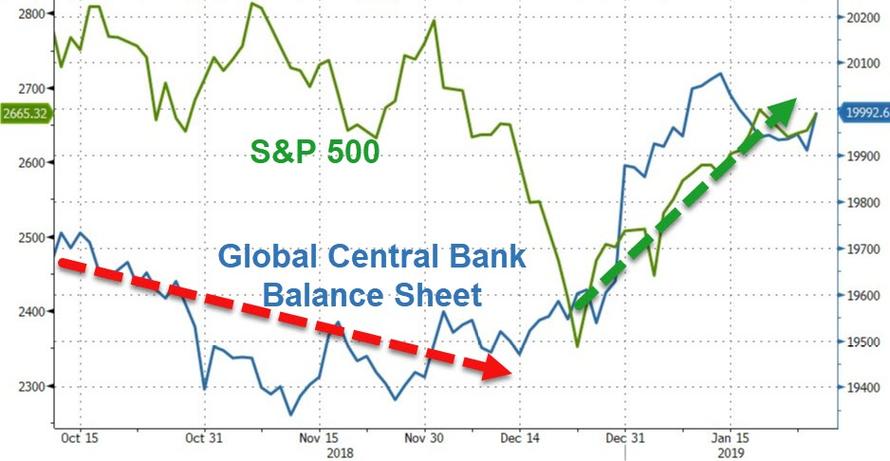

That leaves the major driver of the market as being the Central Bank balance sheet expansion. I have featured the chart before but it’s worth looking at again, if you are still unsure as to what prompts these rallies out of nowhere and with lightening speed. To be clear, there are other factors coming into play as well, such as another giant short squeeze that helped elevate the SmallCap sector.

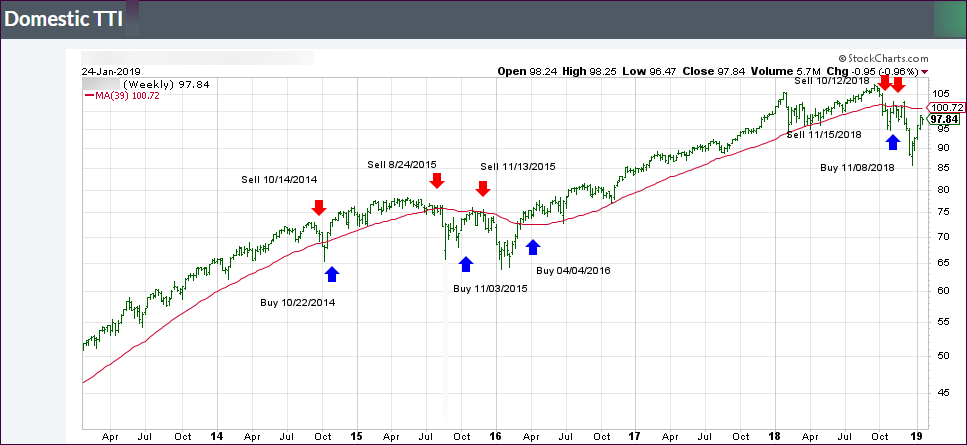

We remain in bear market territory, but our Trend Tracking Indexes (TTIs) have improved markedly and are moving closer to a potential new “Buy” signal (see section 3). Stay tuned…

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}