- Moving the markets

Despite an early struggle for direction, bullish momentum picked up with the major indexes notching another day of gains making this the third winning session in a row.

The trade battles with China and Mexico continued unabated but mixed news was put simply on the back burner. Traders decided to put their focus instead on something more hopeful, namely that the Fed could deliver an interest rate cut and not follow the ECB, which postponed any monetary changes till next year.

It was this type of wishful thinking that supported upside market momentum and kept the bears in check, despite the threat of Mexican tariff going into effect next Monday. Trump said that despite ongoing negotiations “not nearly enough” progress has been made.

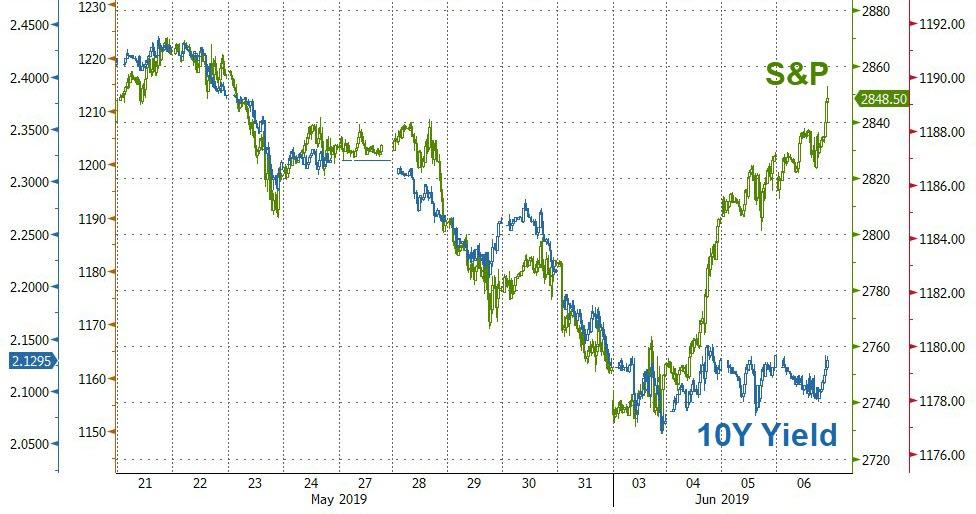

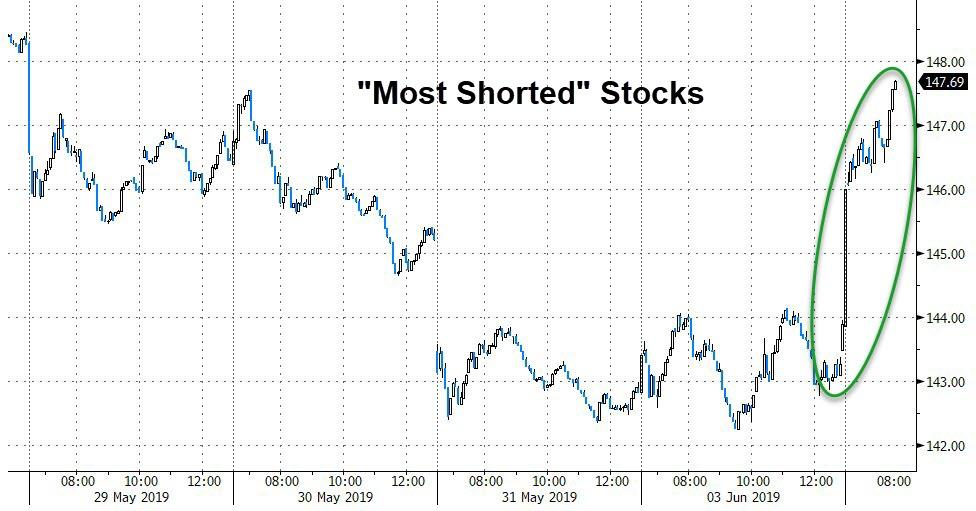

The most shorted stocks were left alone by traders for the second day in a row thereby not contributing to this winning session. Bond yields were steady with the 10-year barely nudging but, in the bigger picture, the decoupling of its yield vs. the S&P 500 remains extreme, as this graph shows.

Our International TTI managed to conquer its long-term trend line, but only by a tiny margin (see section 3), which was not significant enough to consider this a reversal of the recent downtrend—yet.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}