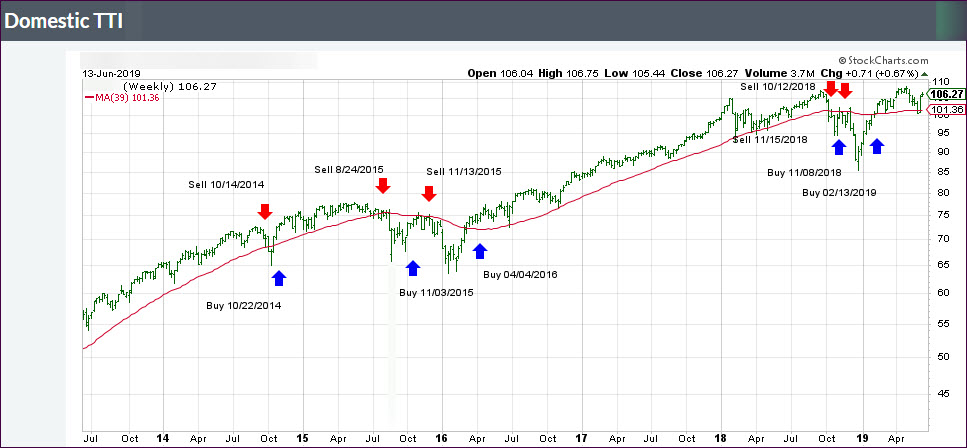

1. Moving the markets

Trump got the markets pumping this morning after tweeting that there will be an “extended meeting” with China’s Xi at the upcoming G-20 meeting in Japan. Bloomberg also added that the two leaders had confirmed a plan for meeting on the sidelines.

That was enough hype for the headline-scanning computer algos to drive the markets out of last week’s trading range, with the S&P 500 now hovering within 1.25% of its record high. Never mind that various reports later-on toned down the Trump/Xi meeting, but that no longer mattered. The bulls were up and running.

The other positive for equities was what appeared to be a policy turnaround, when the head of the European Central Bank (ECB), Draghi, hinted at lower rates and more stimulus. I recall that, only a few weeks ago, Draghi announced no policy changes in the foreseeable future. Hmm, things must have really taken a turn for the worse…

His dovishness was just what global traders wanted to hear with the instant result that stocks pumped and yields dumped, widening the already substantial divergence between the S&P 500 and the 10-year yield.

Bond yields crashed globally, as you can see here, here and here. Other than the U.S., most bond yields on the face of this earth have now slipped into negative territory. For example, if you invest in a German 10-year bond (called ‘Bund’), your annual interest rate is now -0.32%. In other words, you lose -0.32% every year for 10 years. How is that for insanity?

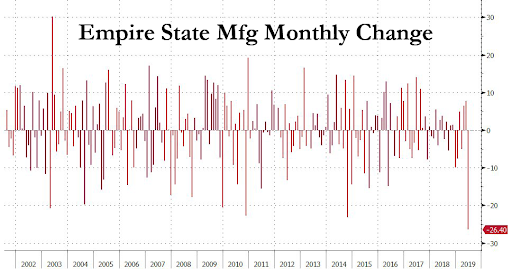

For further contemplation, ZH posted the question: Who’s right? Global Bonds, Global Stocks or Global Macro? This chart shows the divergence. Eventually, we will find out the answer to that question.

My guess is that bonds will prove to be right, with stocks ultimately having to correct down to fair value.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}