- Moving the markets

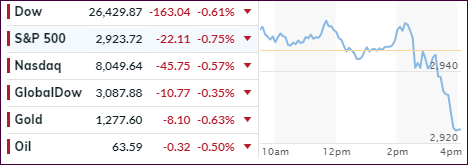

The session started with the major indexes edging higher, that is until the Fed came out stating that current “policy is appropriate with no bias to hike or cut.” Powell further elaborated that U.S. inflation is “possibly being dragged down by ‘transitory’ forces” and that their current stance is “appropriate right now” and “we don’t see a strong case for moving in either direction.”

That put an end to the rumor that the White House is dictating Fed policy and most likely also served as a face-saving action by the Fed, which it had been in dire need of, ever since the sudden policy U-turn last December.

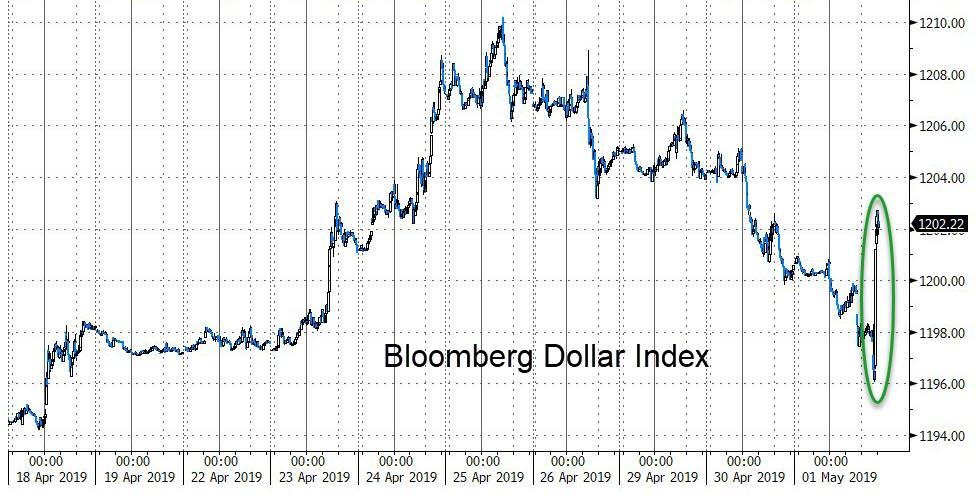

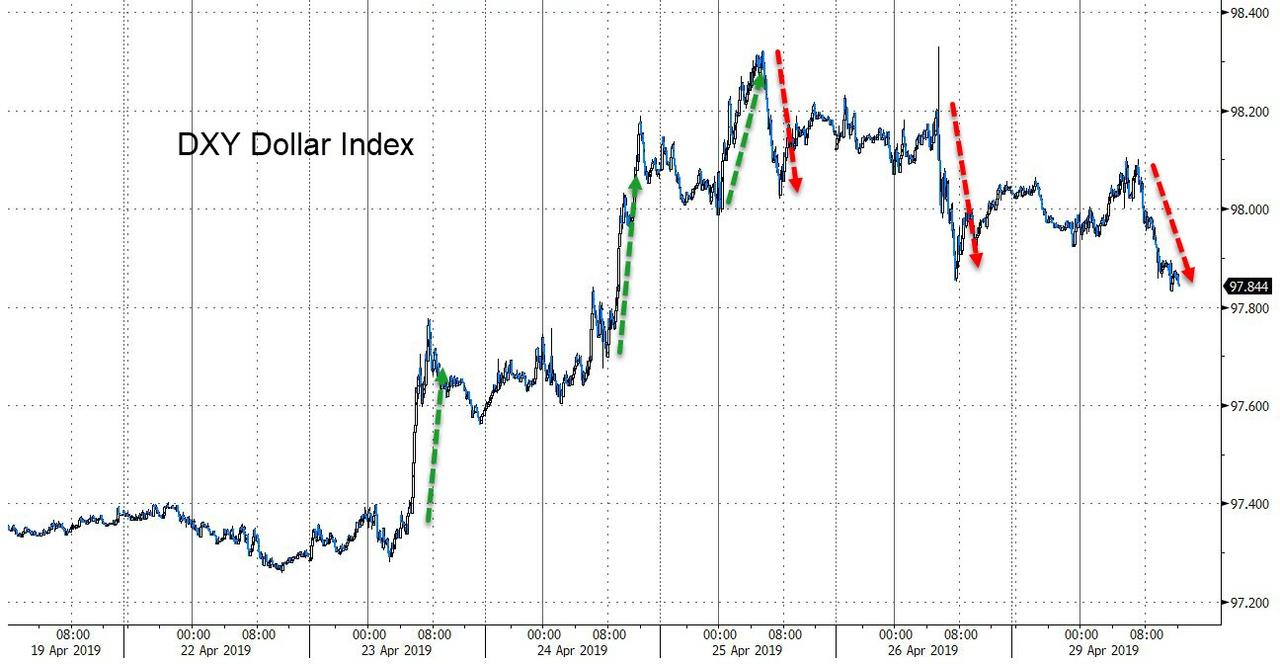

The markets were hoping for a more “dovish” stance from the Fed, so traders decided to hit the sell buttons during the last hour to share their disappointment with the investing public. Apparently, the Fed’s use of the word “transitory” did not only have a negative effect on stocks but also bonds and gold, while the US dollar benefited and spiked.

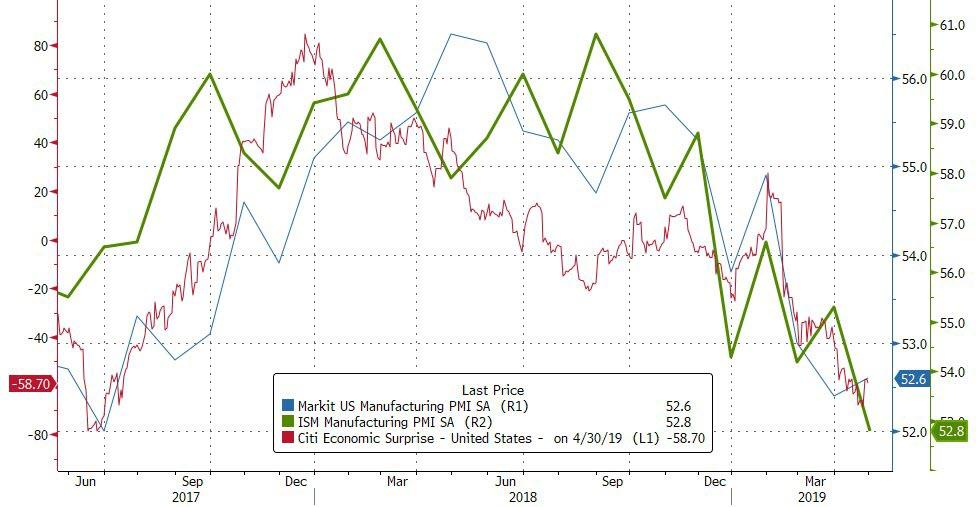

Economic news continued to present more negatives. The manufacturing index plunged to October 2016 lows, while the gauge for export orders dropped below 50 for the first time in three years, as imports missed the threshold for the first time in two years, according to ZH.

This ended up being a poor start to the month of May, and we’ll have to wait and see if the adage “sell in May and go away,” proves to be correct again.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}