1. From the universe of over 1,800 ETFs, I have selected only those with a

trading volume of over $5 million per day (HV ETFs), so that liquidity and a

small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and

2), are made based on the respective TTI and its position either above or below

its long-term M/A (Moving Average). A crossing of the trend line from below

accompanied by some staying power above constitutes a “Buy” signal. Conversely,

a clear break below the line constitutes a “Sell” signal. Additionally, I use a

7.5% trailing stop loss on all positions in these categories to control

downside risk.

3. All other investment arenas do not have a TTI and should be traded

based on the position of the individual

ETF relative to its own respective trend line (%M/A). That’s why those signals

are referred to as a “Selective Buy.” In other words, if an ETF crosses its own

trendline to the upside, a “Buy” signal is generated. Since these areas tend to

be more volatile, I recommend a wider trailing sell stop of 7.5% -10% depending

on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

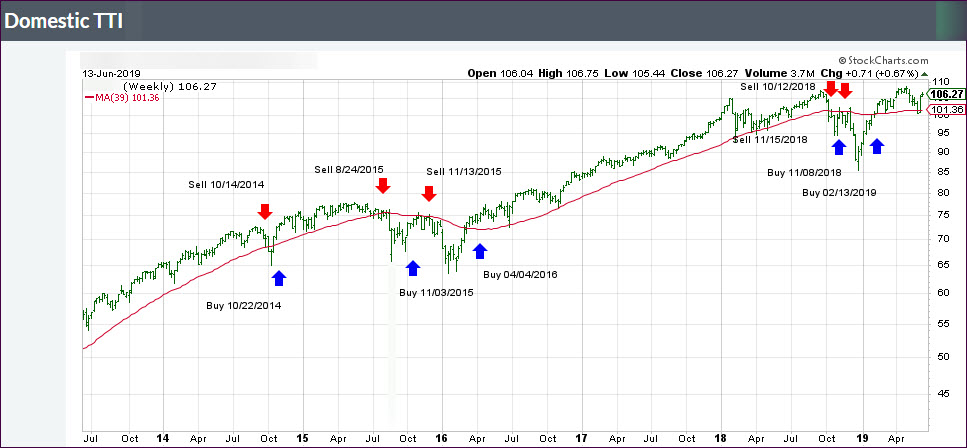

1. DOMESTIC EQUITY ETFs: BUY

— since 02/13/2019

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) is now positioned above its long-term trend line (red) by +4.84% after having generated a new Domestic “Buy” signal effective 2/13/19 as posted.

Equities managed a small rebound, after 2 days of modest

losses kept the major indexes in check. Oil prices spiked as two oil tankers were

damaged in suspected attacks off the coast of Iran, increasing tensions between

Teheran and Washington.

Of course, by default, no matter if it makes sense or

not, Iran is suspected to be the guilty party—at least for the time being. Be

that as it may, the energy sector was the beneficiary of this event with Crude

Oil reclaiming its $52 marker.

Trade tensions with China saw a tiny positive development

when Trump mentioned that he “doesn’t have a deadline” for imposing additional

tariffs and adding that he had a “feeling” a deal could be reached. I am

sure, the jawboning is far from being over…

In the end, it turned out to be a roller coaster ride,

with the major indexes giving back most of their early gains. However, during

the last 30 minutes of trading, a sudden burst of upward momentum pushed the

indexes close to the opening high, but the Nasdaq was unable to get back above its

50-day M/A.

There was not much gained or lost regarding our Trend

Tracking Indexes (TTIs).

Upward momentum was conspicuously absent during this session,

which had stocks drift aimlessly lower, interrupted by the occasional bounce to

nowhere. The major indexes followed yesterday’s theme by slipping moderately.

On the menu was the Consumer Price Index (CPI), which showed

prices advancing by an expected +0.1% in April, while the cost of living over the

past year slowed to 1.8% from 2%. This slowing of price growth was another feather

in the cap of those hoping that the Fed will cut rates sooner rather than

later.

The already declining bonds yields, as well as mortgage rates,

have created a new Refi boom, as mortgage applications surged impressively by

26.8% WoW, which was its largest jump since 2015. 30-year

rates have now tumbled below 4%, a level last seen in January 2019.

Regarding China, Trump came out and said that he was the one

“holding up a trade deal with China,” adding that the two countries

would “either do a great deal…or we’re not doing a deal at all.”

You may be wondering what, other than Fed jawboning, has

been driving stocks higher during the past week, but this chart

(thanks to ZH) clearly shows that, after an interruption in May, the global

money supply has been rising again and thereby lifted stocks out of the May

doldrums.

Despite another positive start to the session, equities struggled,

lost traction and slid into the red, with the major indexes hugging their

respective unchanged lines and closing a tad below it.

Powering the markets early on were reports from China announcing

plans for fresh stimulus to keep their economy running. Hope among traders was

high that an easing of trade tensions might be on deck, yet later renewed

posturing between the U.S. and China supported the view that the standoff will

continue.

In the end, none of these headlines provided enough ammo

to keep the indexes in the green. It appears to me that the trade tensions will

escalate further but will be interrupted from time to time by hope of a

resolution, which will then temporarily support a market bounce.

Right now, expectations are that the Fed will please Wall

Street next Wednesday, when they announce their decision on interest rates.

Until then, we may see some aimless meandering in the indexes until it becomes clear

as to what the verdict might be.

A quick end to the Mexican tariff saga helped the major

indexes to follow through from Friday’s rally with the Nasdaq taking the lead,

while the Dow ended higher for the 6th straight session. Upward

momentum, however, hit a glass ceiling mid-day, and we faded into the close.

However, not all is peaches and cream, and Trump warned that should

Mexico’s cooperation to stem the flow of illegal immigrants fail, “we can

always go back to our previous, very profitable, position on tariffs.”

Giving the market an assist as well was the fact that the Fed

is on deck next week, and we will find out if lower interest rates, which

already have been priced in, will come to fruition. Traders anticipate that last

week’s poor jobs report will influence the Fed’s decision in favor of a reduction

in rates.

On the economic side, things did not look rosy, as job openings

fell in April, while layoffs picked up at the same time. However, job

openings remain above the number of unempoyed workers for the 14th

month in a row.

Bond yields

rose notably on the day, which affected the low volatily ETF (SPLV) negatively,

but its unrealized gain for this Domestic Buy cycle remains higher than that of

its SPY cousin (section 2) by over 50%.

Our International TTI edged deeper into bullish territory,

but it has been hovering above the line for only 3 days. This move could reverse

in a hurry, so I will look for more confirmation before declaring a new ‘Buy’

for this sector.

Continue reading…

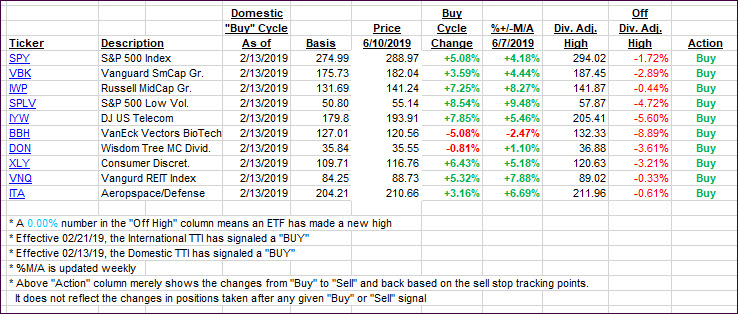

2. ETFs in the

Spotlight

In

case you missed the announcement and description of this section, you can read it here again.

It

features 10 broadly diversified and sector ETFs from my HighVolume list as

posted every Saturday. Furthermore, they are screened for the lowest MaxDD%

number meaning they have been showing better resistance to temporary sell offs

than all others over the past year.

The below table simply demonstrates the

magnitude with which some of the ETFs are fluctuating regarding their positions

above or below their respective individual trend lines (%+/-M/A). A break

below, represented by a negative number, shows weakness, while a break above,

represented by a positive percentage, shows strength.

For

hundreds of ETF choices, be sure to reference Thursday’s StatSheet.

For this current domestic “Buy” cycle, here’s how some our candidates have fared:

Again,

the %+/-M/A column above shows the position of the various ETFs in relation to

their respective long-term trend lines, while the trailing sell stops are being

tracked in the “Off High” column. The “Action” column will signal a “Sell” once

the -8% point has been taken out in the “Off High” column. For more volatile

sector ETFs, the trigger point is -10%.

3.

Trend Tracking Indexes (TTIs)

Our

Trend Tracking Indexes (TTIs) headed north with the International one now being

on the positive side of its trend line for the third day. I’d like to see a

little more staying power before declaring this ‘Sell’ signal to be over.

Here’s

how we closed 06/10/2019:

Domestic

TTI: +4.47% above its M/A (last close +4.14%)—Buy signal effective 02/13/2019

International

TTI: +1.58% above its M/A (last close +1.11%)—Sell

signal effective 05/30/2019

Disclosure: I am obliged to inform you that I, as well as my advisory clients, own some of the ETFs listed in the above table. Furthermore, they do not represent a specific investment recommendation for you, they merely show which ETFs from the universe I track are falling within the specified guidelines.

Below, please find the latest High-Volume ETF Cutline

report, which shows how far above or below their respective long-term trend

lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s

StatSheet and includes 322 High Volume ETFs, defined as those with an average

daily volume of more than $5 million, of which currently 239 (last week 145)

are hovering in bullish territory. The yellow line separates those ETFs that

are positioned above their trend line (%M/A) from those that have dropped below

it.

In case you are not familiar

with some of the terminology used in the reports, please read the Glossary of Terms.

If you missed the original

post about the Cutline approach, you can read it here.

{kind=link}

{kind=link}

{kind=link}

{kind=link}