Below, please find the latest High-Volume ETF Cutline

report, which shows how far above or below their respective long-term trend

lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s

StatSheet and includes 322 High Volume ETFs, defined as those with an average

daily volume of more than $5 million, of which currently 211 (last week 157)

are hovering in bullish territory. The yellow line separates those ETFs that

are positioned above their trend line (%M/A) from those that have dropped below

it.

In case you are not familiar

with some of the terminology used in the reports, please read the Glossary of Terms.

If you missed the original

post about the Cutline approach, you can read it here.

TRADE

WORRIES CONTINUE TO DISSIPATE; S&P 500 UP FOR DAY BUT DOWN FOR THE MONTH

[Chart courtesy of MarketWatch.com]

Moving

the markets

An early rally bit the dust with the major

indexes losing upside momentum, dipping into the red and bouncing around their

respective trend lines throughout most of the session. A last hour push helped

the Dow and S&P back into the green, but the Nasdaq fell just short and

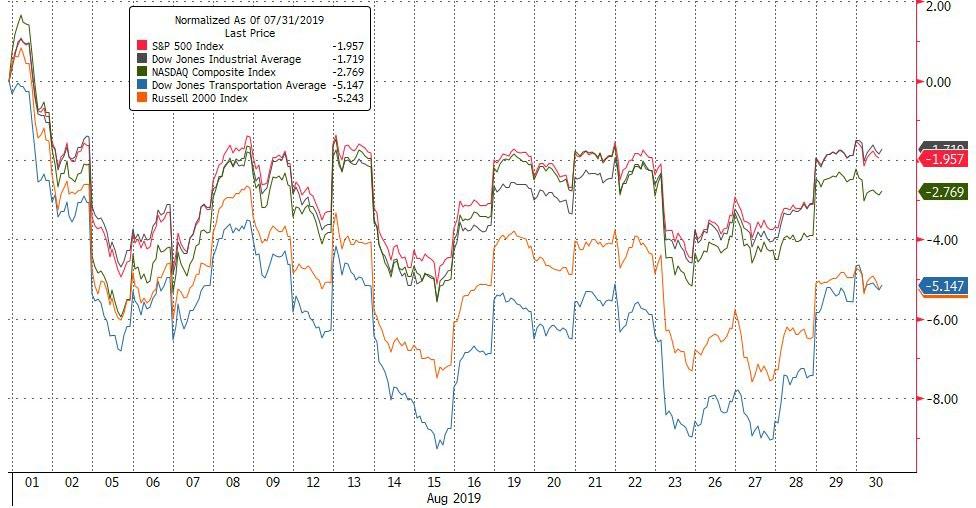

closed down a tad. For the month,

Transportation and SmallCaps fared the worst, while the Dow and S&P lost

the least.

Helping this week’s comeback was the proper dangling

of the trade carrot, which helped the markets climb out of last Friday’s deep

hole, while recovering some of the losses sustained in this volatile month of

August.

It sure paid to be invested in the less volatile

SPLV, which gained +2.14% vs. the S&P 500’s loss of -1.8%.

Since our Domestic ‘Buy’ cycle in February, SPLV has gained 11.69% vs. the SPY’s

+6.35%.

With the US-China trade talks, or rather lack

thereof, having taken centerstage, one analyst described the impasse as

follows:

“Despite U.S. tariffs on $300 billion worth of Chinese goods

set to be raised beginning Sept. 1, another round of trade talks could take

place in the month ahead. Such a possibility allows markets to continue

clinging on to hope that a resolution to this protracted impasse is not dead in

the water, with traders using this as an excuse to push further into risk-on

territory at any given opportunity.”

And there you have it. It’s either US-China words

of hope for any improvement in trade relations or dovish jawboning from the Fed,

with either one of those events being the drivers of equities; fundamentals be

damned.

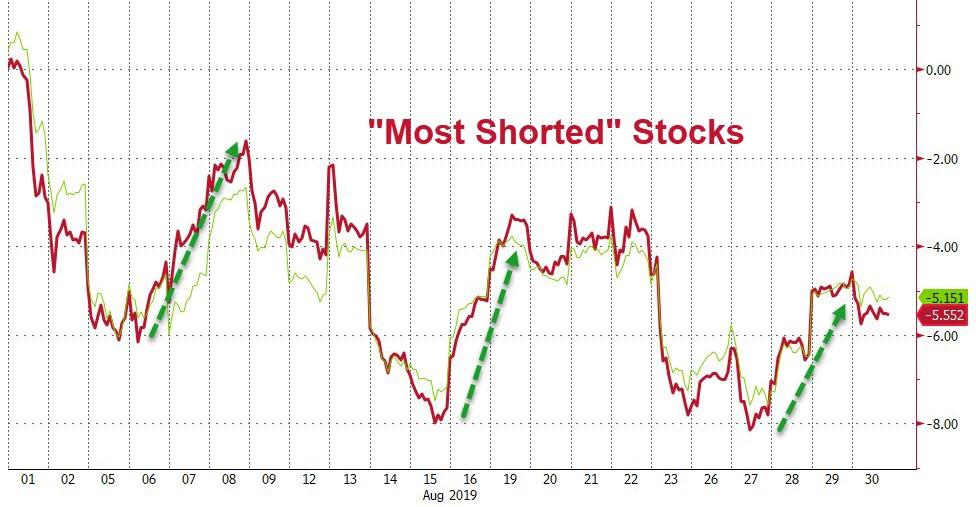

Buybacks gave an assist to the markets on several

occasions, as this

chart by ZH clearly shows. Selected short squeezes also had an impact, as you

can see here,

although they weakened towards the end of the month.

We’re now staring the always volatile September

in the face, and I’m sure it won’t be smoothing sailing. Our trailing sell

stops are ready to be executed, should the need arise.

ETF Data

updated through Thursday, August 29, 2019

Methodology/Use of this StatSheet:

1. From the universe of over 1,800 ETFs, I have selected only those with a

trading volume of over $5 million per day (HV ETFs), so that liquidity and a

small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and

2), are made based on the respective TTI and its position either above or below

its long-term M/A (Moving Average). A crossing of the trend line from below

accompanied by some staying power above constitutes a “Buy” signal. Conversely,

a clear break below the line constitutes a “Sell” signal. Additionally, I use a

7.5% trailing stop loss on all positions in these categories to control

downside risk.

3. All other investment arenas do not have a TTI and should be traded

based on the position of the individual

ETF relative to its own respective trend line (%M/A). That’s why those signals

are referred to as a “Selective Buy.” In other words, if an ETF crosses its own

trendline to the upside, a “Buy” signal is generated. Since these areas tend to

be more volatile, I recommend a wider trailing sell stop of 7.5% -10% depending

on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

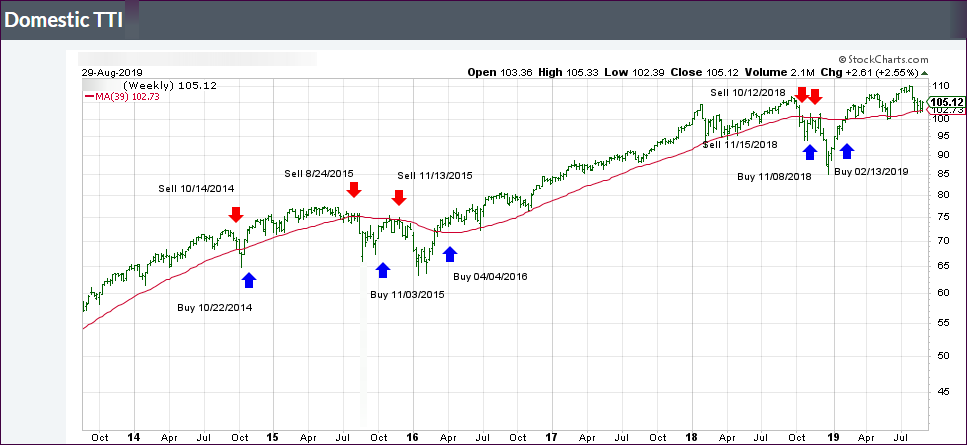

1. DOMESTIC EQUITY ETFs: BUY

— since 02/13/2019

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) is now positioned above its long-term trend line (red) by +2.45% after having generated a new Domestic “Buy” signal effective 2/13/19 as posted.

When all else fails, a few well-chosen words seem to be

enough these days to put a sagging market back into bullish mode. Such was the

case today, when China indicated that they were in no rush to respond to the

latest round of tariffs announced by Washington.

In the process, this week’s rebound has sharply reduced

the month-to-date losses for the major indexes. In the case of the S&P 500,

the index is now only down -1.85%, while at its worst point, on August 14th,

we saw a loss of -4.66%. With tomorrow being the last trading day of the month,

we could see another move higher, should positive trade jawboning continue.

However, today’s jump caused an opening gap in the S&P 500

chart (red circle), which eventually must be closed, meaning that the index

will retreat to cover that gap. It always happens, it’s just a question of

when.

At the same time, the S&P 500 is closing in on the

upper range of its current trading band, as I posted yesterday. The above chart

shows that level (blue line) at around the 2,945. If pierced, we may very well

see an assault of the July highs.

If recent history is an indication, we could bounce off

that “glass ceiling” and head back down to the support line, which lies at the 2,820

level. If that is shattered to the downside, a break of the 200-day M/A (red)

will come into play, which might have dire consequences in that it would not

only bring the June lows into play but also end this current bullish cycle.

Despite an early sell-off, caused

by the bond market flashing a recession signal, the major indexes managed to

climb out of that hole supported by a lift from the energy sector, as oil prices

showed new signs of life. Even with that good effort, we remain stuck in a trading

range with the ceiling of the S&P 500 being in the 2,945 area, while the

bottom lurks around 2,820.

That’s a huge range, in which

we’ve been seesawing since early August. A push through the ceiling may bring all-time

highs back into play, while a break below the bottom may cause the index to

revisit its June lows of 2,728. The Dow as well is rangebound

between its 100-day and 200-day M/As.

Better-than-expected earnings

from Hewlett Packard and Tiffany helped to fuel the fire and kept the bullish

rebound going. The only fly in the ointment was low volume, which is typical

for the week ahead of Labor Day.

The big news came from the

bond market with the 30-year Treasury Bond now yielding less than what the S&P

500 pays in dividends. ZH charted it like this.

This is so unusual and has only occurred for about 3 months in the past 40 years.

It confirms that markets continue

to be distorted beyond recognition.

An early follow through

rally hit the skids and reversed with the major indexes ending up closing in the

red.

It seems that yesterday’s attempt

by the White House to try to revive the trade carrot ran out of steam, when China’s

Global Times editor signaled that there appears to be no great desire (on their

part) to move towards a trade deal any time soon:

“China on Tuesday

issued 20 directives to boost consumption, in an effort to further tap domestic

market, not putting so much emphasis on trade talks. China’s economy is

increasingly driven internally, it’s more and more difficult for the US to press

China to make concessions.”

That was enough to take the

starch out of equites with the Dow

leading the race towards negative territory. It was a seesaw session that

is sure to continue, as any potential trade talks are bound to include more saber

rattling and will be tumultuous at best.

In economic news, we learned

that US home price growth slowed to the weakest in 7 years with the meager MoM

rise of 0.04% missing expectations of an 0.1% rise. This now the 15th

straight month of YoY declines in price, despite plunging mortgage rates.

It looks like the markets

are stuck and are erratically reacting on the latest headline news, which seem

to do nothing but support the current roller coaster. A breakout is sure to come

sooner or later with the question being “will it be to new highs, or will we

head towards bear market territory.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}