Below, please find the latest High-Volume ETF Cutline

report, which shows how far above or below their respective long-term trend

lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s

StatSheet and includes 322 High Volume ETFs, defined as those with an average

daily volume of more than $5 million, of which currently 234 (last week 272)

are hovering in bullish territory. The yellow line separates those ETFs that

are positioned above their trend line (%M/A) from those that have dropped below

it.

In case you are not familiar

with some of the terminology used in the reports, please read the Glossary of Terms.

If you missed the original

post about the Cutline approach, you can read it here.

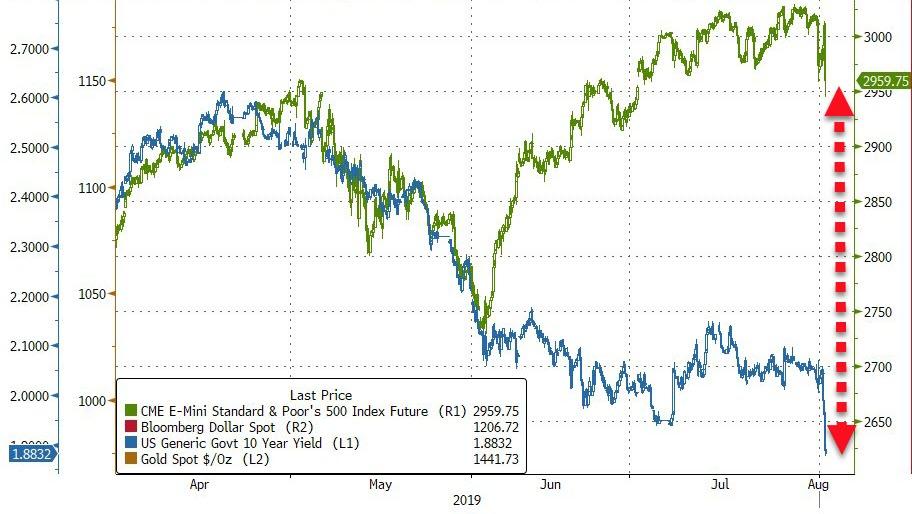

Equities spent most of their day surrounded

by a sea of red, thanks in part to further fallout from the Fed cutting rates by

“only” 0.25%. The bigger impact, however, came from the follow through of tough

language after Trump had announced further tariffs on Chinese goods.

That pushed the markets into bearish mode and

today’s counter punch from the Chinese via words like “temperamental US will

suffer more pain,” did nothing to soothe the raw nerves. This aggravated Wall

Street traders/algos and down we went again recording the worst week of 2019.

As the chart above shows, the outcome could have

been a lot worse, but thanks to buyers stepping in at mid-day, the losses were

sharply reduced, but we still closed in the red. This was the S&P 500’s 5th

successive drop in a row.

Today’s payroll report did not contain any surprises

with 164k jobs added, which was just about the expected number. This decent

headline was weakened by the fact that substantial historical downward revisions

pulled employment gains for May and June down by 41,000 from what was previously

reported.

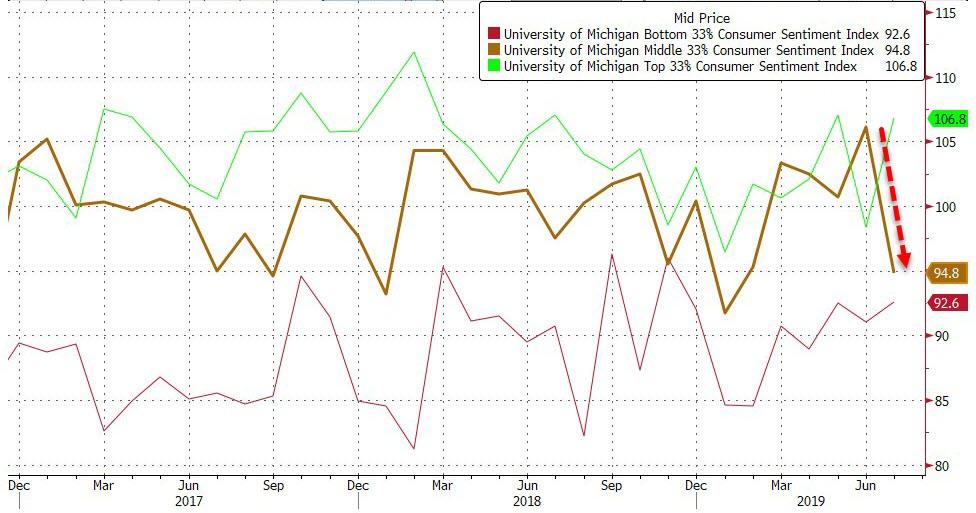

On the economic front, the dire news continues

with Consumer Confidence dropping to 5-month lows, but only in the arena considered

to be the middle-income

Americans, while the bottom and top numbers improved.

Factory orders contracted for the 2nd

month in a row due to a reduction in war-spending, which is a good thing…

Looking towards Europe, we learned that the entire

yield

curve of economic powerhouse Germany dropped below zero for the first time ever.

What that means is that the idiocy continues in bond land, where every bond you

want to buy has now a negative return. Yes, even the 30-year dropped into minus

territory by a tad.

It’s a race to the bottom, with now some $14

trillion in global bonds now yielding less than zero. I am afraid, it’s just a

matter of time that the US will follow suit.

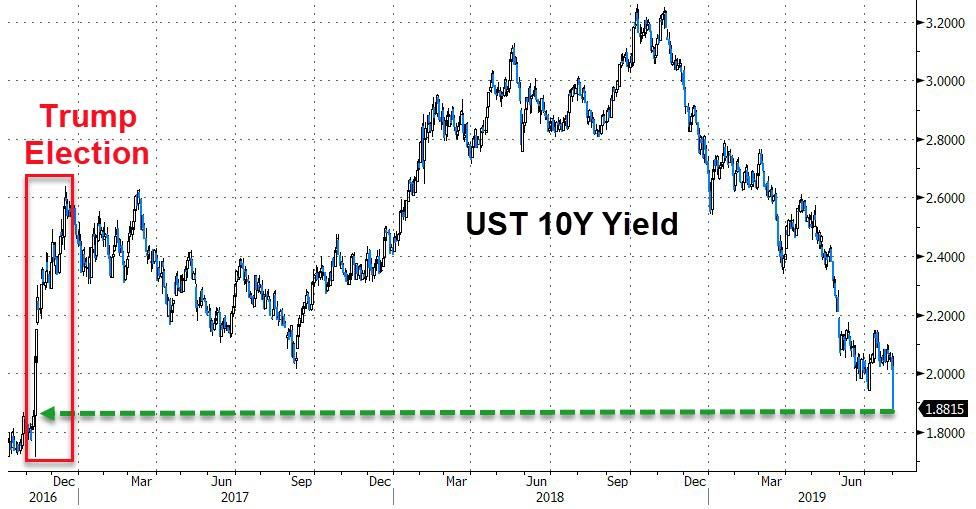

As ZH pointed out, despite this week’s carnage,

bonds and stocks remain dramatically decoupled,

as the 10-year yield experienced its biggest

drop in a week, since the end of 2014.

If the last few days are an indication of what we can expect in the markets, it promises to be an August to be remembered.

1. From the universe of over 1,800 ETFs, I have selected only those with a

trading volume of over $5 million per day (HV ETFs), so that liquidity and a

small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and

2), are made based on the respective TTI and its position either above or below

its long-term M/A (Moving Average). A crossing of the trend line from below

accompanied by some staying power above constitutes a “Buy” signal. Conversely,

a clear break below the line constitutes a “Sell” signal. Additionally, I use a

7.5% trailing stop loss on all positions in these categories to control

downside risk.

3. All other investment arenas do not have a TTI and should be traded

based on the position of the individual

ETF relative to its own respective trend line (%M/A). That’s why those signals

are referred to as a “Selective Buy.” In other words, if an ETF crosses its own

trendline to the upside, a “Buy” signal is generated. Since these areas tend to

be more volatile, I recommend a wider trailing sell stop of 7.5% -10% depending

on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

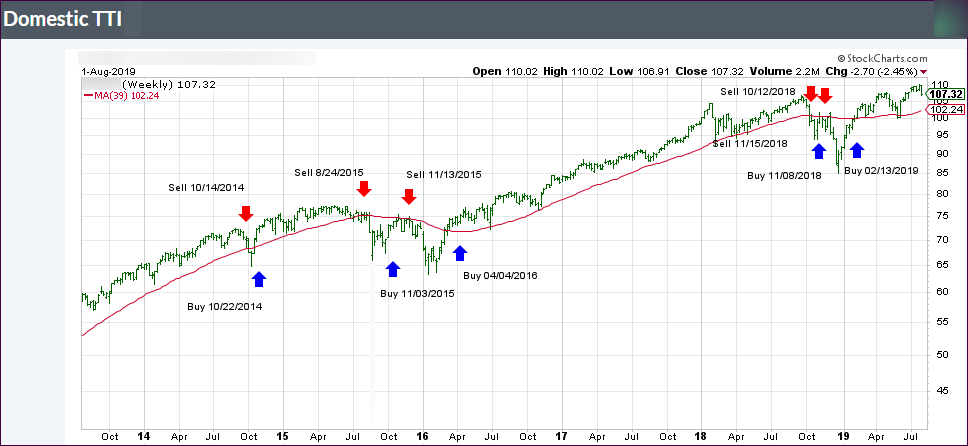

1. DOMESTIC EQUITY ETFs: BUY

— since 02/13/2019

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) is now positioned above its long-term trend line (red) by +5.20% after having generated a new Domestic “Buy” signal effective 2/13/19 as posted.

Sometimes you just have to laugh

out load. Today was such a day, as data showing that US Manufacturing dropped

to its weakest in 10 years, or more specifically since September 2009. One analyst

suggested that the goods producing sector is “on course to act as a significant

drag on the economy in the third quarter.”

That is truly terrible news,

but it was greeted on Wall Street as “terrific” with the major indexes staging

a huge rebound, after yesterday’s drubbing, with the Dow being up at one

point over 300 points.

Then came unexpected “bad

news 2.0” in the form of Trump’s announcement that he will add a 10% tariff on

the remaining $300 billion of Chinese imports starting in September.

That caused an instant trend

reversal, and the major indexes dove south with the Dow at one point being down

over 300 points. All gains evaporated

within minutes, while the 10-year bond yield also did its best swan dive

imitation by reaching a yield that is now below the Trump

election lows.

That caused the “jaws

of death,” as ZH termed it, first to widen and then to narrow. In case you missed

it, they simply represent a divergence between the 10-year yield and the

S&P 500, which sooner or later will have to “normalize.” The question remains

whether it will be via a crash in the S&P or a hike in bond yields or a

combination of both.

Will history repeat itself as this chart comparison to 1987 seems to indicate? Only time will tell, but it’s good to have an exit strategy; just in case.

The Fed did what was expected by cutting interest rates

by 0.25% for the first time in 11 years. Of course, on Wall Street,

expectations don’t mean much, unless you beat them. The Fed failed to do that,

and the markets tanked with the Dow at one point being down some 400 points.

What created most of the damage was Fed head Powell’s

press conference, during which he appeared dazed and confused, after a barrage

of questions forced him to explain his reasoning. He said that the US economy

is doing great, confidence is rebounding, while the 0.25% was an “insurance”

cut.

Then he revealed that today’s rate reduction was just a “mid-cycle”

adjustment and not the start of a “long series of rate cuts.” That shook and stunned

the markets, as several more cuts were assumed to be forthcoming. One analyst

summarized it like this:

“The market was fine with the statement, but

as seems to be the case, the press conference reveals details that do not sit

well with the market. The response that this is a mid-cycle adjustment and not

part of a longer-term accommodative stance has raised concerns. The market has

really talked itself into a need for lower rates. Obviously the FOMC still

feels strongly the economy is resilient.”

That means the widely anticipated easing cycle over the next

six months will not happen, which this

cartoon sums up perfectly. Powell now holds the dubious record of having

held 12 press conference, of which 10 of them were followed by stocks tanking.

Still, while volatility returned with a vengeance today,

for the month, the major indexes gained, led by the Nasdaq, while SmallCaps

fared the worst.

It will be interesting to see if the markets will adjust

to the “Powell theme,” or if there is more fallout to come over the next week

or so.

While the major indexes recovered

form an early session dump, they pretty much repeated yesterday’s theme by slipping

and sliding below the unchanged line without much directional conviction.

A mixed earnings picture today,

along with some negative tweets from Trump regarding a possible China deal,

added to today’s uncertainty and kept equities in a tight range.

As a I posted before, tomorrow

will be the most important trading day of the year, as the Fed is scheduled to

release its verdict on interest rates. Opinions as to its market effect and

whether they should or shouldn’t cut rates have been all over the place.

ZH offered a comparison to

the events of 1987 via this

chart posing the question: Is the Fed rate-cut enough to make new highs in

stock…just like we did in 1987?

We should know the answer to

that in the very near future.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}