- Moving the markets

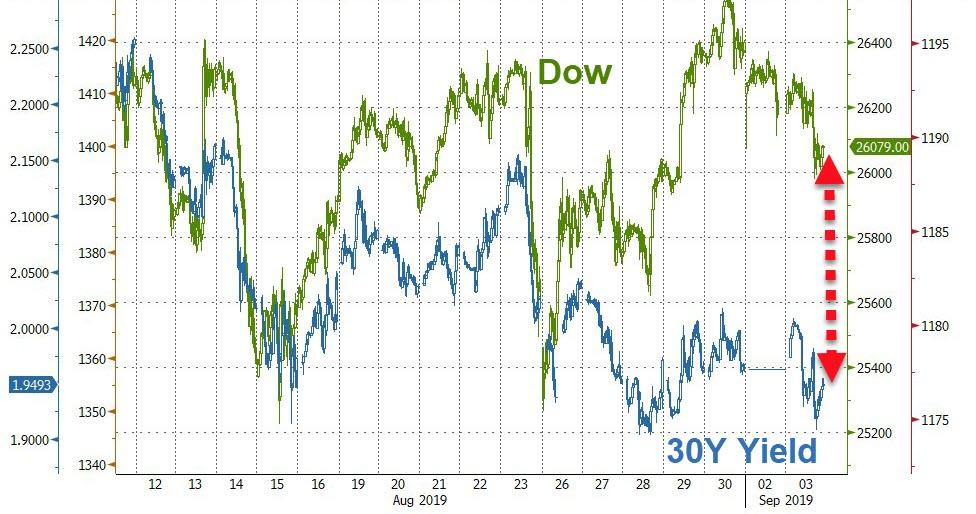

The major indexes staged a turnaround, after yesterday’s pullback, encouraged by an apparent ease in Hongkong tensions. Chief executive Carrie Lam announced that she would withdraw the controversial extradition bill that has sparked months of violent protests, which were feared to eventually hurt the business climate and global financial markets.

While this bill meets only one of five demands from the protesters, at least it’s a step in the right direction, which put the computer algos into a buying frenzy and spreading a sea of green in equities.

Also helping the bullish mood were reports that the People’s Bank of China will soon implement cuts in reserve requirements for Chinese banks, a move that is expected to boost growth and shows willingness by the government to battle the effects of higher US tariffs on Chinese imports.

This readiness by the Chinese to engage in some sort of stimulus eased fears, at least for the moment, that the US economy might slide into a recession in part due to the endless US-China tariff conflict, which has been a contributing factor to not just a worldwide disruption of supply chains but too a slowdown of global economies.

Likewise giving an assist to the bullish cause was more dovish encouragement from a variety of Fed speakers that rate cuts are on the menu. ZH summed them up as follows:

Williams (Dovish): “Ready to act as appropriate”, July cut was right move, economy mixed (admitted consumer spending not a leading indicator), international news matters, low inflation biggest problem.

Kaplan (Dovish): “Monetary policy a potent force”, worried about yield curve inversion, economy mixed (factories weak due to trade, consumer strong), watching for “psychological effects” on consumers, “if you wait for consumer weakness, it might be too late.”

Kashkari (Dovish): Tariffs, “trade war are really concerning business”, job market not overheating, slower global growth will impact US, most concerned about inverted yield curve. Fed’s policy is “moderately contractionary.”

Bullard/Bowman (Looked Dovish): Took part in “Fed Listens” conference but made no comment on policy but then again when has Jim Bullard ever not been dovish.

Beige Book (Mixed): Moderate expansion but trade fears are mounting, but optimism remains, despite what Kashkari says: “although concerns regarding tariffs and trade policy uncertainty continued, the majority of businesses remained optimistic about the near-term outlook”

Evans (Dovish): Trade policy increases uncertainty and immigration restrictions lower trend growth to 1.5%, Auto industry especially challenged

As a result, the markets have now ‘priced in’ an astonishing 124 bps (1.24%) of rate cuts through the end of 2020. Tip of the hat goes to ZH for this chart. On the other hand, a trade deal is now almost entirely ‘priced out,’ which means that the only ‘big dog’ left to support equities is none other than the Fed and its policies.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}