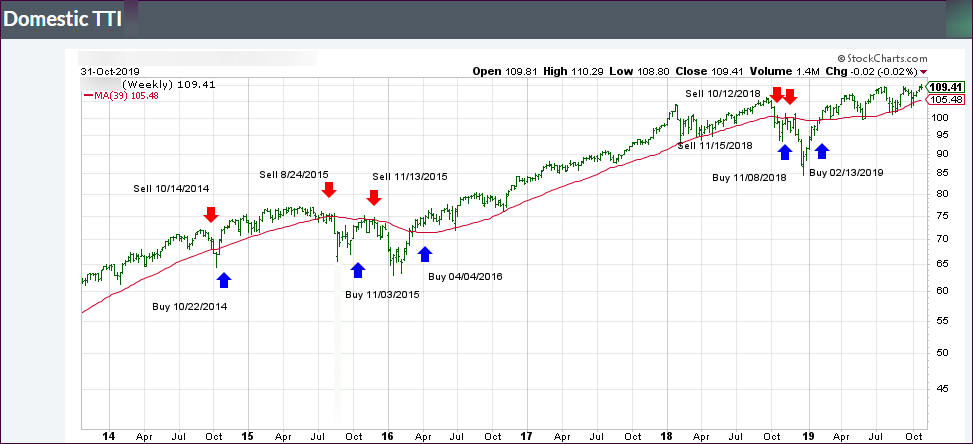

ETF Tracker StatSheet

You can view the latest version here.

Markets Melt Up Due To Better Than Expected Jobs Report

- Moving the markets

The jobs report proved to be the dominating market force today, as October lost its luster as a bull market killer. The US economy added 128k jobs, which was far better than the expected 85k. Another bullish surprise were the upside revisions in employment gains in August and September, which combined were 95,000 more than previously reported.

Manufacturing suffered due to the strike at GM causing a decline of almost 42k automaker jobs but, now that the strike is over, a rebound of similar magnitude is expected next month.

The oddity that stocks continue to rally as bond yields rise, despite the Fed’s easing policy, seems contrary to conventional wisdom—and it is. This scenario has, short-term, not worked out well for the low volatility ETF SPLV, which has not participated in the current rally, as it did for the first 9 months of this year.

As a result, the S&P 500 (SPY +11.34%) is closing in on SPLV’s performance (+13.23%), but it has not caught up yet, however, given current circumstances, I will make some adjustments to our holdings.

Not all of today’s melt-up was due to the jobs report, as variety of officials were called up to keep the mood bullish.

ZH summed up the events in this timeline:

0830ET Jobs Beat – Dow +100

0915ET Fed’s Kashkari dovish: “we’re not at maximum employment.. in free lunch zone” – Dow +20

0920ET Mnuchin: “constructive talks, working hard” – Dow +30

0930ET Fed’s Rosengren hawkish: further monetary accommodation not needed – Dow unch

0935ET Fed’s Clarida neutral: “we will be data-dependent, economy/consumer in good place” – Dow unch

0936ET Fed’s Kaplan dovish: “growth in US is decelerating, need skills-based immigration”

0937ET Kudlow: White House wants tax cuts for middle class, Trump optimistic on trade deal – Dow unch

0945ET Kudlow: “enormous progress on IP theft” – Dow +30.

0950ET Record high for S&P and Nasdaq

0955ET Kudlow: “US-China trade call may be happening now, Ag & FX parts virtually completed” – Dow +20

1000ET ISM Manufacturing MISS, 3rd month of contraction (bad news is good news) – Dow +50

1050ET Mission Accomplished – Dow futs take out post-Powell high stops

1215ET Dow futs stops run and fade begins into EU close

1255ET USTR: “constructive trade talks today” – Dow unch

1300ET Fed’s Quarles dovish: current policy stance “likely to remain appropriate… unless data weakens” – Dow unch

1310ET MOFCOM: “constructive trade talks today, achieved consensus” – Dow +20

1325ET Fed’s Daly neutral/hawkish: “annual wage growth of about 3% is good news” – Dow unch

1450ET Fed’s Williams neutral/hawkish: “economy is in a very good place, it is strong” – Dow -10

1600ET RECORD CLOSE FOR S&P AND NASDAQ

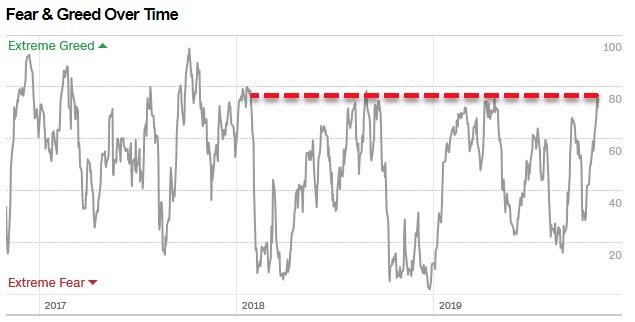

Of course, the Fear & Greed index paints a different picture and has risen to a height last seen in January of 2018. Every time this indicator has reached current levels, it abruptly changed direction. Will it be different this time?

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}