- Moving the markets

The “buy everything” mantra continued today extending the election week rally on beliefs that the current dilemma might result in a divided government, with the powers of the president/congress being offset by the opposing party controlling the senate.

The bullish reaction to the results so far “may have been due to the fact that Republicans appear likely to retain a majority in the Senate, something that will make it hard for Biden to proceed with the tax increases and stricter regulations he promised,” said Charalambos Pissouros, senior market analyst at JFD Group, in a note.

Even though analysts had originally claimed that a “blue wave” sweep of the White House and the congress was being priced in the market, when, suddenly the possibility of a split government seemed “market pleasing” giving power to the bullish cause.

Despite the WH outcome far from being certain, traders are confident that much of the election uncertainty has passed, and the worst possible outcomes seem to have been avoided. At least for the moment, this viewpoint prevails, yet it could change in a hurry.

ZH added this succinct spot-on tweet:

A disputed election is bad for stocks

Legislative gridlock is bad for stocks.

But the combination of the two is great for stocks

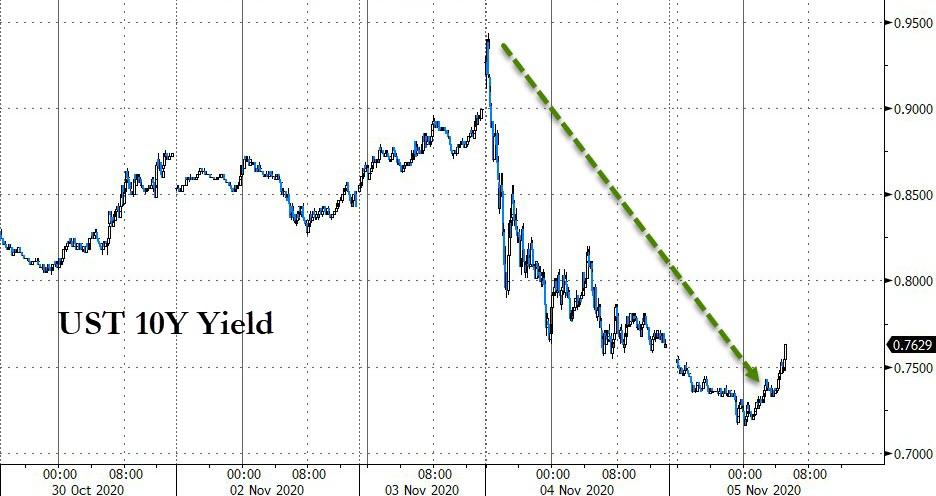

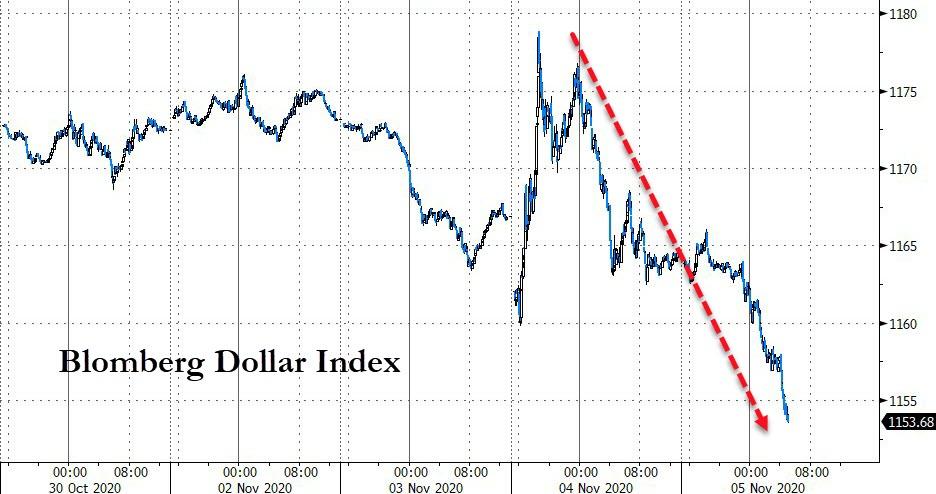

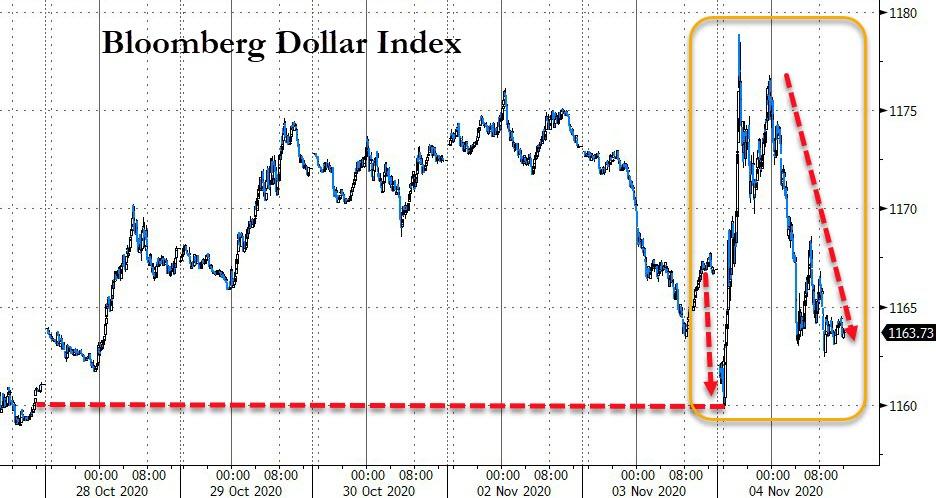

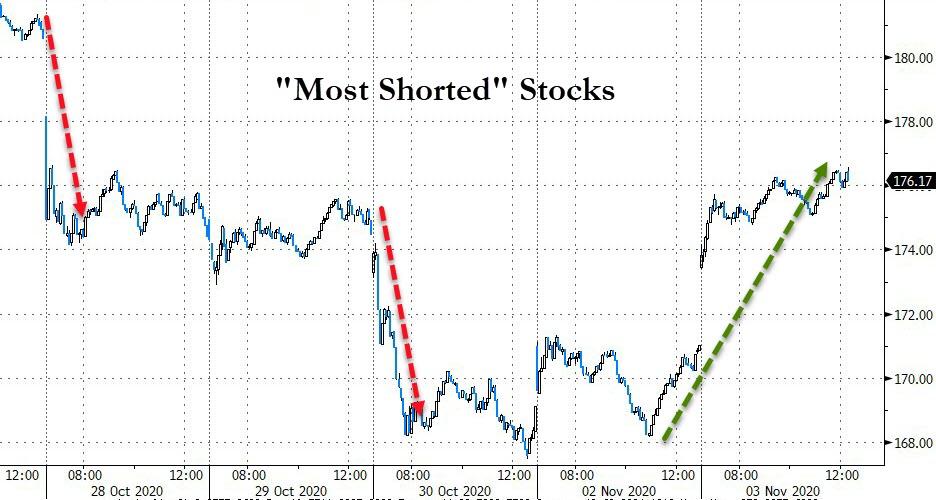

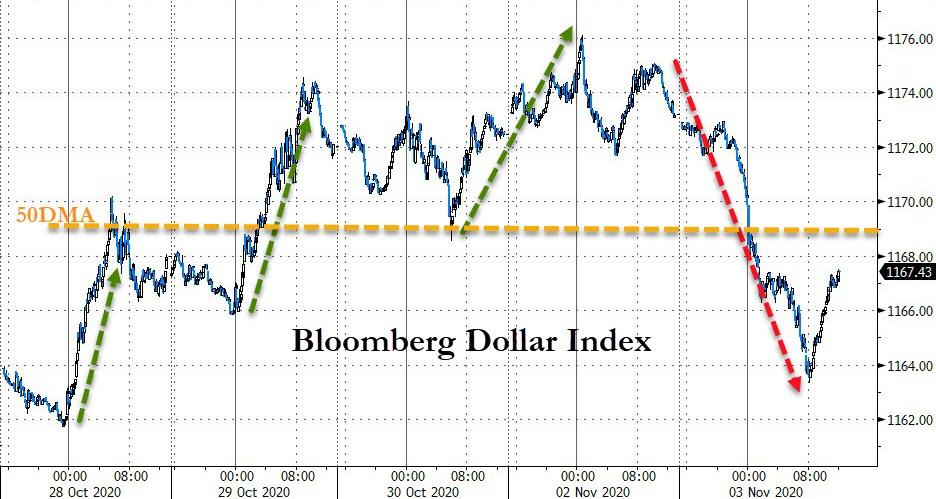

In the end, stocks soared led by the Nasdaq, bond yields tanked, and the US dollar got clobbered. The combination of lower bond yields and a declining dollar was like pouring fuel on the fire for gold, which ripped higher with spot gold actually outperforming the major indexes for the session.

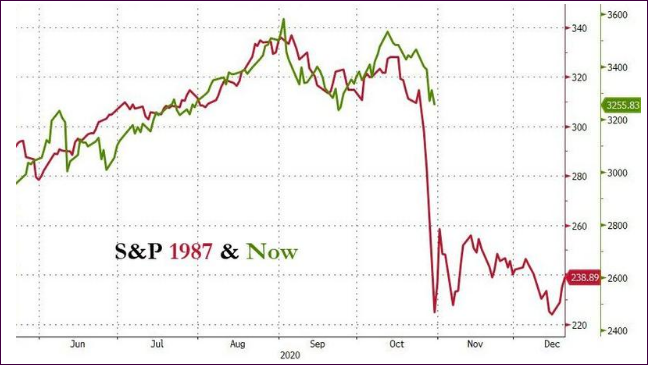

Of course, as great as this rally feels, we must be aware that much is hype and not based on economic fundamentals, as this separation of “soft” vs. “hard” survey data shows. Additionally, the SMART money is not participating at all, and has not since August, which is demonstrated in this chart.

That’s why our exit strategy will always be an ever-present component of our Trend Tracking strategy.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}