- Moving the markets

Despite weakness in the futures markets, the computer algos went to work this morning by pushing the major indexes to another green close with the S&P 500 gaining around +1.4%, while crude oil dumped -23%.

We saw two assists supporting equities.

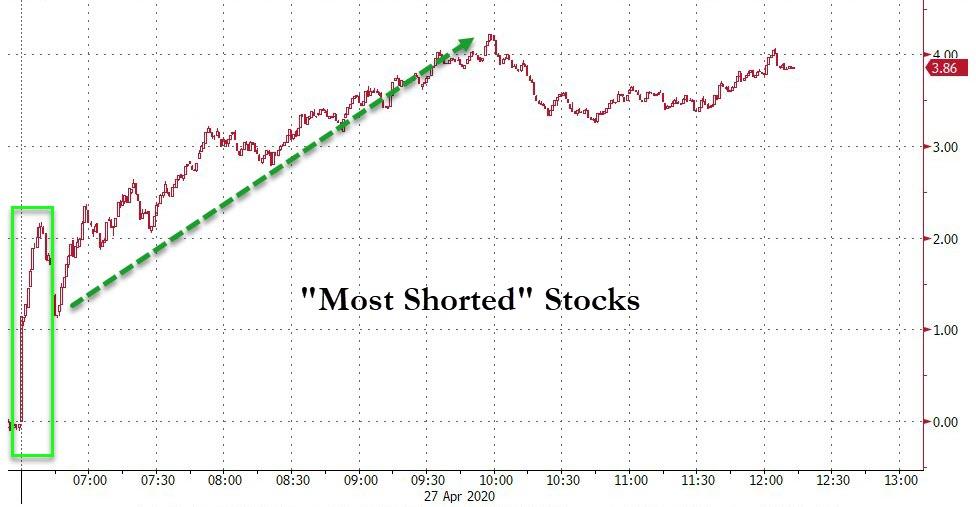

One came from a giant short squeeze causing US stocks to surge, as Bloomberg’s chart shows. The other one, of a more global nature, came from BoJ’s promise to buy more assets, which pumped global markets, with especially the Nikkei being on fire.

This wiped out last week’s losses, as traders’ optimism about loosening restrictions took center stage, despite the usual warnings that such early moves could be premature and backfire.

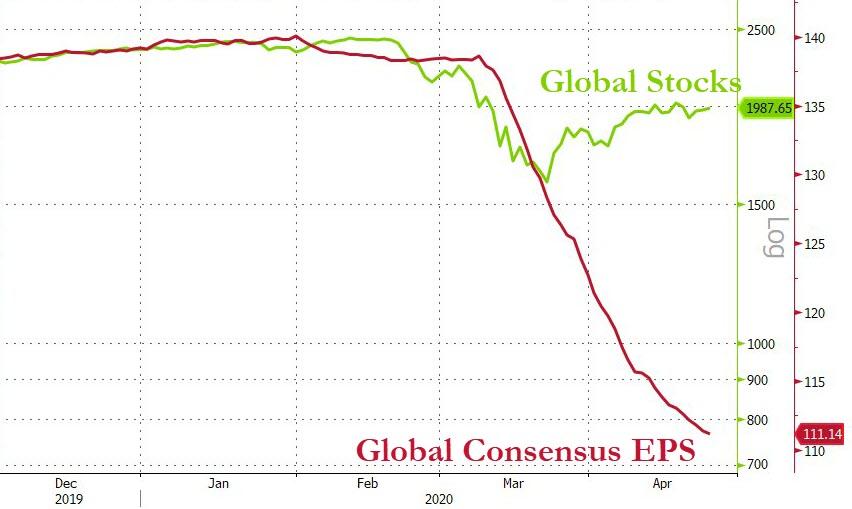

The busiest week of the earnings season has started with negative news being widely expected, which is another reason why markets are in rally mode confirming once again that bad news can be good news. But for how long?

Guggenheim’s CIO Scott Minerd chimed in by saying:

“The central bank will never be able to get back to normal. The Fed’s balance sheet has expanded from $4.5 trillion to $6.6 trillion in just about a month, and it is likely on its way to over $9 trillion soon.”

With ZeroHedge concluding:

“And there you have it: the US is now (and has been for the past decade) just a more dignified form of USSR-style central planning, one where prices are set by decree and a decline in asset levels is prohibited for one simple reason: with financial assets over 6x global GDP, any crash in markets would result in a depression that would promptly spiral in social collapse.”

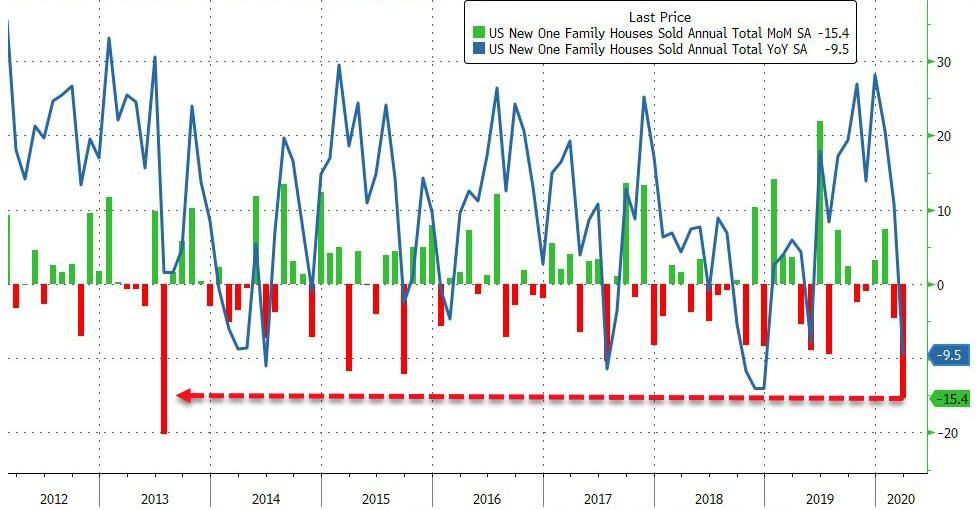

Words of wisdom indeed. In case you were wondering, this is exactly why markets are totally disconnected from any reality. Even the real economy, as demonstrated by crude oil, is disintegrating at the same time as earnings expectations are dumping, and not just in the US but globally as well.

This week is loaded with a variety of events, any of which could force the markets in either direction.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}