Do you want to know which ETFs are hot and which ones are not? Then you need my High-Volume ETF Cutline report. It tells you how close or far each of the 311 ETFs I follow is from its long-term trend line (39-week SMA). These are the ETFs that trade more than $5 million a day, so they are not some obscure funds that nobody cares about.

The report is split into two parts: The winners that are above their trend line (%M/A), and the losers that are below it. The yellow line is the line of shame that separates them. You can see how many ETFs are in each group and how they have changed since the last report (271 vs. 272 current).

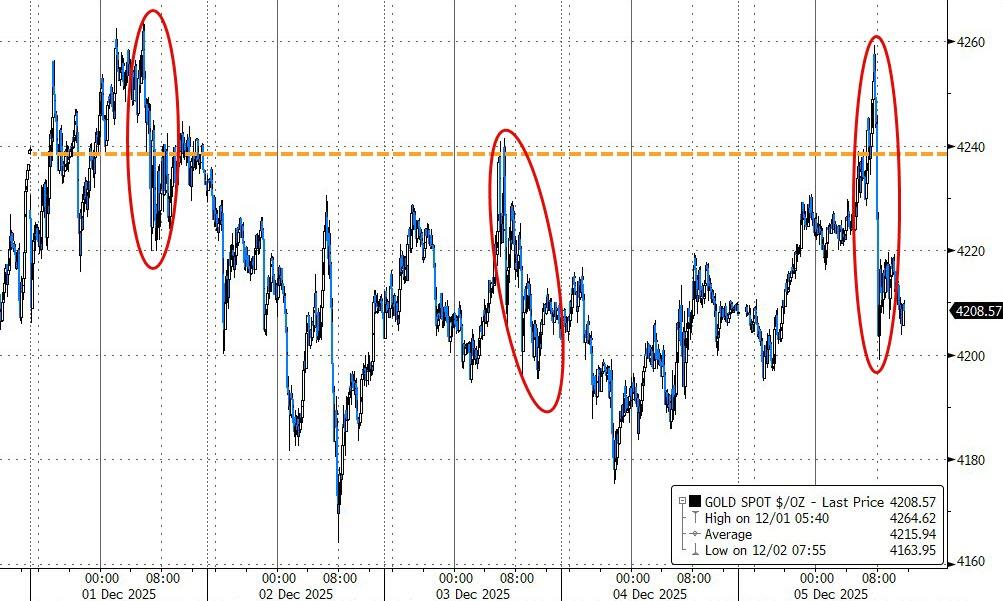

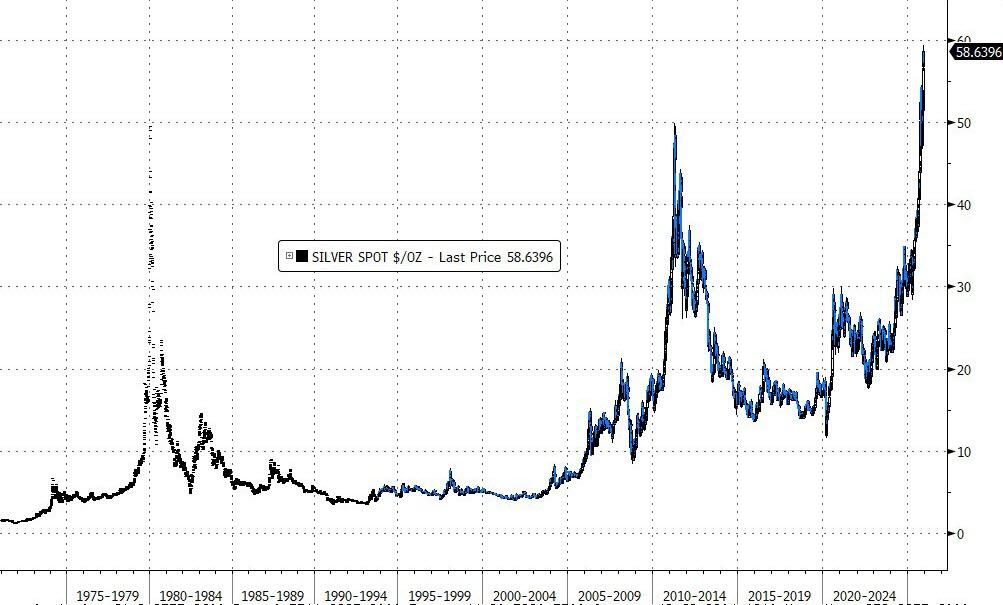

SILVER ALMOST $60, GOLD HOLDS $4,200 – METALS STILL SHINING

[Chart courtesy of MarketWatch.com]

Moving the market

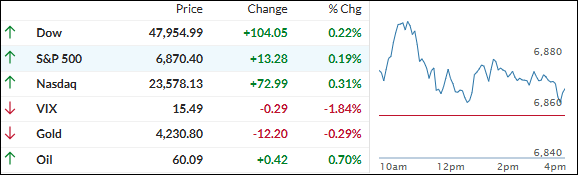

We started strong and never really let up, locking in a fourth straight green day as everyone chewed on fresh inflation data that landed softer than expected.

The big one was the delayed September Core PCE (the Fed’s favorite gauge) coming in at 2.8% year-over-year – below the 2.9% estimate.

Tame inflation + recent weak jobs numbers = pretty much locks in that quarter-point cut next Wednesday. The University of Michigan consumer sentiment survey beat expectations too, giving another little tailwind.

Stocks followed the usual script: Small Caps and Nasdaq led the week, while the S&P was the laggard (barely green after some late selling and plenty of intraday chop).

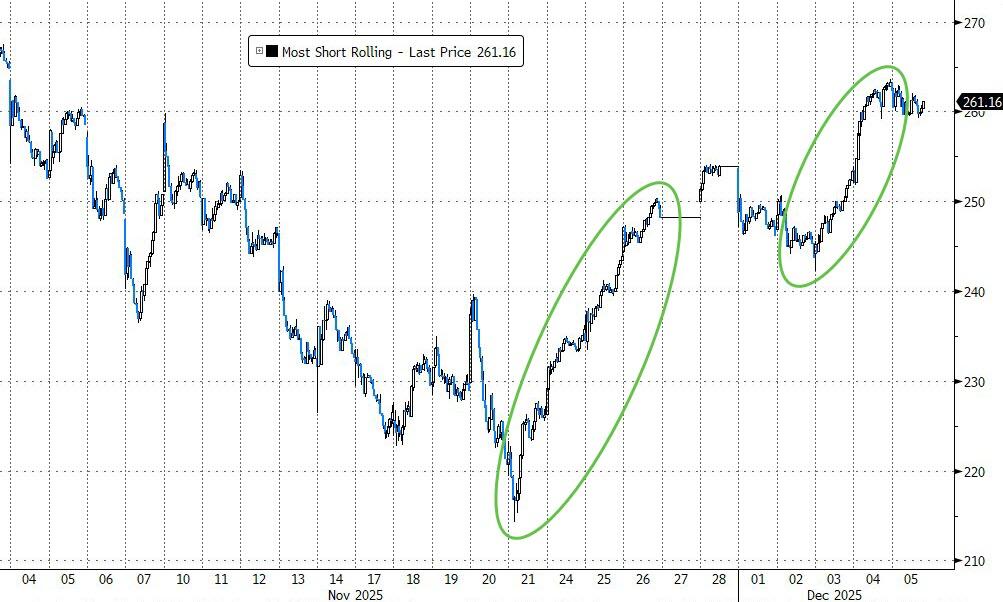

A massive two-week short squeeze – the biggest since August 2022 – helped the Mag 7 crush the rest of the S&P 493.

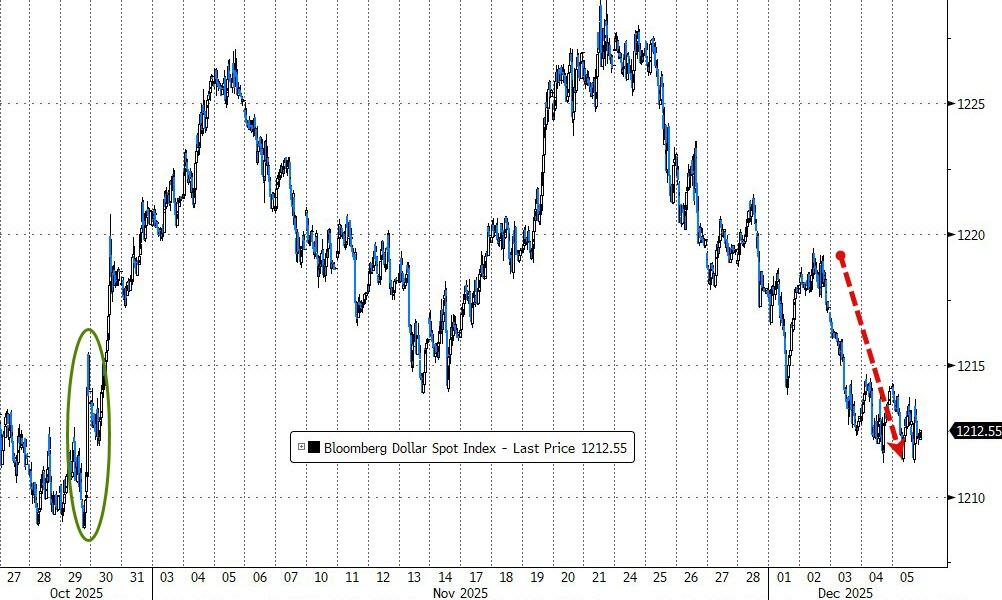

Bond yields rose on the week, the dollar fell for the fourth time in five weeks, gold gave back a little but stayed comfy above $4,200, and silver was the real rockstar – blasted to a new record high, nearly kissing $60 before settling just under.

Bitcoin cooled off from mid-week highs around $94K and closed the week below $90K.

Quick thought as we’re heading into Fed week:

With the cut basically priced in and inflation looking cooperative, are we setting up for the classic “buy the rumor, sell the news” move next Wednesday, or will the Santa rally just keep rolling right through it?

ETF Data updated through Thursday, December 4, 2025

How to use this StatSheet:

Out of the 1,800+ ETFs out there, I only pick the ones that trade over $5 million per day (HV ETFs), so you don’t get stuck with a lemon that nobody wants to buy or sell.

Trend Tracking Indexes (TTIs)

These are the main indicators that tell you when to buy or sell Domestic and International ETFs (section 1 and 2). They do that by comparing their position to their long-term M/A (Moving Average). If they cross above, and stay there, it’s a green light to buy. If they fall below, and keep going, it’s a red light to sell. And to make sure you don’t lose your shirt if things go south, I also use a 12% trailing stop loss on all positions in these categories.

All other investment areas don’t have a TTI and should be traded based on the position of each ETF relative to its own trend line (%M/A). That’s why I call them “Selective Buy.” In other words, if an ETF goes above its own trend line, you can buy it. But don’t forget to use a trailing sell stop of 12%, or less if you’re feeling nervous.

If some of these words sound like Greek to you, please check out the Glossary of Terms and new subscriber information in section 9.

DOMESTIC EQUITY ETFs: BUY— effective 5/20/2025

Click on chart to enlarge

This is our main compass, the Domestic Trend Tracking Index (TTI-green line in the above chart). It has broken above its long-term trend line (red) by +6.43% and remains in “Buy” mode, with our new holdings being subject to our trailing sell stops.

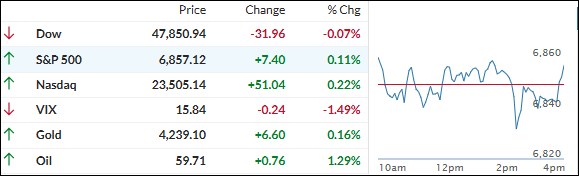

The day felt like the market was stuck in neutral—early trading was super quiet as everyone digested more signs the job market is cooling off.

The Challenger report showed U.S. companies have now announced over 1 million job cuts this year (blame restructuring, AI, and tariff worries), and yesterday’s weak ADP payrolls number added to the pile.

Traders basically shrugged at today’s weekly jobless claims hitting their lowest since September 2022 and focused on the big picture: the labor market is softening enough that a December Fed rate cut feels like a lock.

Markets are now pricing an 89% chance of a quarter-point cut next Wednesday—way up from just a couple weeks ago. That dovish vibe kept things calm, even though it was a choppy, directionless session overall.

Small caps were the clear winners (short squeeze still in full swing), while the rest of the market just bounced around.

Bond yields crept higher, the dollar finished flat, gold squeaked out a tiny win and got back above $4,200, and bitcoin gave back some of its recent gains to settle around $92K.

On a brighter note, for wallets: average gas prices nationwide just dipped below $3.00/gallon for the first time since May 2021 (California folks… yeah, we’re still paying the premium).

Tomorrow, we get consumer sentiment, personal income/spending, and—most importantly—the September Core PCE number, the Fed’s favorite inflation gauge.

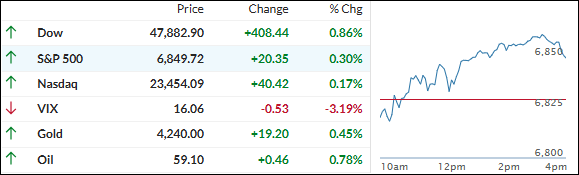

Stocks got off to a wobbly start but eventually found their legs, with all the major indexes closing in the green, led by the Dow while the Nasdaq lagged a bit.

Traders spent the day digesting weaker economic data and what it might mean for the Fed’s next move as the last policy meeting of the year approaches.

Microsoft slipped about 2% after headlines claimed it was cutting AI-linked software sales quotas, a story the company pushed back on. Other big AI names moved lower in sympathy, with Nvidia slightly in the red, Broadcom off more than 1%, and Micron Technology down around 2%.

The tone improved after ADP’s report showed private payrolls unexpectedly falling by 32,000 in November instead of rising, as economists had forecast.

That weak reading, along with a sharp dive in broader U.S. macro data, reinforced the idea that the Fed is now effectively locked into a rate cut next week, turning this into yet another “bad news is good news” day for risk assets.

Rate-cut expectations stayed pinned at 100% for December and even ticked higher for January, with odds for an additional move next month climbing above 30%.

Small Caps enjoyed a strong session thanks to a hefty short squeeze, and many AI-related names joined that rebound trade, even if some mega caps finished mixed.

In the background, bond yields edged lower, the dollar extended its pullback, and gold managed a modest gain while silver basically went sideways.

Bitcoin added to yesterday’s strength and pushed above $93,000, and copper quietly turned in a standout performance with a solid move higher.

ZeroHedge also highlighted how heavily this year’s S&P 500 returns have leaned on a handful of AI giants—without them, the index would have delivered less than half of its nearly 19% year-to-date gain.

With so much riding on a small group of AI leaders and the Fed seemingly one weak data point away from more easing, the big question is whether this “bad news is good news” dynamic can keep propping up the market—or if concentration risk and a softening economy will eventually catch up with the bulls.

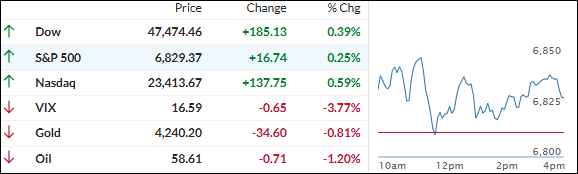

Stocks bounced back today, helped by a strong rebound in Bitcoin and a solid move higher in big tech, as traders tried to shake off December’s shaky start.

The major indexes spent most of the day climbing, helped by renewed appetite for growth and AI names after Monday’s stumble.

Bitcoin surged throughout the session, wiping out the prior day’s losses and reinforcing its recent pattern of trading in step with rising odds of a December Fed rate cut.

AI-linked tech also did its part: Oracle reversed the previous session’s slide, Nvidia added nearly 2%, and AI infrastructure names like Credo Technology and Astera Labs ripped higher, with Credo jumping about 17% to a record and Astera tacking on roughly 6%.

Even so, this bounce comes after the major U.S. indexes snapped five-day win streaks on Monday, as persistent worries about sticky inflation, stretched valuations, and uncertain AI payoffs have kept a lid on enthusiasm.

Rate expectations remain a key driver: markets now see an almost 90%-plus chance of a cut at the Fed’s December 10 meeting, a big jump from mid-November, giving bulls a narrative to lean on even as the macro picture looks mixed.

Around the edges, bond yields eased a bit, the dollar dipped late in the day, and precious metals took a pause without breaking their uptrends.

Gold held above the 4,200 level, and silver, after being hit early, clawed back to finish above 58—keeping the “metals as quiet leaders” story intact for now.

With only a handful of data releases due tomorrow, and some of them fairly stale, the near-term tape may stay more focused on Fed odds, AI sentiment, and crypto’s mood swings than on the economic calendar.

With rate-cut hopes firming, AI names heating back up, and Bitcoin acting like a high-beta play on Fed expectations, the key question now is whether this rebound can build into a more durable December run—or if one more bout of anxiety will knock the rally off course again.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}