Below, please find the latest High-Volume ETF Cutline report, which shows how far above or below their respective long-term trend lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s StatSheet and includes 322 High Volume ETFs, defined as those with an average daily volume of more than $5 million, of which currently 131 (last week 114) are hovering in bullish territory. The yellow line separates those ETFs that are positioned above their trend line (%M/A) from those that have dropped below it.

In case you are not familiar with some of the terminology used in the reports, please read the Glossary of Terms. If you missed the original post about the Cutline approach, you can read it here.

Even though the futures markets jumped supported by trade deal optimism, as China showed willingness to step up purchases of US farm goods to comply with the phase one trade agreement. Traders, however, quickly dismissed the story as being laughable.

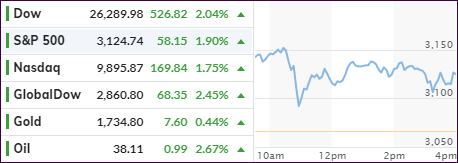

As a result, a slow and steady descent took the major indexes back into the red, and they bounced along their respective unchanged lines for the remainder of the session ending up with modest losses. The exception again was the Nasdaq, which eked out a tiny gain.

Not helping the bulls and contributing to the decline were several news reports. First, Apple Computers announced that it will be re-closing 11 of their stores in various states due to rising cases of coronavirus.

Not to be outdone, the World Health Organization (WHO) said the virus has entered a “new and dangerous phase,” which caused concern about the widely but wrongly assumed V-shape economic rebound.

Despite these negatives, today’s quadruple options expirations had no measurable market effect with the S&P 500 still squeezing out +1.88% for the week.

ZH summarized the week like this:

Well that was a week of worrisome headlines (from World War 3 to global COVID re-awakenings), awe-inspiring US macro-economic beats (which lose all context in relation to the collapse) as earnings outlooks remain just “off the lows”, and a stock market that refuses to go down despite bonds, the dollar, and commodities all signaling anything but strong growth ahead…

Our Trend Tracking Indexes (TTIs) slipped at tad, but the Domestic one still hovers in the neutral zone keeping our investments intact. However, I break-out will occur, the only question is “will it be to the upside or downside?”

There’s a good chance that we will find out next week.

1. From the universe of over 1,800 ETFs, I have selected only those with a trading volume of over $5 million per day (HV ETFs), so that liquidity and a small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and 2), are made based on the respective TTI and its position either above or below its long-term M/A (Moving Average). A crossing of the trend line from below accompanied by some staying power above constitutes a “Buy” signal. Conversely, a clear break below the line constitutes a “Sell” signal. Additionally, I use a 7.5% trailing stop loss on all positions in these categories to control downside risk.

3. All other investment arenas do not have a TTI and should be traded based on the position of the individual ETF relative to its own respective trend line (%M/A). That’s why those signals are referred to as a “Selective Buy.” In other words, if an ETF crosses its own trendline to the upside, a “Buy” signal is generated. Since these areas tend to be more volatile, I recommend a wider trailing sell stop of 7.5% -10% depending on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

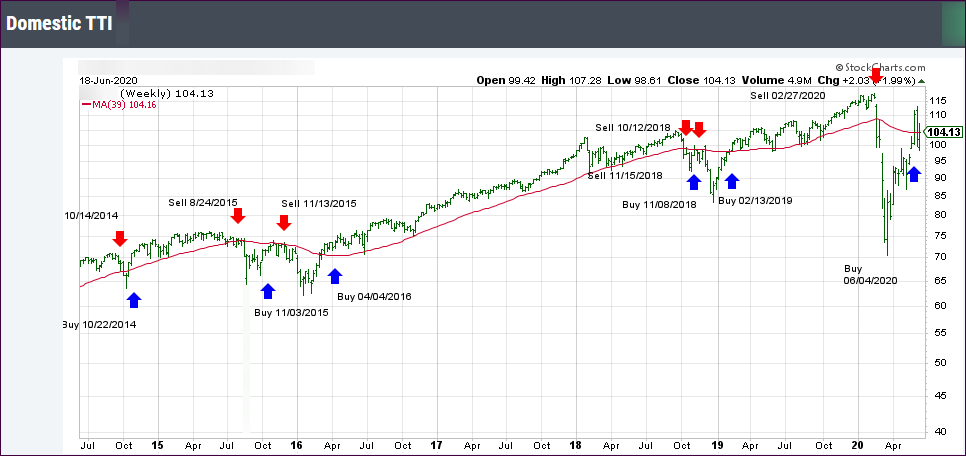

1. DOMESTIC EQUITY ETFs: BUY— since 04/06/2020

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) has now dropped below its long-term trend line (red) by -0.10% after having generated a new Domestic “Buy” signal effective 06/04/20 as posted.

A lack of commitment to push the markets one way or the other was noticeably absent today, as the major indexes vacillated aimlessly around their respective unchanged lines.

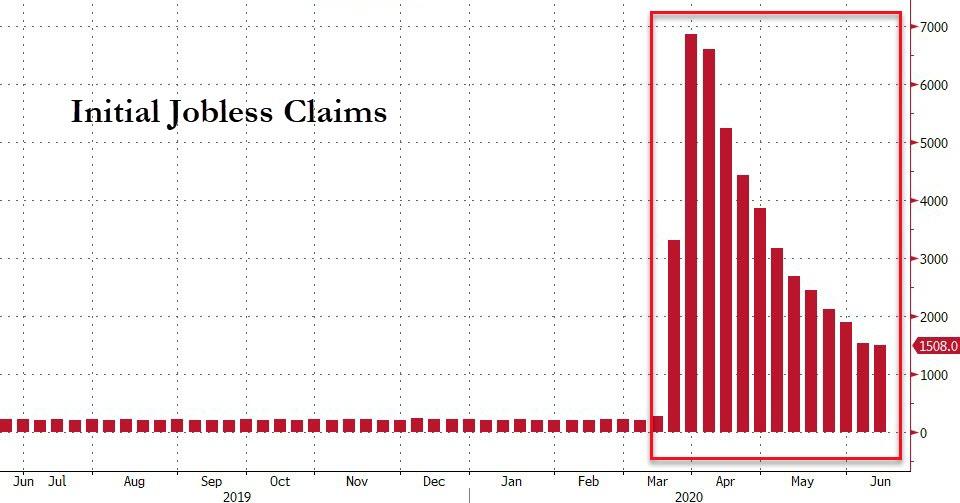

Not much was gained or lost, but the Nasdaq closed in the green. Today’s report on unemployment claims showed that 1.508 million more Americans filed for first-time benefits, which was worse than the 1.29 million expected.

This brings the total number of claims, since the lockdowns began, to 46 million with no end in sight, but Bloomberg’s chart shows that downward momentum may have slowed some.

ZH noted:

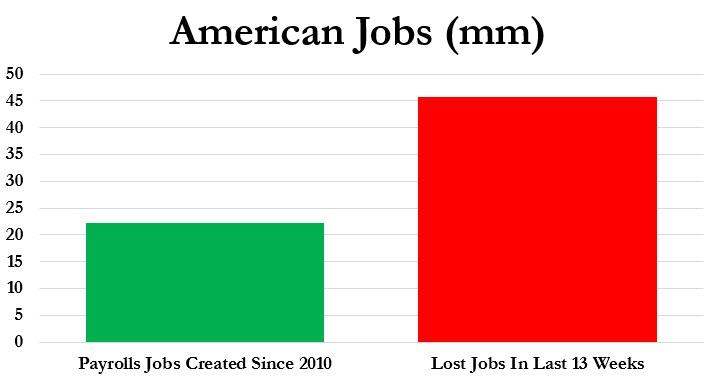

What is most disturbing is that in the past 13 weeks, more than twice as many Americans have filed for unemployment than jobs gained during the last decade since the Great Recession (22.13 million gained in a decade, 45.714 million lost in 13 weeks)

Finally, it is notable, we have lost 388 jobs for every confirmed US death from COVID-19 (117,717).

This story is far from being over because what happens when the stimulus and bonus checks stop arriving after July 31st?

Noted Bloomberg:

Earnings dropped in the first quarter by 16%, the biggest decline since 2008, and are poised to fall again in the second quarter because of business disruptions tied to the coronavirus. Yet the S&P 500 has recovered most of its 34% plunge after setting a record in February.

Today’s tight trading range only had a small impact on our Trend Tracking Indexes (TTIs), which you can see in section 3. On deck is tomorrows huge option expirations’ day, the volatility of which will certainly push the indexes around more sharply compared to what we saw today.

After three days of gains, the major indexes traded near their respective unchanged lines but dove into the red during the last hour. The exception was the Nasdaq, which gave up mid-day gains but ended up in the green.

Contributing to the sell-off were reports that coronavirus cases were on the rise in at least 9 US states and China, but hope remains that a quick recovery will be still possible. Fed chair Powell continued with his second day testimonial before Congress, and while emphasizing the lasting toll of the pandemic, he also suggested that unemployment benefits should be extended.

Powell also said some form of unemployment insurance should continue past the expiration date of July 31 and defended the central bank’s more than $2 trillion slate of emergency funding to keep credit flowing during the pandemic.

Overall, the trading range of the indexes was relatively small, but that could change in a hurry with an uptick in volatility.

As ZH explained, first, there is a massive option expiration set for this Friday the 19th with some $1.8 trillion in SPX options to expire, which makes it the 3rd largest non-December expiration on record.

Second, there is massive pension selling ahead towards the end of the month, at the tune of $76 billion, due to outperformance of stocks over bonds this quarter. The required rebalancing makes this an unavoidable event.

The question is: “How much downside will come into play and will it affect our current bullish theme?”

Since no one has that answer, we will need to be prepared for either scenario.

The futures markets kept bullish momentum alive based on news that a live-saving steroid, dexamethasone, was found to cut the risk of coronavirus death by 35% for patients on ventilators, and 20% for those on supplemental oxygen without intubation.

How this will turn out is everyone’s guess at this time, but it was enough to ramp the markets higher. This momentum put a fire under the Dow, as the regular session got underway, with the index sporting a 700-point gain after the opening bell.

Giving an assist was Fed chair Powell’s testimony before Congress and his suggestion that more fiscal stimulus might be needed before the American economy can make a full recovery from the coronavirus pandemic.

With the Fed now having admitted to buying individual corporate bonds as well, stocks and equity ETFs are on deck and will most likely come into play after another 20% market drop.

Added Global Market Monitor:

The United States is on the fast track to a Japanese style zombie economy, where the Nikkei 225 is still 45 percent below its December 1989 high, even after massive fiscal stimulus and quantitative easing, which includes direct equity purchases by the central bank. Japan is also a net saver and the U.S. is not.

Technical analyst Sven Henrick saw it this way:

But it’s not just the Fed. Yesterday’s announcement was apparently not enough as the Trump administration suddenly tossed a trillion-dollar infrastructure plan soundbite on top of the liquidity fire. Also, on the heels of a 10% correction. How convenient. Whether that plan ultimately materializes or not is beside the point, futures reacted and squeezed vertically even higher. What a circus. Not a stable market and my mantra of the extremes getting ever more extremes continues to hold true.

In the olden days future growth came about because the system was allowed to cleanse itself and new business models sprung to fruition from the ashes. Inefficient businesses went bust; new businesses were formed. Corporate debt was reduced. That’s called a cleansing and new innovation.

Be that as it may, the markets rallied strongly also supported by soaring retail sales in May after a disaster number the month prior.

Thanks to today’s levitation, our Domestic TTI (section 3) rallied back above its long-term trend line thereby confirming our bullish position—at least for the time being. We are seeing market absurdity, and I am sure that increased volatility and sudden reversals are here to stay.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}