ETF Tracker StatSheet

You can view the latest version here.

WHEN GOOD NEWS IS BAD NEWS—OR MAYBE NOT?

- Moving the markets

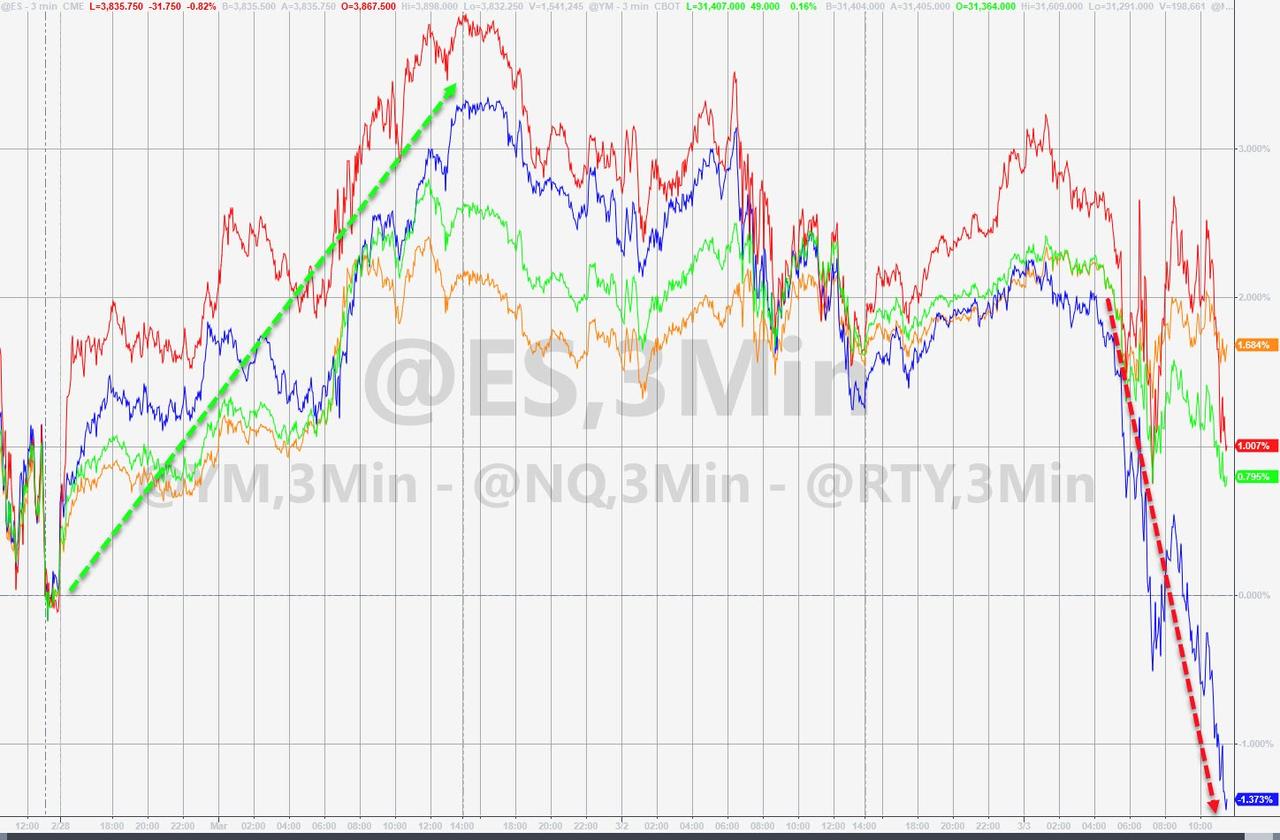

Another wild ride in the markets turned out to be positive, after an early pump was followed by a huge dump, which then formed the base to be a springboard for the ramp into the close.

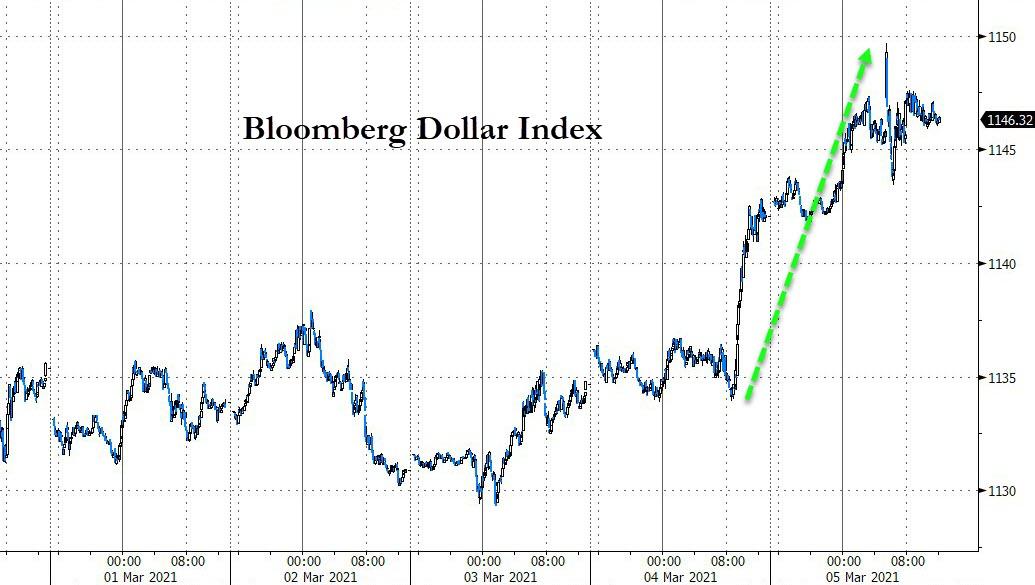

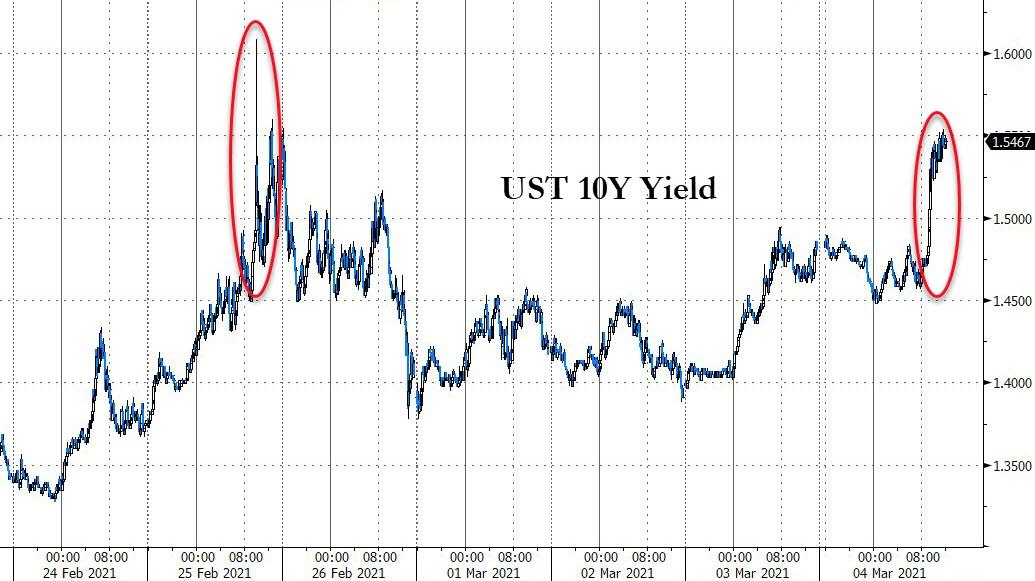

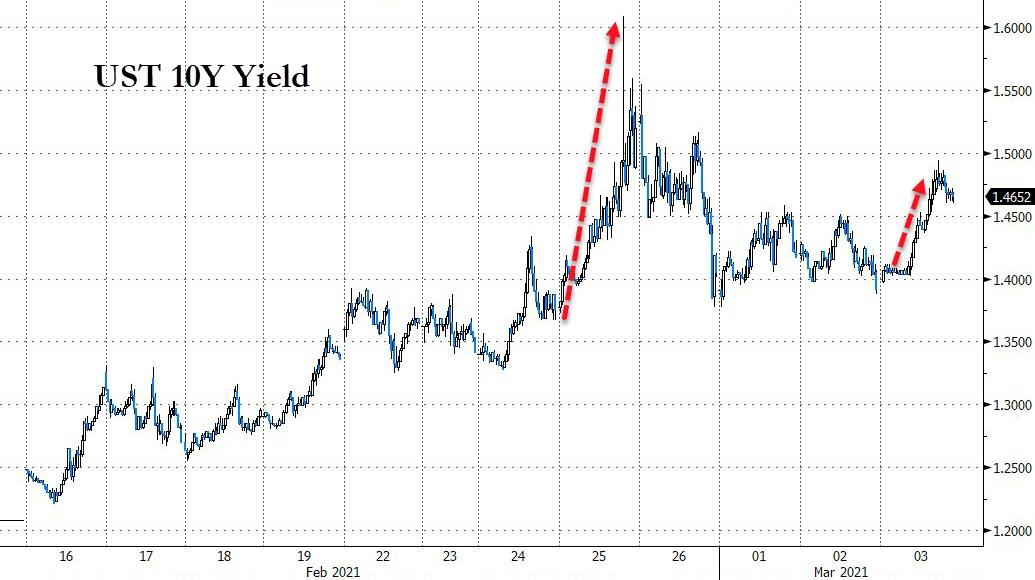

The early slam was the result of a better-than-expected improvement in the labor markets with the unemployment rate dipping to 6.2% and payrolls gaining 379k (good news), which is not what traders wanted to see. This news sent bond yields surging, with the 10-year spiking above the 1.60% level.

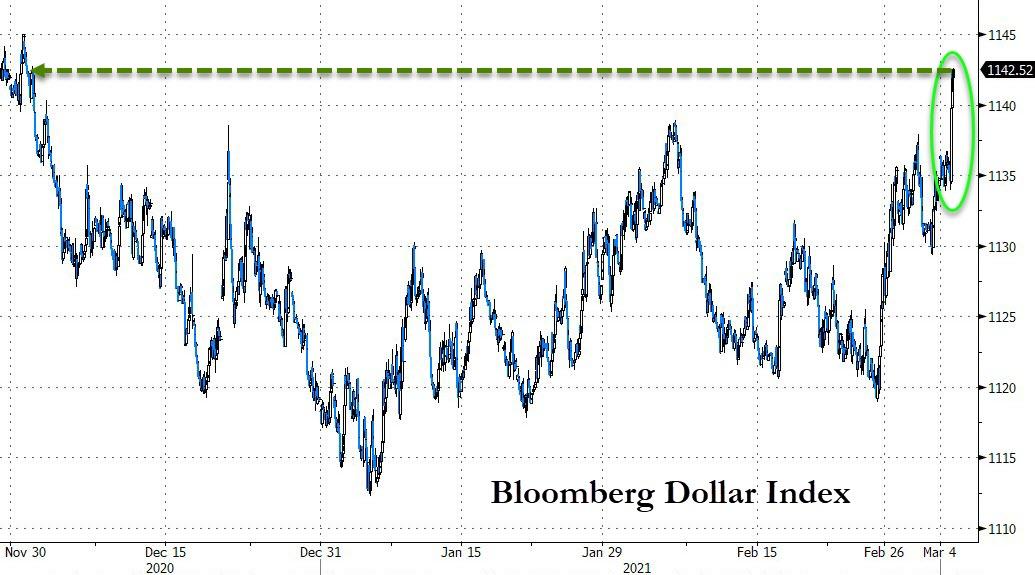

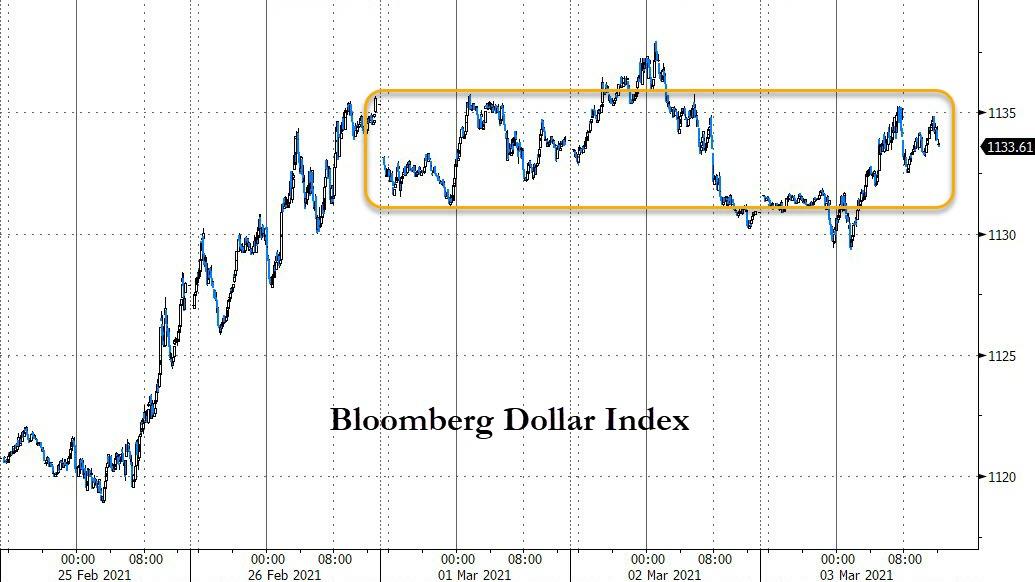

That in turn sent the US Dollar index sharply higher and triggered massive selling in stocks with the Nasdaq leading the way to the downside. One of our more volatile holdings, which had triggered its trailing sell stop yesterday, was liquidated, and will be replaced next week.

Our newly added SmallCap value ETF performed exceptionally well by adding +2.76%, thereby outperforming its “growth” cousin by a wide margin.

Easing bond yields around mid-session, with 10-year dropping to 1.56%, was enough of a motivator to drive the markets back up with all 3 major indexes ending the day close to their highs. Given the low level the Nasdaq had fallen to, it was its biggest intraday comeback in over a year.

Added ZH:

Today was utter chaos – just look at the swings in small caps! From +2% pre-open, to down 2.5% as SHTF, and back up to gains over 2% into the close…

The swings today were very technical nature – S&P ripped back up to test its 50DMA from below, Nasdaq bounced off its 100DMA, Dow bounced off its 50DMA, and Small Caps ripped back up above their 50DMA intraday…

Volatility exploded this week causing wild swings in all asset classes, in part due to Fed head Powell’s not very encouraging comments that that the economy sees “transitory increases in inflation…I expect that we will be patient.”

Hmm, makes me wonder if that type of meaningless jawboning will be enough to keep the markets calm and elevated.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}