Traders and investors alike tried to digest Fed head Powell’s comments that interest rates may be hiked with twice the magnitude (50 bps) as had been assumed (25 bps) due to inflation “being much too high.”

Despite that hawkishness, the markets are considering Powell’s current and future planned increases as a policy error, with Wall Street clearly focusing on the long-term implications rather than the immediate ones.

Even though, it’s simply odd and not sustainable that markets can rally on “easing” and rally on “tightening” news, this aberration will end sooner or later. However, this chart clearly shows the upside-down world we are in.

Traders are aware that rate hikes will continues throughout 2022, but the Fed will have to ease again during 2023/2024, with the foregone conclusion being that later this year a slowdown/recession will materialize causing a reversal of policy.

In other words, a future recession and rate-cut odds will happen in sync, which allowed the major indexes to keep the current rebound alive, with support coming from a continued short-squeeze, which started on March 15.

Bond yields ratcheted higher with the 10-year adding another 8 bps and closing at 2.38%, thereby exerting more pain on bond holders, as prices got crushed. The widely held TLT (20-year bond ETF) is down -12.04% for the year. So much for the perceived security of bonds.

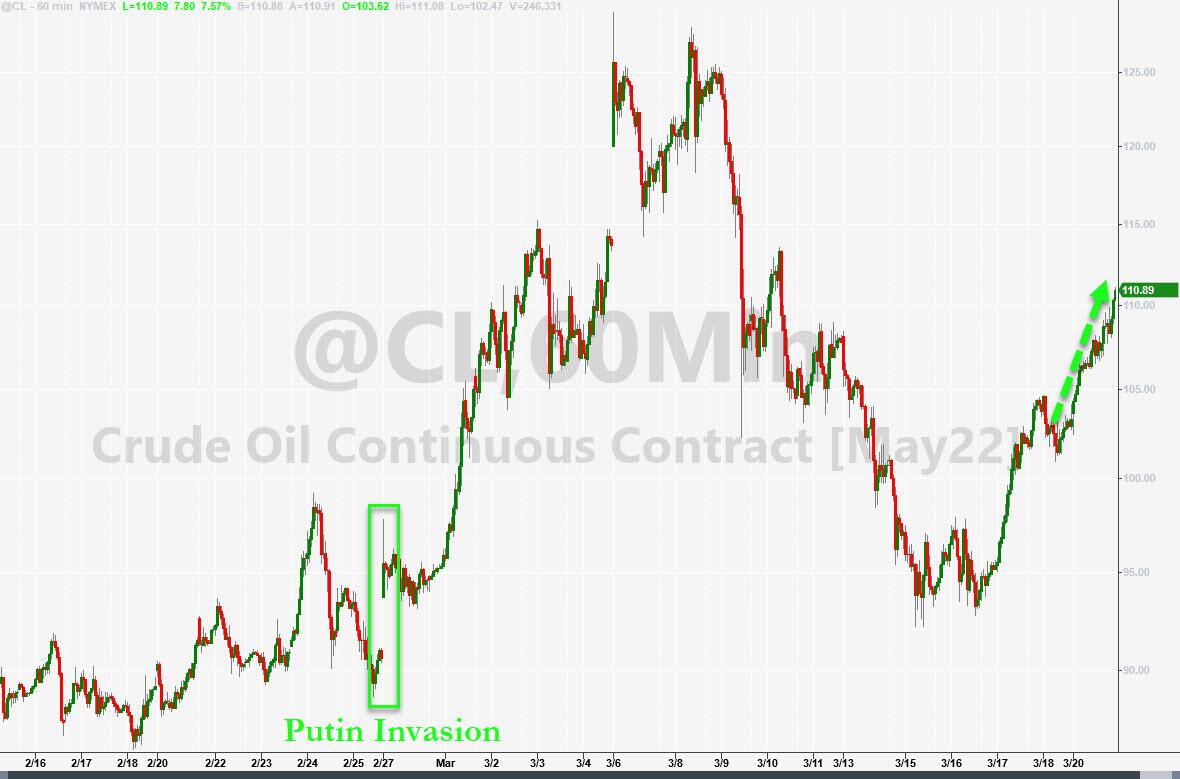

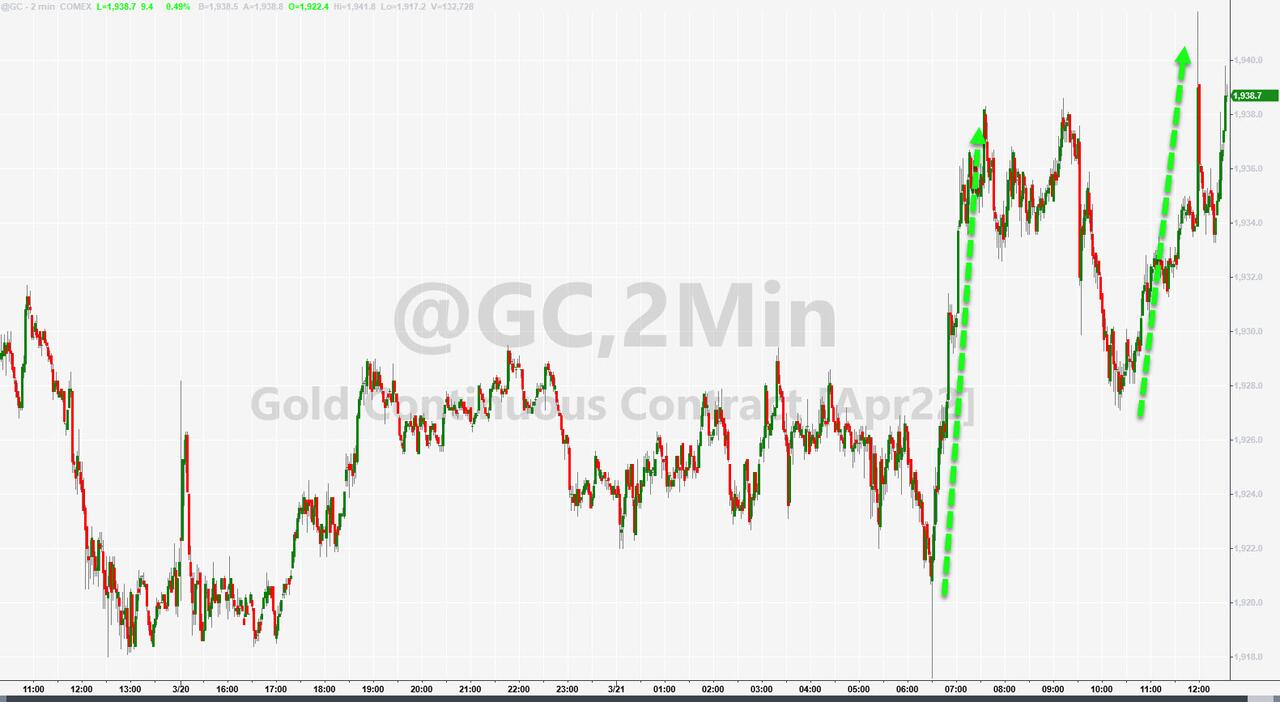

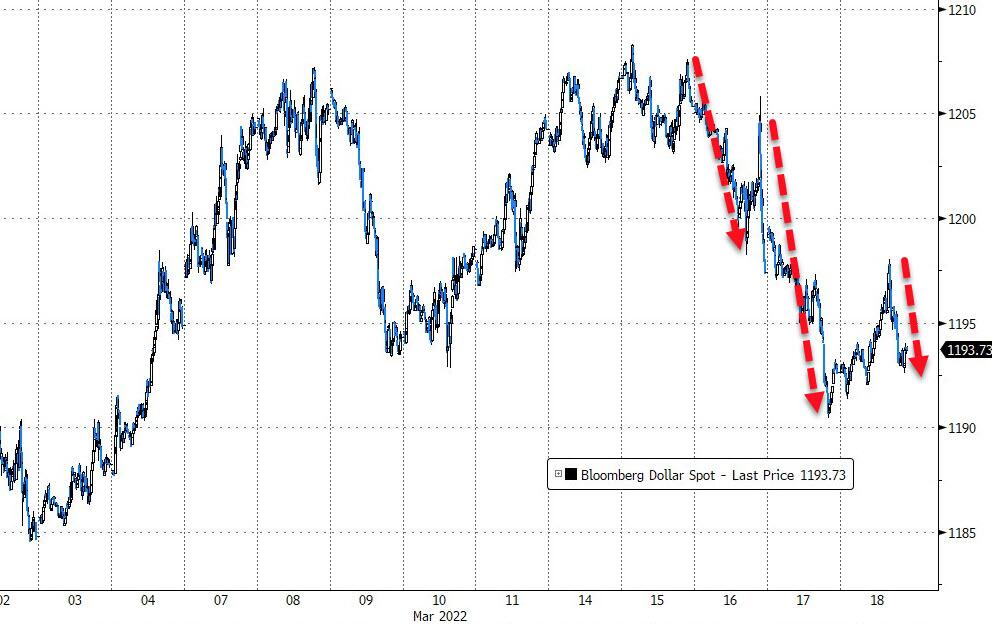

The US Dollar slipped, as did Crude Oil, with Gold initially selling off but recovering into the close with modest loss of -0.40%.

In summary, the markets are hopeful that the much-feared recession scenario will materialize, if for no other reason than that the Fed will be forced to cut rates, which is the driver necessary to propel stocks to new all-time highs in the face of deteriorating economic conditions.

Last week’s enthusiastic rally, in the face of nothing but geopolitical and economic issues, came to an end today when Fed Head Powell rang the bell on inflationary concerns while hinting at tougher responses.

After finally admitting that “inflation is much too high,” he vowed to take appropriate measures to get a better grip on prices. That pledge would take form via more aggressively hiking rates at the tune of 50 bps, should the need arise, rather than the 25 bps that had been widely circulated.

The Fed must have had some sort of awakening, with this announcement coming only a week after the first 25 bps rate hike since 2018. Here are some Fed-speak snippets as presented by ZH:

*BOSTIC SAYS HE’S NOT WEDDED TO ONLY MOVE RATES IN 25 BPS STEPS

*BOSTIC SAYS FED SHOULD GET MOVING `QUICKLY’ ON BALANCE SHEET

*BARKIN: CAN MOVE AT 50 BP CLIP AGAIN TO TAME INFLATION

*BARKIN: WE COULD MOVE FASTER, BUT ALREADY IMPACTING BOND MARKET

Commented Morgan Stanley’s Mike Wilson:

The rally in equities over the past week was one of the sharpest on record. While it could go a bit higher … we remain convinced it’s still a bear market, and we would use this strength to position more defensively.

My sentiments exactly. Because if the Fed is truly serious and follows through with hiking rates in manner that will have a noticeable effect on controlling inflation, stocks will come off their lofty levels and soon confirm that a bearish trend is in the making.

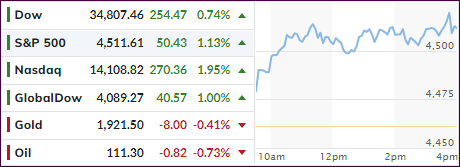

In the end, the pullback was moderate with the S&P 500 bouncing back to its unchanged line. That surprised most traders, as bond investors got spanked with the 10-year spiking an astonishing 15 bps to close at 2.305%.

Crude oil prices soared over 7% to $112, the US Dollar inched higher, while Gold pumped, dumped, and pumped to closer higher by +0.33%.

Here’s Zero Hedge’s market comparison to 2018, when the Fed last raised rates, crushing the markets in the process, only to reverse their hawkish stance and bring the bullish theme back into play.

Below, please find the latest High-Volume ETF Cutline report, which shows how far above or below their respective long-term trend lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s StatSheet and includes 312 High Volume ETFs, defined as those with an average daily volume of more than $5 million, of which currently 107 (last week 64) are hovering in bullish territory. The yellow line separates those ETFs that are positioned above their trend line (%M/A) from those that have dropped below it.

In case you are not familiar with some of the terminology used in the reports, please read the Glossary of Terms. If you missed the original post about the Cutline approach, you can read it here.

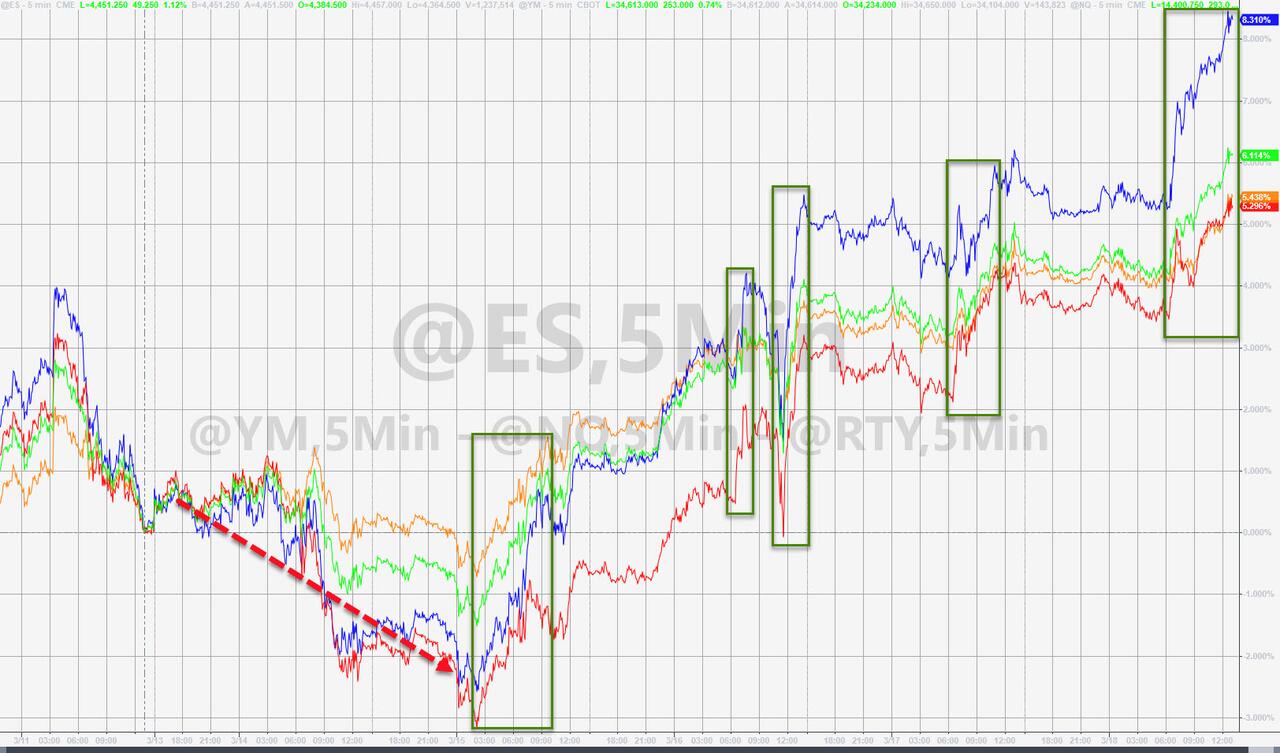

Even in the face of a $3.5 trillion options expirations fest, questionable geopolitical and economic news, along with hawkish tones from Fed Gov Waller, nothing appeared to be able to keep equities from rallying into the weekend, thereby continuing to cut down on YTD losses.

Waller insisted that data were screaming for a half-point rise in rates:

I really favor front-loading our rate hikes, that we need to do more withdrawal of accommodation now if we want to have an impact on inflation later this year and next year,” he told CNBC’s Steve Liesman during a live “Squawk Box” interview.

“So, in that sense, the way to front-load it is to pull some rate hikes forward, which would imply 50 basis points at one or multiple meetings in the near future.”

Stocks ignored the hawkish view, and the computer algos pushed the indexes to their best week in 2020, but despite this effort, the broadly held S&P 500 is still down for the year by -6.4%.

We also learned today that Existing Home Sales plunged by a bigger than expected -7.2% MoM in February, as ZH pointed out, which is its biggest MoM drop since May 2020.

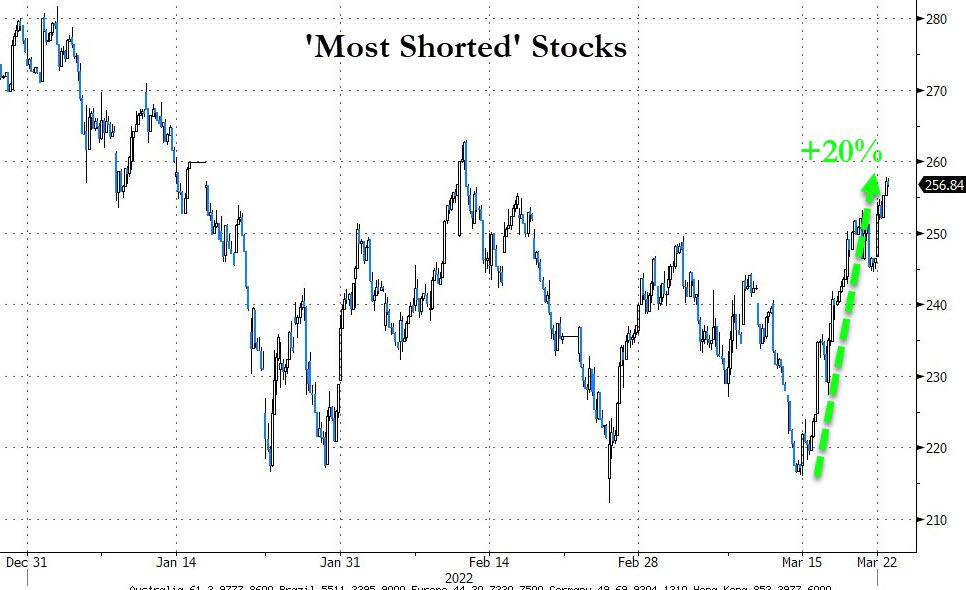

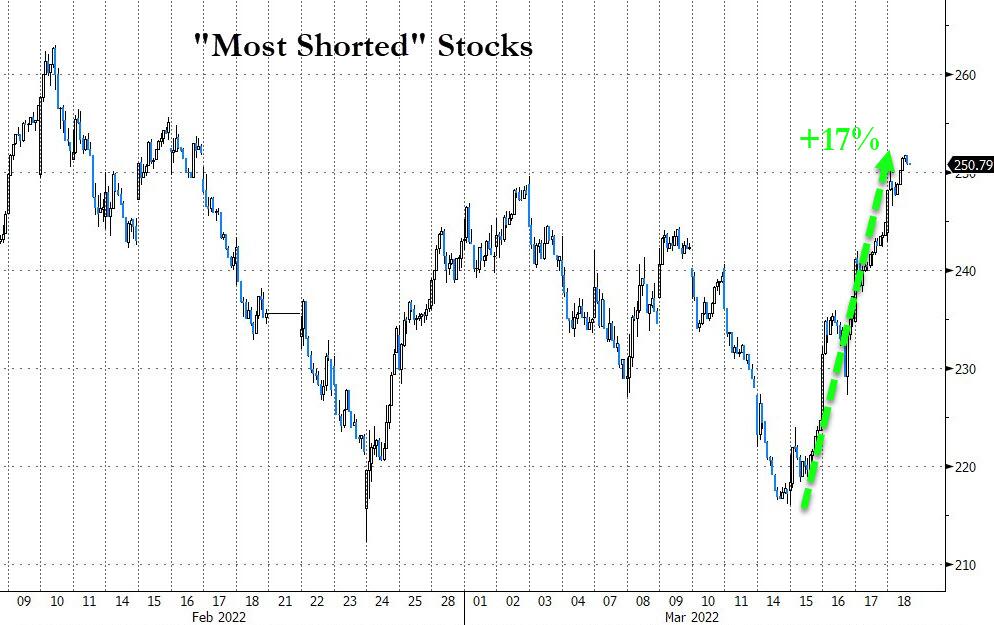

As is always the case, when stocks suddenly explode, a short squeeze is likely part of the manipulation, and this week was no exception, as the most shorted stocks were pushed sharply higher.

Bond yields rose this week, the US Dollar got hammered, and Gold bounced a few times but sold off today and remains below its $2k level. Crude oil followed a similar pattern but managed to crawl back above its $100 level.

Today’s bounce fest pushed our Domestic Trend Tracking Index (TTI) a tad deeper into bullish territory (section 3 below), which means, absent a drop in the market on Monday, I will start nibbling at adding domestic market exposure.

1. From the universe of over 1,800 ETFs, I have selected only those with a trading volume of over $5 million per day (HV ETFs), so that liquidity and a small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and 2), are made based on the respective TTI and its position either above or below its long-term M/A (Moving Average). A crossing of the trend line from below accompanied by some staying power above constitutes a “Buy” signal. Conversely, a clear break below the line constitutes a “Sell” signal. Additionally, I use an 12% trailing stop loss on all positions in these categories to control downside risk.

3. All other investment arenas do not have a TTI and should be traded based on the position of the individual ETF relative to its own respective trend line (%M/A). That’s why those signals are referred to as a “Selective Buy.” In other words, if an ETF crosses its own trendline to the upside, a “Buy” signal is generated. Here too, I recommend trailing sell stop of 12%, or less, depending on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

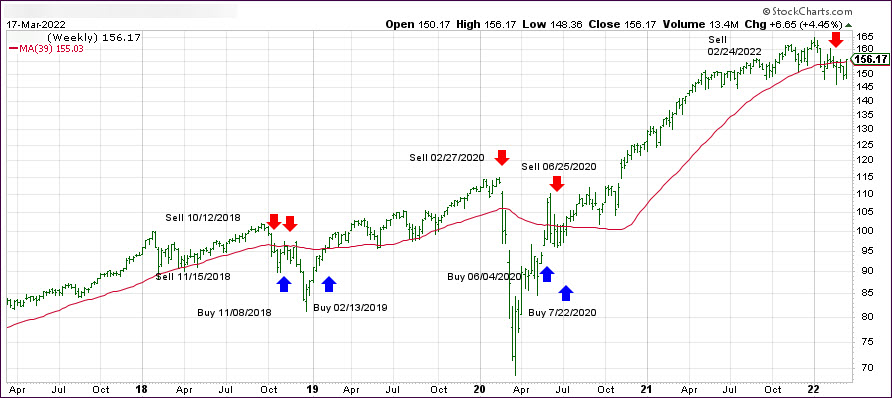

1. DOMESTIC EQUITY ETFs: SELL— since 02/24/2022

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) has just broken above its long-term trend line (red) by +0.92% and remains in “SELL” mode—although it is on the edge of moving back to the Buy side.

Equities jumped for the third straight day pushing our Domestic Trend Tracking Index (TTI) above its long-term trend line for the first time, since the effective date of our latest Sell signal on 2/24/22.

As I pointed out yesterday, the markets are ignoring all the geopolitical and economic dramas (Stagflation) and are focusing on the main driver, which can make or break bull markets, and that is Fed interest rate policy.

It’s now been widely accepted that the Fed has made a policy error and that, despite the Fed’s remaining 2 rate hikes, they will walk back their tough talk, as ZH explained:

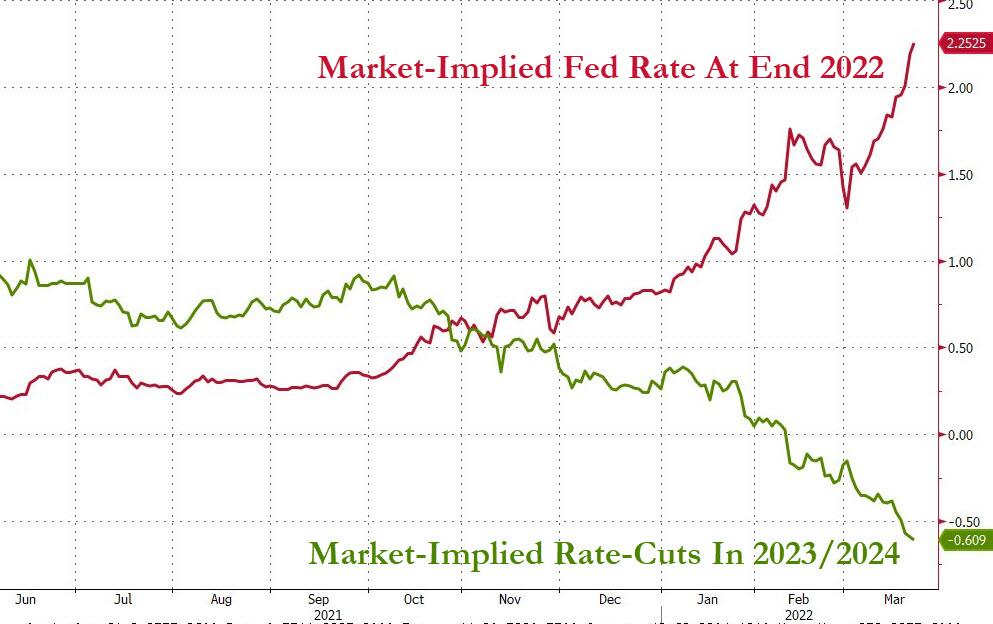

The market is now pricing in rate-hikes to 2.00% in 2022… and then a full rate-cut in 2023…

That is full policy error pricing as the market is now convinced The Fed will hike into stagflation, guaranteeing a recession, sparking rate-cuts. All of which is perhaps another reason why gold is rebounding today…

Here are some snippets from Rabobank and BofA, who called it like this:

“By the September meeting the damage from the Ukraine crisis to the global economy may become a threat to the US economic expansion. The doves in the FOMC are likely to jump from the hiking bandwagon by then and demand a pause.”

Putting it all together, Marey’s Rabobank colleague Michael Every picks up where we left off with our FOMC post-mortem, and writes that “the market is going even further. With 30-year yields dropping and US 5-10s inverting, and only 20bp to go on 2s-10s, and with stocks, gold, and crypto all up, we are now pricing for a policy error and the inevitable rate cuts and new QE that will have to follow.” In other words, and as we have been hammering for months, “just as the Fed drives things off a cliff, Mr Market is already pricing in the trampoline at the bottom of it that will take us to even higher market-y highs.”

There you have it. The markets fully anticipate the above scenario and are already counting on future rate cuts and QE, even though none of that may happen till the end of this year.

As you can see in section 3 below, our Domestic TTI has moved back into bullish territory and, should that condition hold for a couple of days, we will look for new domestic exposure next week.

Looking at the big picture, ZH added:

Meanwhile, the Russia-Ukraine conflict continues, stagflation fears are soaring (today’s Philly Fed saw growth expectations plunge, prices paid soar), COVID cases are on the rise again, China growth concerns persist, and commodity prices are rebounding again.

Let’s see what the panic-BTFD algos say tomorrow after options expirations…

Continue reading…

2. ETFs in the Spotlight

In case you missed the announcement and description of this section, you can read it here again.

It features some of the 10 broadly diversified domestic and sector ETFs from my HighVolume list as posted every Saturday. Furthermore, they are screened for the lowest MaxDD% number meaning they have been showing better resistance to temporary sell offs than all others over the past year.

The below table simply demonstrates the magnitude with which these ETFs are fluctuating above or below their respective individual trend lines (%+/-M/A). A break below, represented by a negative number, shows weakness, while a break above, represented by a positive percentage, shows strength.

For hundreds of ETF choices, be sure to reference Thursday’s StatSheet.

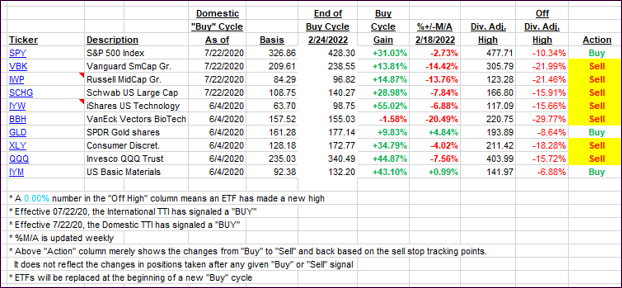

For this just closed-out domestic “Buy” cycle, here’s how some of our candidates have fared:

Click image to enlarge.

Again, the %+/-M/A column above shows the position of the various ETFs in relation to their respective long-term trend lines, while the trailing sell stops are being tracked in the “Off High” column. The “Action” column will signal a “Sell” once the -12% point has been taken out in the “Off High” column, which has replaced the prior -8% to -10% limits.

3. Trend Tracking Indexes (TTIs)

Our TTIs followed the broad market direction higher, with the Domestic one crossing above its trend line into bullish territory. I need to see more staying power before activating a new “Buy” signal.

This is how we closed 03/17/2022:

Domestic TTI: +0.92% above its M/A (prior close -0.34%)—Sell signal effective 02/24/2022.

International TTI: -0.94% below its M/A (prior close -2.18%)—Sell signal effective 03/08/2022.

Disclosure: I am obliged to inform you that I, as well as my advisory clients, own some of the ETFs listed in the above table. Furthermore, they do not represent a specific investment recommendation for you, they merely show which ETFs from the universe I track are falling within the specified guidelines.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}