- Moving the markets

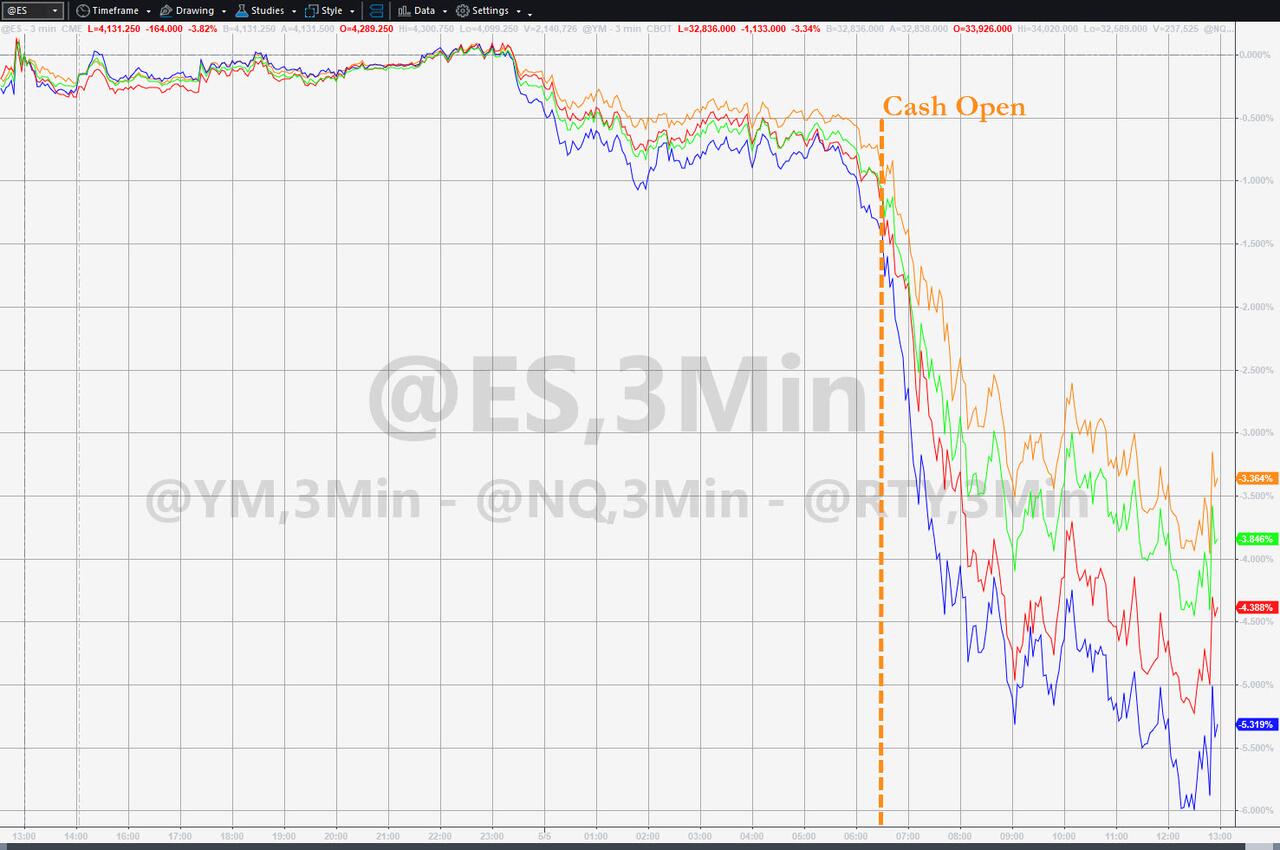

Not only did last week’s debacle continue this morning, but markets also took a sudden dive during the last hour of trading, with the S&P 500 breaching its psychologically important 4k marker to the downside to close slightly below it and at its lowest in 13 months.

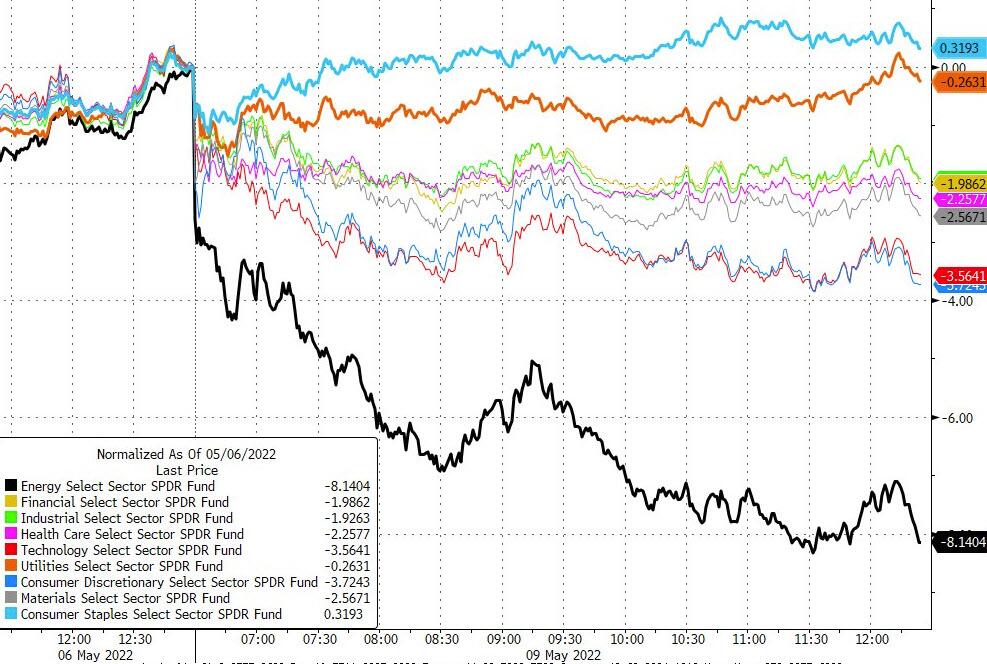

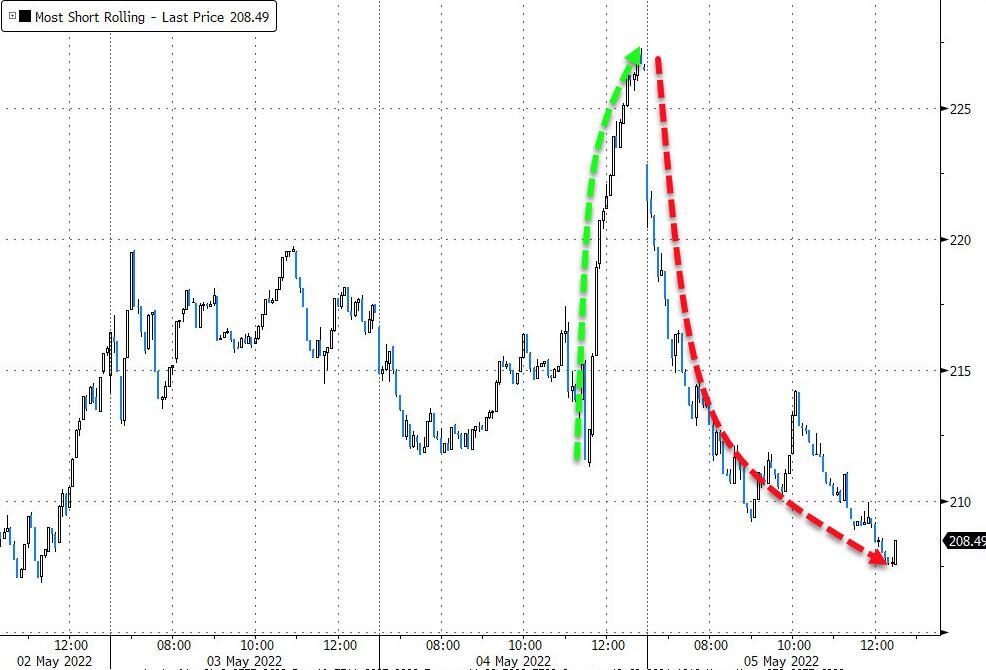

Again, this was a day with no place to hide, as even well-performing sector funds, like energy and commodities, were not immune from the onslaught of selling. Our energy sector position touched its trailing sell stop, which I took as an opportunity to get out of it and lock in some unrealized gains.

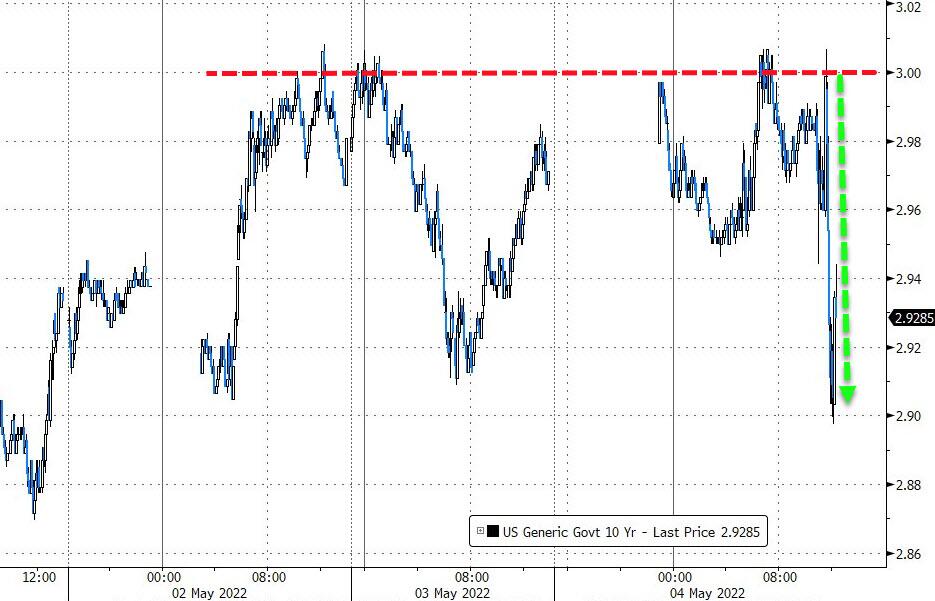

Interest rate fears had bonds swinging wildly with the 10-year slipping 9 basis points but maintaining its position above the 3% level. Rising interest rates have crushed the Nasdaq with the index caving another 4.3% today, and now down 27% from its record highs.

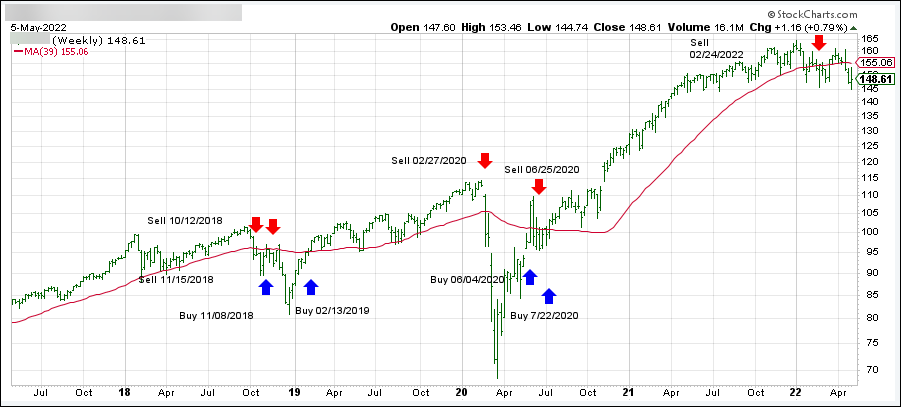

While bear market rallies can always develop suddenly, the major trend is to the downside, which had been confirmed by our Domestic TTI on 2/24/22.

As I pointed out, this is not the time to be in equities but to be in cash on the sidelines or in selected sector funds that are undergoing their own bullish trends. The Stagflation risk will be with us, which means that weakness in equities is bound to continue.

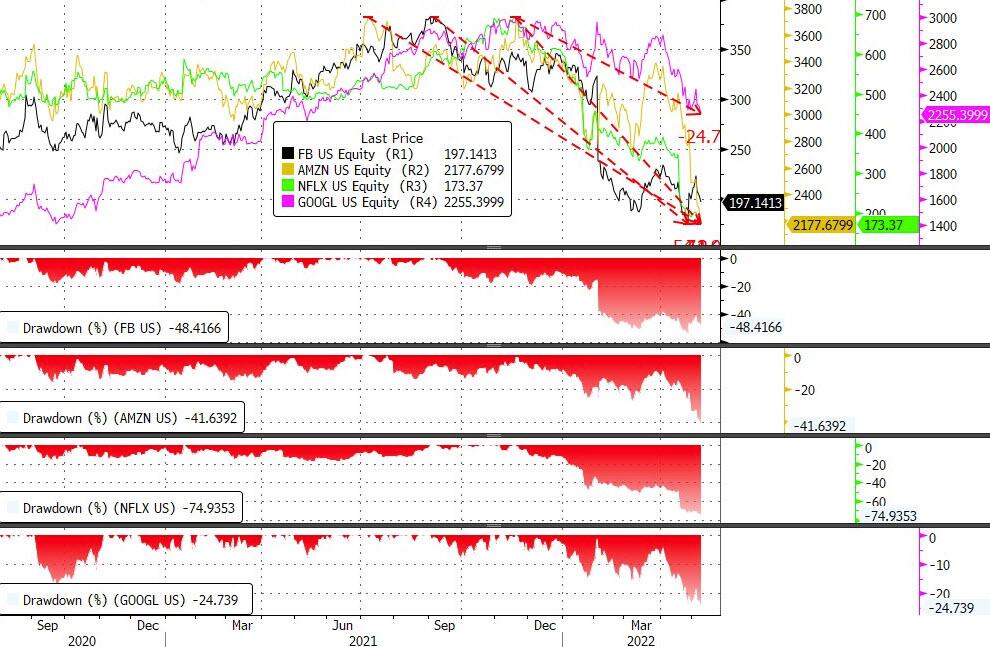

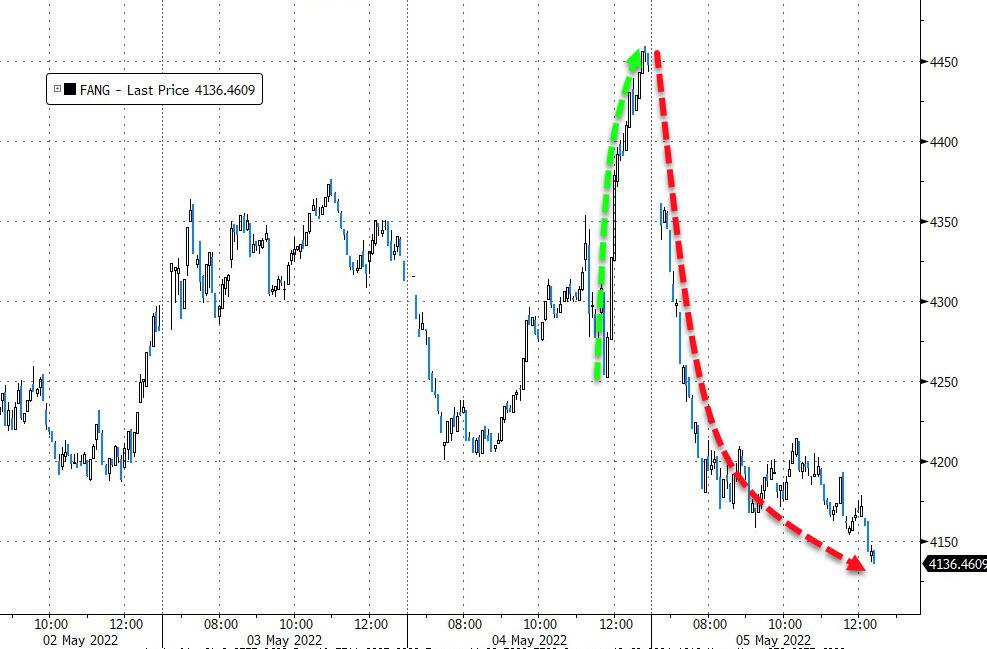

If this is not clear, ZH pointed to what happened to the Fang stocks so far:

FB -48%, AMZN -42%, NFLX -75%, GOOGL -25%

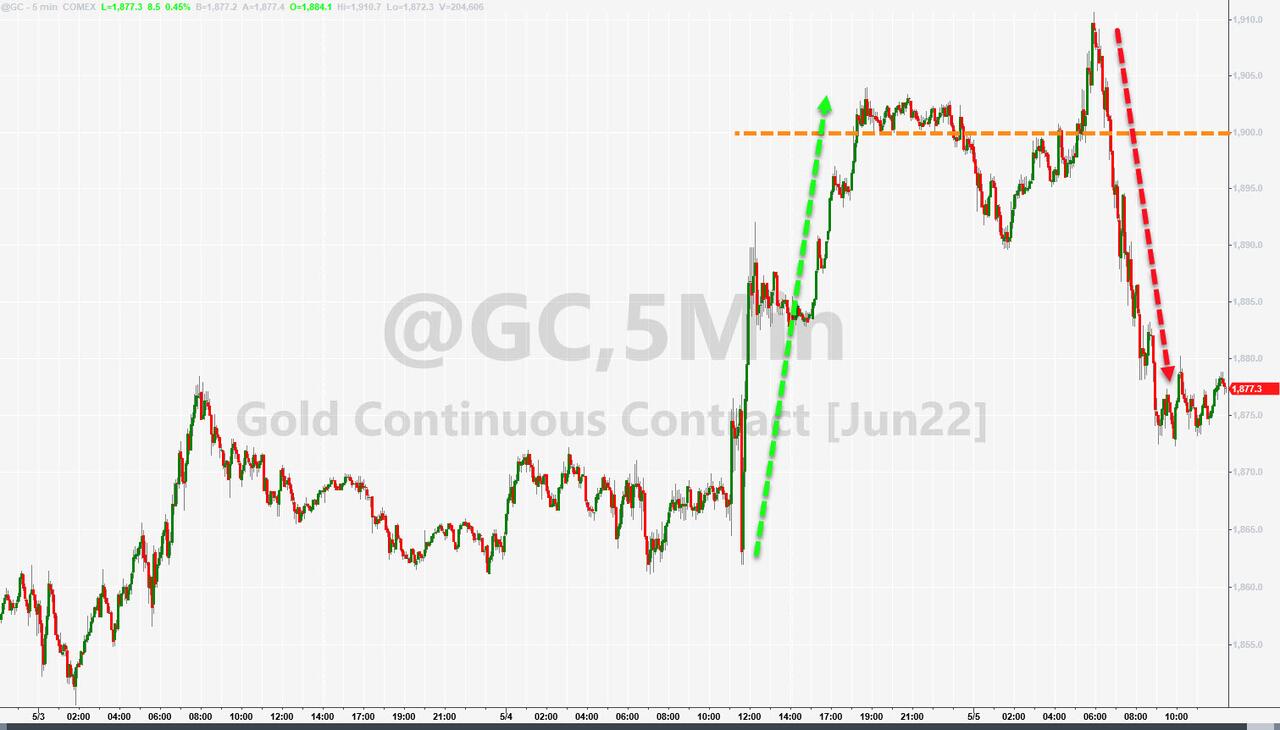

Crude oil plunged and gold tumbled, while the US Dollar went sideways and still hovers near its 20-year highs.

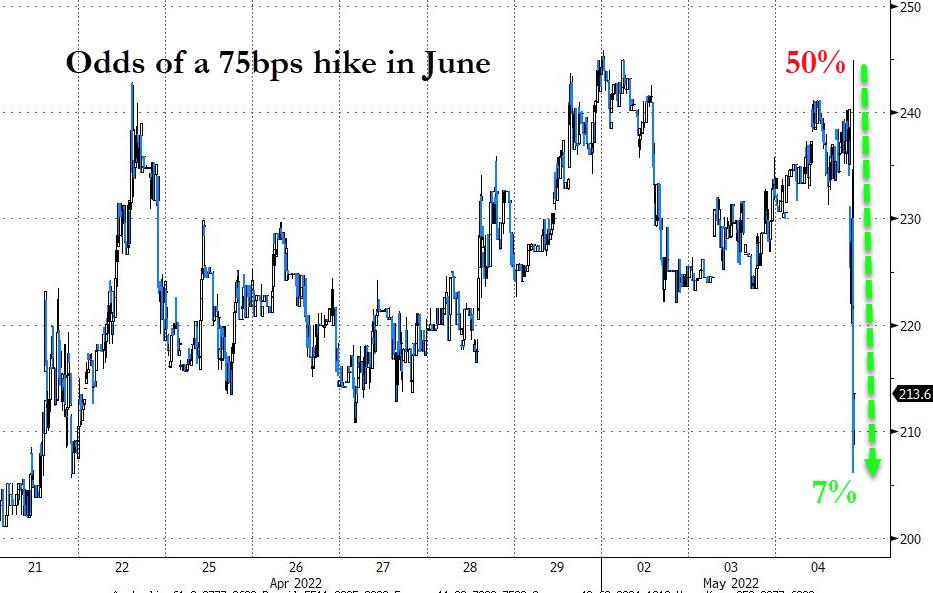

All this begs the question as to whether the Fed will fold to save the markets or be serious in its intentions to battle inflation.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}