Below, please find the latest High-Volume ETF Cutline report, which shows how far above or below their respective long-term trend lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s StatSheet and includes 312 High Volume ETFs, defined as those with an average daily volume of more than $5 million, of which currently 22 (last week 16) are hovering in bullish territory. The yellow line separates those ETFs that are positioned above their trend line (%M/A) from those that have dropped below it.

In case you are not familiar with some of the terminology used in the reports, please read the Glossary of Terms. If you missed the original post about the Cutline approach, you can read it here.

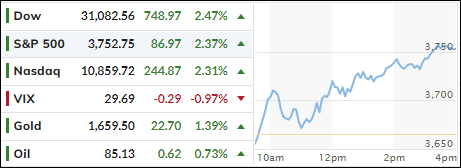

After dropping into oversold territory last week, it was time a for a bounce back, and that is exactly what we got. Despite some mid-week weakness, the major indexes found some footing and propelled themselves to a solid green close.

Surging bond yields and some disappointing earnings reports did not help, yet bullish sentiment prevailed. However, like most bounces we have seen, none of them had staying power past a few days, which means that this rebound of hope is not guaranteed to continue next week.

Added Greenlight Capital’s David Einhorn:

As long as official policy is to make the stock market go down, so that people are less wealthy, so that they buy fewer things, so that prices stop going up, all while doing nothing about fiscal policy, we believe the correct posture is to be bearish on stocks and bullish on inflation.

However, helping the bullish cause today were the Fed’s mouthpieces offering a glimmer of dovish hope mixed in with some hawkishness:

*DALY: LITTLE BIT OF PENT-UP TIGHTENING WORKING THROUGH ECONOMY

*DALY: NEED TO WATCH HOW RESTRICTIVE; CAN’T OVERTIGHTEN EITHER; REQUIRES STEP DOWN INTO SMALLER INCREMENTS OF HIKES

*DALY: THINK HARD ABOUT STEP DOWN BUT WE’RE NOT THERE YET

*EVANS: EXPECT FED TO RAISE RATES FURTHER, HOLD STANCE A WHILE

*BULLARD: STRONG JOB MARKET GIVES FED LEEWAY TO FIGHT INFLATION

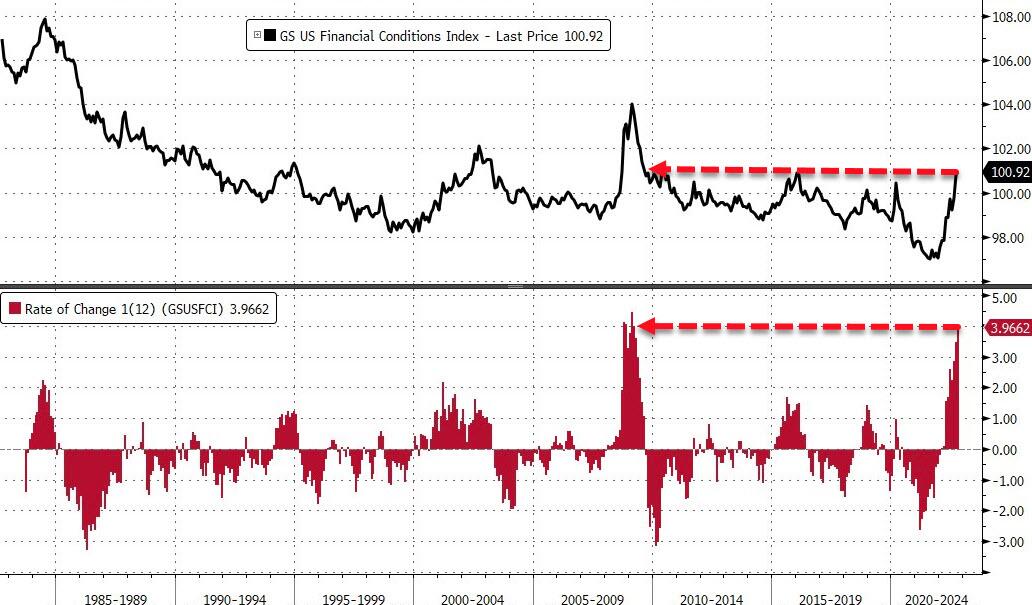

As ZeroHedge pointed out, the result was a dovish drop in terminal rate expectations, but a hawkish shift in subsequent rate-cut expectations, as this graph shows. In other words, the guesswork as to if/when the Fed will pivot continues, despite tightening financial conditions with accusations growing louder by the day that the Fed wants to “crash the economy.”

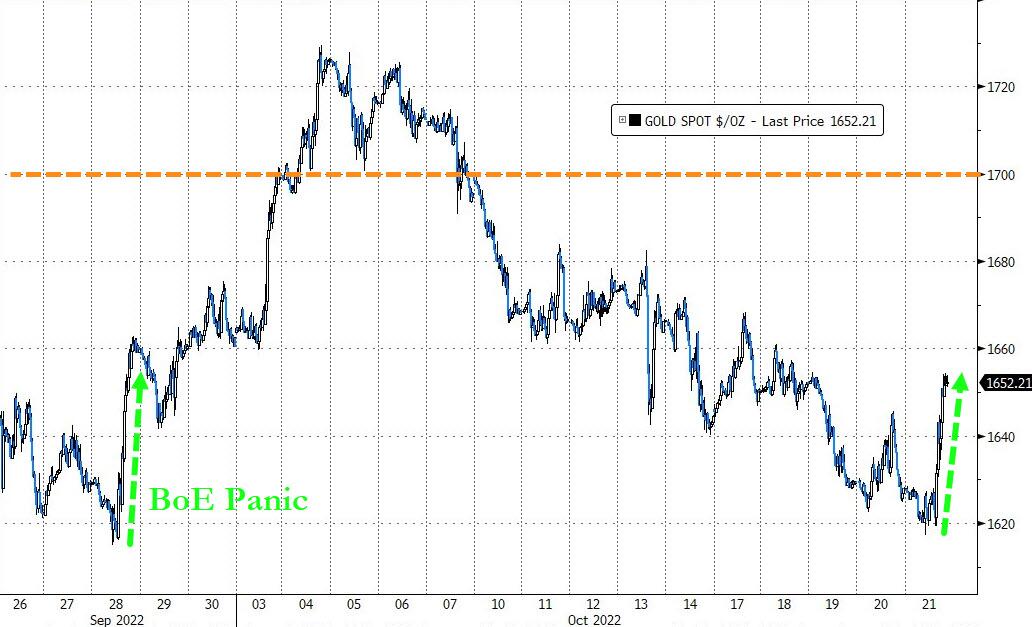

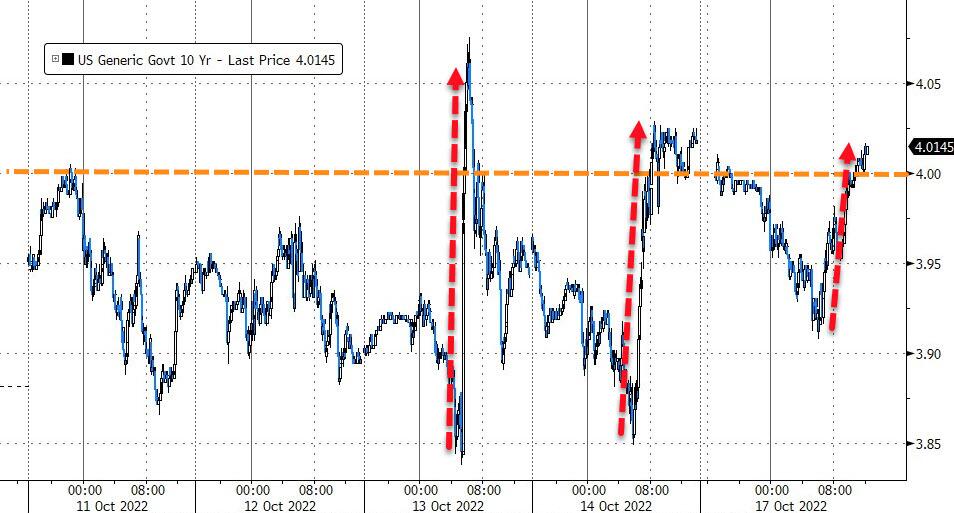

For a change, bond yields softened today, which contributed to the bullish meme, as the 10-year retreated slightly but remains firmly entrenched above its 4% level at 4.228%. The US Dollar dumped big time to its worst weekly drop since August, which helped Gold to a solid gain of +1.49% on the day.

Despite this week’s comeback, I believe the Fed is not done hiking, as much as traders like to believe it, because Fed President Bullard made that abundantly clear when he stated that “I would not call lower equity prices financial stress.” (A tip of the hat to ZeroHedge for this reference)

This risk remains to the downside, as all indications are that dollar funding around the world remains problematic, which means something could very well break in the financial system and push equities considerably lower.

Therefore, it’s wise to be in safety mode on the sidelines by favoring the return of your capital than on your capital.

ETF Data updated through Thursday, October 20, 2022

Methodology/Use of this StatSheet:

1. From the universe of over 1,800 ETFs, I have selected only those with a trading volume of over $5 million per day (HV ETFs), so that liquidity and a small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and 2), are made based on the respective TTI and its position either above or below its long-term M/A (Moving Average). A crossing of the trend line from below accompanied by some staying power above constitutes a “Buy” signal. Conversely, a clear break below the line constitutes a “Sell” signal. Additionally, I use a 12% trailing stop loss on all positions in these categories to control downside risk.

3. All other investment arenas do not have a TTI and should be traded based on the position of the individual ETF relative to its own respective trend line (%M/A). That’s why those signals are referred to as a “Selective Buy.” In other words, if an ETF crosses its own trendline to the upside, a “Buy” signal is generated. Here too, I recommend trailing sell stop of 12%, or less, depending on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

1. DOMESTIC EQUITY ETFs: SELL — since 02/24/2022

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) has broken below its long-term trend line (red) by -10.11% and remains in “SELL” mode.

Despite Netflix’s beating of earnings and revenue, and its shares rallying some 13%, it was simply not enough to overcome the negatives of surging bond yields, which indicated that inflation fears have not subsided and won’t soon.

As a result, the major indexes gave back some of their gains of the past two days, but they held up better than expected given the solid crossing of the 4% level by the 10-year yield, which closed higher by almost 12-bps to end the session at 4.128%, its highest point since July 2008.

For sure, today’s menu of bad news was not good news for the markets for a change, with UK inflation (back above 10%), Ukraine tensions, ugly housing starts, hawkish Kashkari comments and more UK government chaos could not get traders and algos to push the ‘Buy” buttons, as ZeroHedge lamented.

Rate-hike expectations shifted into more hawkish mode (higher rates) followed by higher subsequent rate-cut expectations, meaning that the prior terminal rate, the moment in time when the Fed is expected to pivot, has been pushed up a notch to about 4.977%.

This also means that the market is now pricing in a full 75-bps increase for November with odds of a 75-bps hike having risen to 60%. Unless the Fed suddenly changes its mind and pauses, rates will continue to ratchet higher and exert more pain into the equity arena.

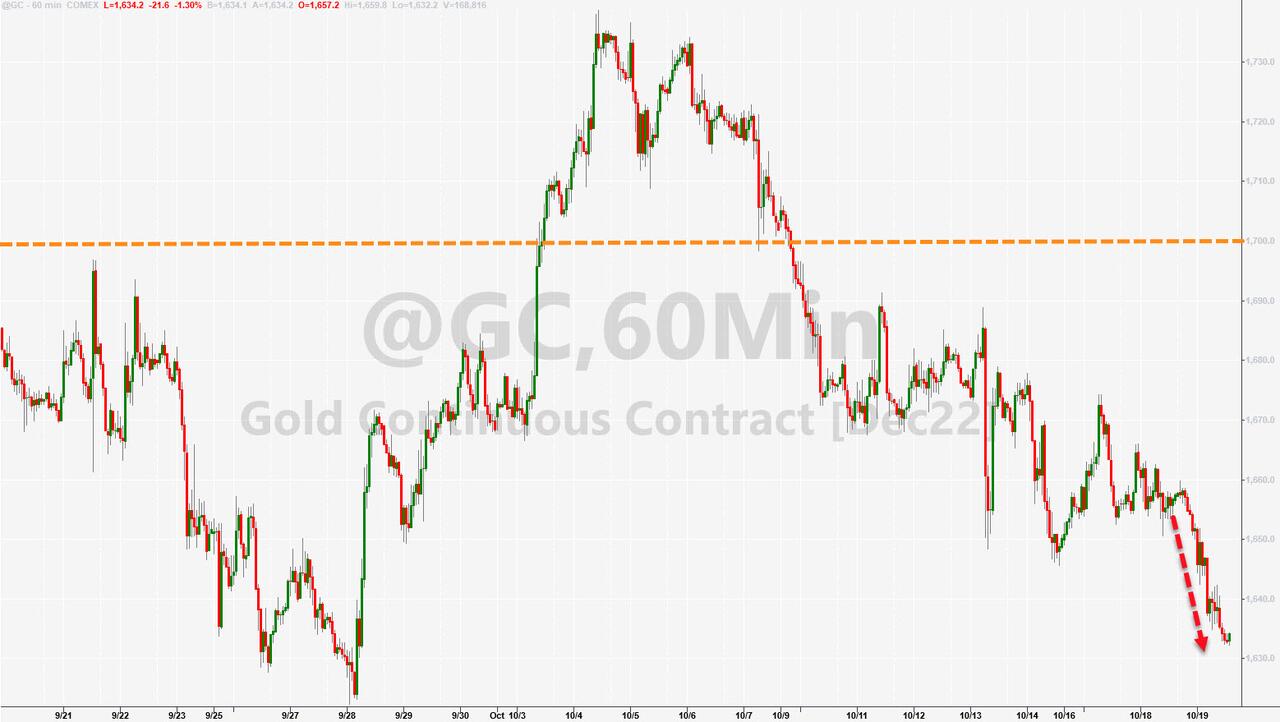

9 out of the 10 S&P sectors ended the session in the red with the lowly exception of Energy, which advanced over 3%. The US Dollar reversed its recent slide punishing Gold in the process.

Despite an early 500-point jump in the Dow, supported by strong earnings reports (Goldman Sachs, Lockheed Martin), volatility set in with the major indexes tumbling off their lofty levels. The cause was Apple reporting that it will be cutting iPhone 14 production less than 2 weeks after its debut.

Added ZeroHedge:

The news that there is just not enough demand for the trinkets and beads of the world’s largest company makes one wonder if the consumer is really as strong as the talking heads would like everyone to believe.

Uncertainty reigned and trading was choppy, as many investors seem to lack conviction that this rally has legs. According to my count, we have seen 5 occurrences when, after a rebound, the indexes dumped to make lower lows each time, which is a hallmark of bear market behavior.

This SPY chart demonstrates what the bulls had to put up with in 2022:

Will this current rebound be different?

Today, another short squeeze helped the bullish cause with the major indexes closing in the green. Bond yields chopped around and ended slightly lower with the 10-year losing its 4% level by closing at 3.99%.

Gold retreated a tad, but Crude Oil stumbled and is threatening to break the $80 barrier to the downside. With the current administration’s plan to announce more SPR releases to lower the price of gasoline at the pump, and a weakening economy, we could see the black gold take a dump into $70s.

A relief rally held its ground with the major indexes remaining steady above their respective unchanged lines, as strong bank earnings by Bank of America and Bank of Mellon provided the fuel to sustain the rebound.

Of course, stocks have been in deeply oversold territory, and are hovering near year lows of the year, with the S&P 500 having declined in four of the past five weeks. We have witnessed big moves in both directions, as apprehension has spread through Wall Street causing this roller-coaster type of swings.

Today, the pendulum swung back in favor of the bulls, which also found some encouragement by the markets now moving into the seasonally strong part of the year.

Whether that is enough to propel the rally further remains to be seen and will be impacted by the upcoming earnings season, as well as companies’ outlooks and/or revisions, along with the Fed’s policies in the face of persistently high inflation and an economic slowdown.

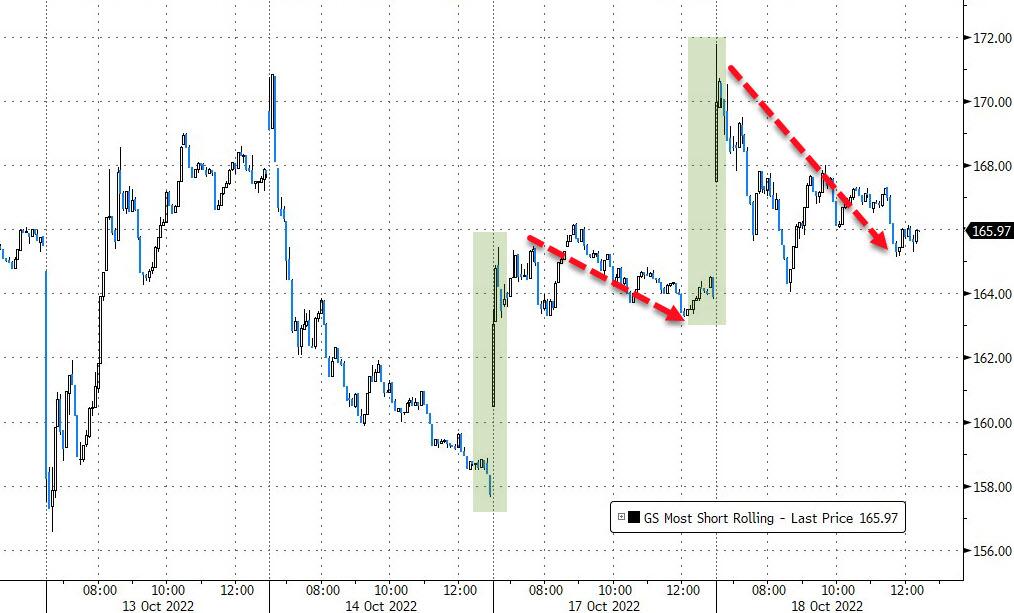

As ZeroHedge pointed out, “Friday’s bloodbath was dominated by hedge fund shorting, which set up the market for a major squeeze higher…yet again.” And that is exactly what happened, as the most shorted stocks got squeezed early on, but that was it—no follow through, which could indicate that all of the ammo has been used up.

Bond yields presented a mixed picture with the 10-year rallying back above 4% and closing at 4.02%, while the 30-year followed suit. Yields have now risen for 11 straight weeks, the longest such streak since 1978, as ZeroHedge added.

The US Dollar was in diving mode today, which helped Gold to rally, but the precious metal could not sustain the early gains but closed in the green.

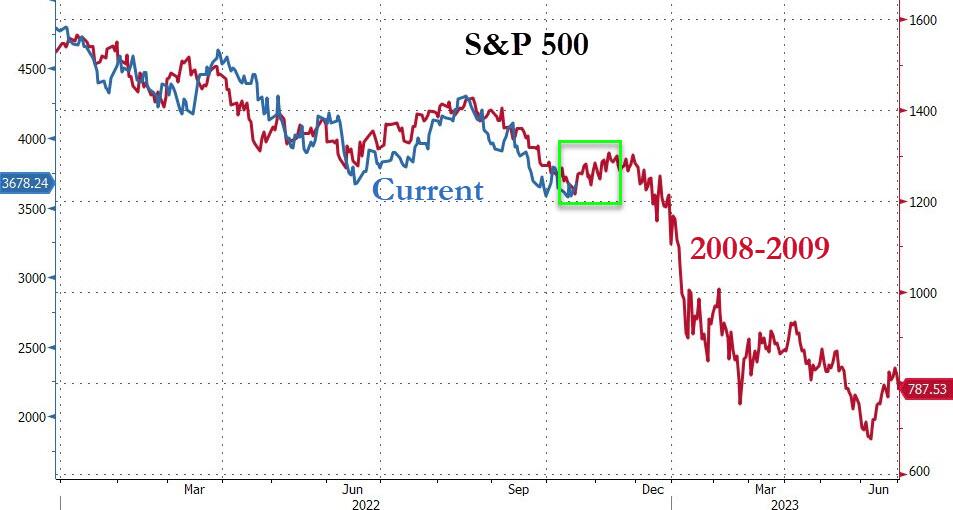

Can this bounce be prolonged? ZeroHedge concluded that it can—at least until the November FOMC meeting—that is if the 2008-2009 analog holds true.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}