Below, please find the latest High-Volume ETF Cutline report, which shows how far above or below their respective long-term trend lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s StatSheet and includes 312 High Volume ETFs, defined as those with an average daily volume of more than $5 million, of which currently 43 (last week 22) are hovering in bullish territory. The yellow line separates those ETFs that are positioned above their trend line (%M/A) from those that have dropped below it.

In case you are not familiar with some of the terminology used in the reports, please read the Glossary of Terms. If you missed the original post about the Cutline approach, you can read it here.

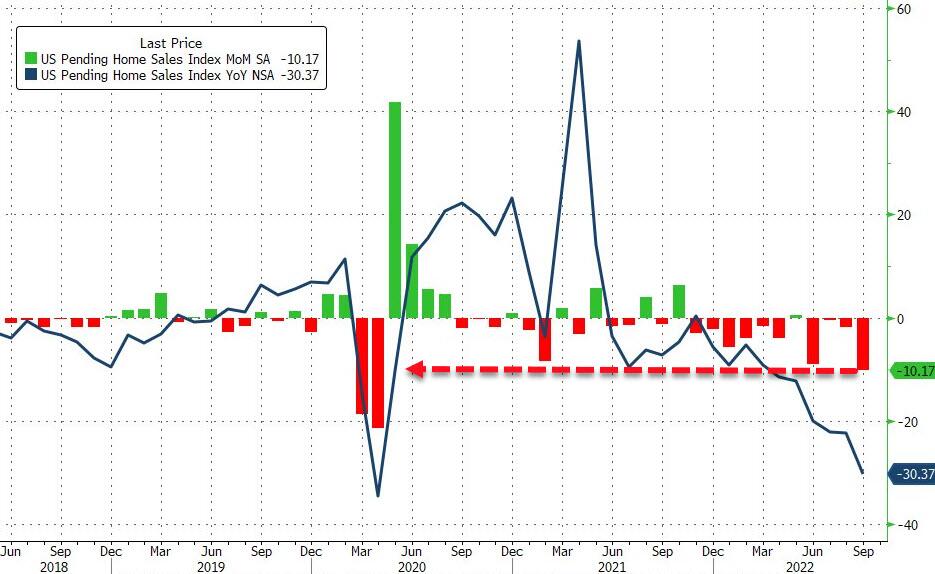

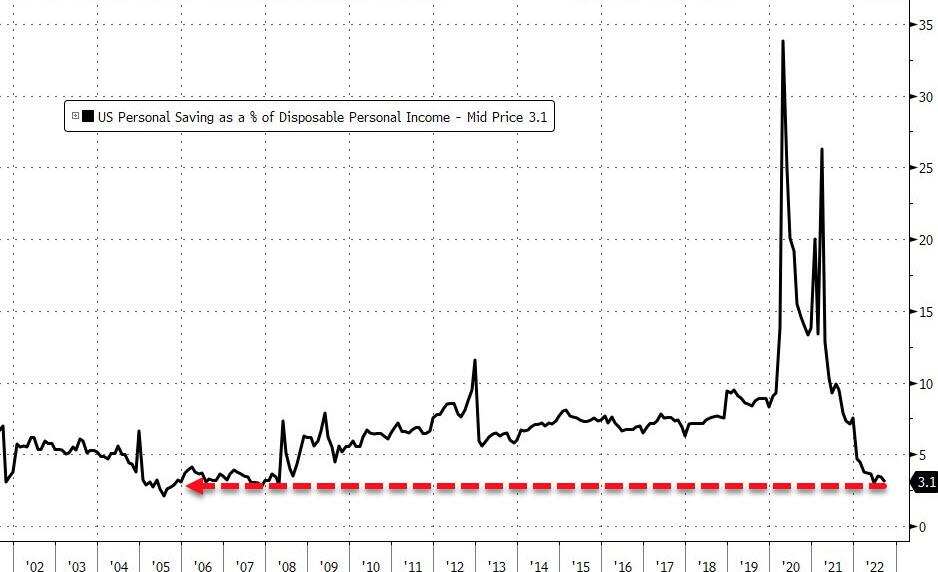

Looking at the tech wreck this week—during which heavyweights like Facebook and Amazon imploded, and the GDP allegedly grew by 2.6% in the 3rd quarter, while economic news was horrific, as inflation expectations jumped, US Pending Home Sales collapsed to their weakest since 2010, and the Americans’ Savings rate plunged to near record lows—you would have expected the markets to pull back in the face of such deteriorating economic conditions.

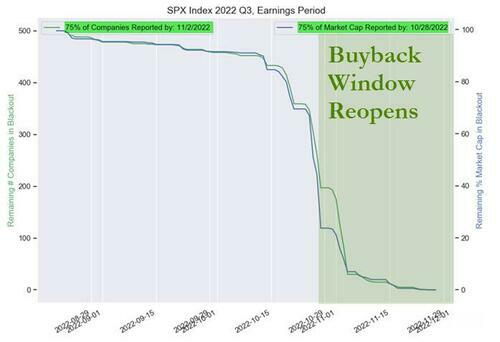

However, exactly the opposite occurred, as even the threat of nuclear war could not deter traders, algos and the corporate buy-back studs from ramping stocks higher, as October winds down with one more trading day to go.

Analyst MN Gordon of the EconomicPrism.com explained it this way as inflation, contrary to popular opinion, will continue to rear its ugly head:

The big Powell pivot that’s now being telegraphed for the December Federal Open Market Committee (FOMC) meeting has nothing to do with the arrival of a much-anticipated deceleration in the rate of inflation.

Nope, it’s all politics to juice the stock market in the runup to election day.

Given that, and the now much lower hoped forterminal rate expectations, as a potential Fed pivot is supposed to be imminent, I can see that the recognition, after the mid-term elections, that the inflation monster has not yet been brought under control, could provide the markets with another surprise, namely a “rug pull” that will collapse stocks again to new YTD lows.

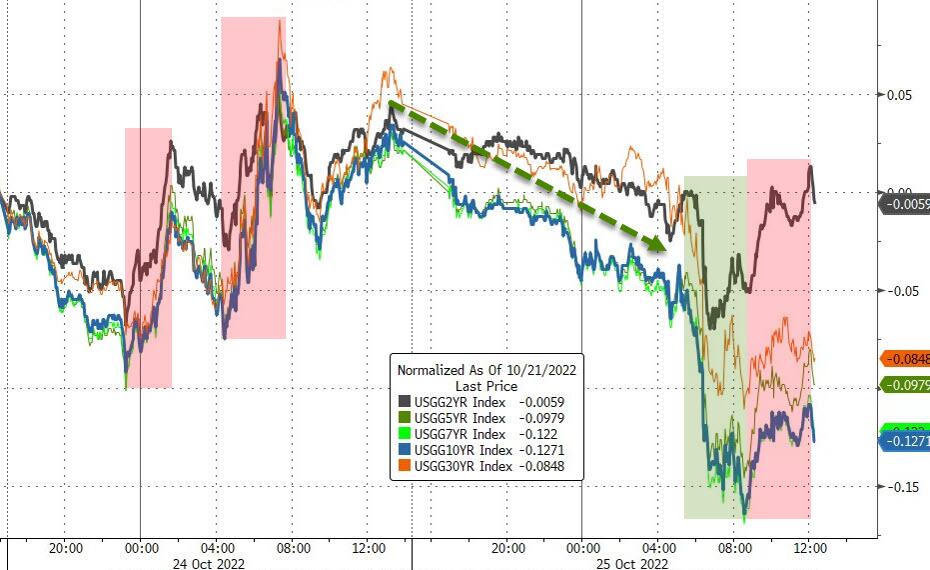

Bond yields popped for the day but were lower for the week, with the 10-year recovering its 4% level after having dropped below it yesterday. Despite recovering during the past two sessions, the US Dollar ended the week to the downside.

This upside charge in equities was not lost on my Trend Tracking Index (TTI-section 3), which surged this week and has now reached a point that is only -2.49% below its long-term trend line. Should this Ramp-A-Thon continue, we could find ourselves back in the market shortly.

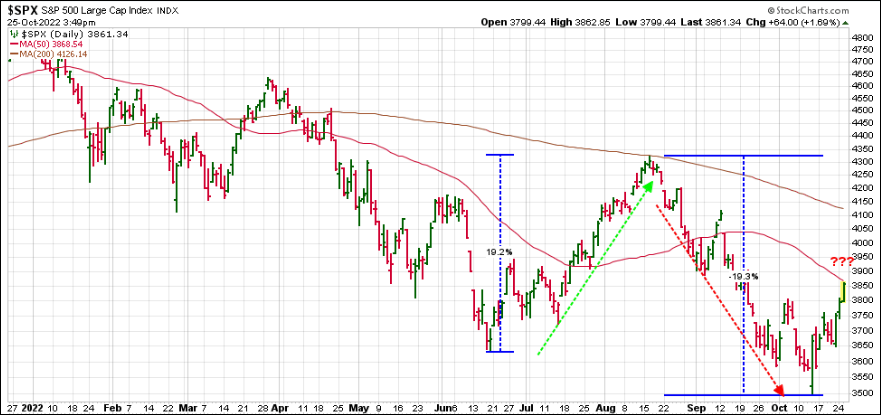

Speaking against a robust upside continuation is the surprisingly so far spot-on historical analog to 2008/2009. Look at this chart, which may be more accurate than a 1,000 words.

ETF Data updated through Thursday, October 27, 2022

Methodology/Use of this StatSheet:

1. From the universe of over 1,800 ETFs, I have selected only those with a trading volume of over $5 million per day (HV ETFs), so that liquidity and a small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and 2), are made based on the respective TTI and its position either above or below its long-term M/A (Moving Average). A crossing of the trend line from below accompanied by some staying power above constitutes a “Buy” signal. Conversely, a clear break below the line constitutes a “Sell” signal. Additionally, I use a 12% trailing stop loss on all positions in these categories to control downside risk.

3. All other investment arenas do not have a TTI and should be traded based on the position of the individual ETF relative to its own respective trend line (%M/A). That’s why those signals are referred to as a “Selective Buy.” In other words, if an ETF crosses its own trendline to the upside, a “Buy” signal is generated. Here too, I recommend trailing sell stop of 12%, or less, depending on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

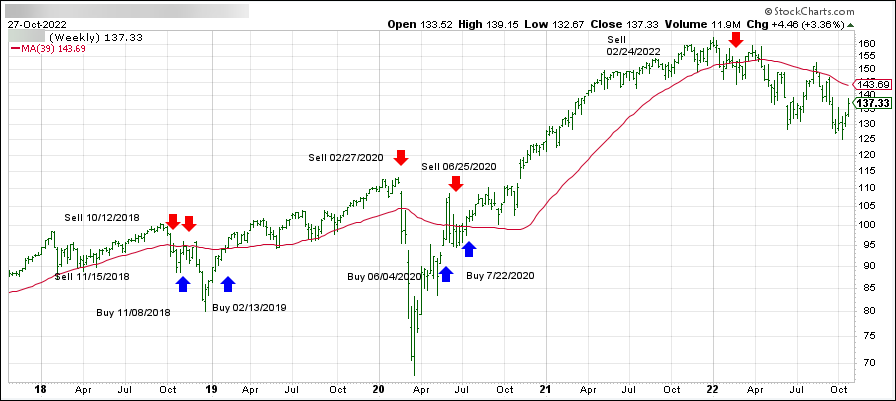

1. DOMESTIC EQUITY ETFs: SELL — since 02/24/2022

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) has broken below its long-term trend line (red) by -4.67% and remains in “SELL” mode.

Despite an early 300-point jump in the Dow, the major indexes were not able to hang on to that euphoric start, as the reality set in that all is not well with Big Tech. Both, Alphabet and Microsoft shares got hammered, with the former missing earnings expectations on the top and bottom lines, while the latter reported weaker than expected cloud revenue.

That ended a three-day winning streak, as traders tried to balance the overall earnings picture with what it might mean for future interest rate hikes. Optimism that the Fed will pivot, should things deteriorate more quickly, has been the main driver for this current rebound.

In terms of deterioration, housing appears take top billing when, after recent pessimistic reports, we learned today that New Home Sales plunged due to re-surging mortgage rates thereby wiping out the August “hope” bounce.

Looking at the big picture, we witnessed violent swings with the Chinese Yuan exploding higher, bond yields plunging, stocks pumping and dumping, the dollar getting clubbed, while crude oil and gold ramped higher.

And to be included in today’s confusion, former NY Fed President Bill Dudley called for the Fed to be hawkish for longer:

Emphasizing “longer” rather than “higher” has some advantages. It presumably reduces the risk of a hard landing: If monetary policy is somewhat tight, but not very tight, activity and employment should slow gradually. It gives Fed officials time to assess the consequences of their efforts, recognizing that monetary policy entails uncertainty and affects the economy with long and variable lags.

That said, the downside risks are significant. Because less-aggressive tightening takes longer to bring down inflation, it might allow inflationary expectations to become unanchored – a dynamic that only even-higher interest rates could counteract.

That, of course, puts a crimp in the dovish storyline that a pivot could be on the horizon, but then again, nobody can be sure about anything. We could see more follow through to the upside or a huge crash—take your pick.

Plunging bond yields provided the perfect background to keep the bear market rally intact for the third day, a scenario we’ve witnessed several times this year. The largest drop and subsequent rebound happened in June, when the S&P 500 exploded off its bottom by 19.2% only to shift in reverse and surrender all gains:

While we may see a similar pattern play out again, the big unknown here is the Fed and its “anticipated” (not announced) intentions. If in fact they pause or pivot, we will likely see this bear market rally turn into a new bull market, which will then get us trend trackers back into equities.

Jumping in any time prior to our Trend Tracking Index (TTI) breaking its trend line to the upside is like trying to catch a falling knife, and we’ve witnessed how that idea ended up in nothing but financial pain on six occasions this year. As tempting as it may be, it’s wiser to let a bullish trend establish itself before pushing the Buy button.

The fact that earnings estimates have been reduced by analysts allowed companies to fare better than anticipated, thereby proving some support for the current rally, despite decreases in 2023 forecasts. And, of course, a short-squeeze was activated and contributed to the melt-up.

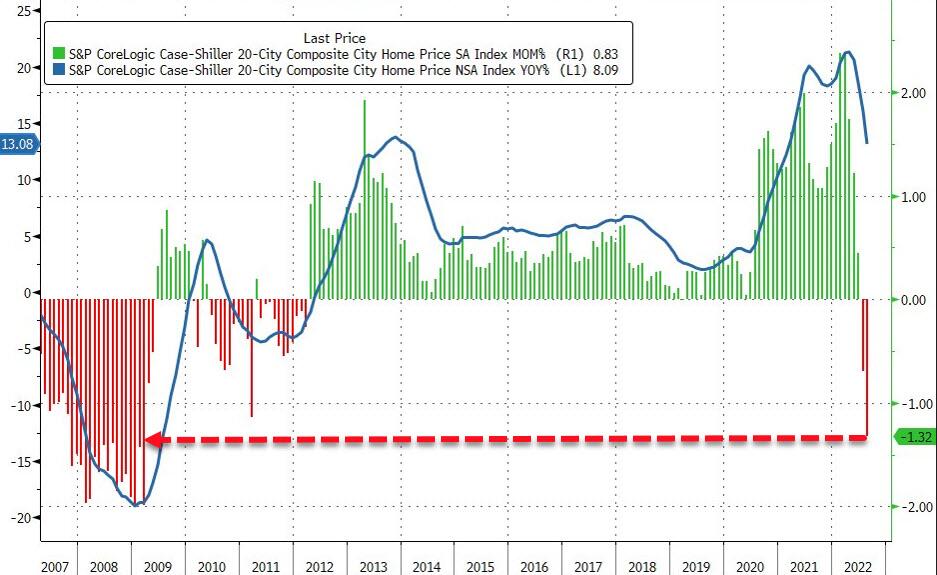

On the economic side, we learned that Consumer Sentiment tumbled with current conditions crashing to 18-month lows, as ZeroHedge reported. Real estate news was just as ugly, as home prices plunged the most since 2009, but fear not, any bad news was seen as good news for the markets—at least for this day.

The US Dollar dropped to 3-week lows, which benefited gold, and the precious metal gained some ground but has a way to go get back to its old highs.

In terms of earnings, the big boys are on deck with Alphabet and Microsoft due out this afternoon, which is followed by Amazon’s and Apple’s report cards on Thursday.

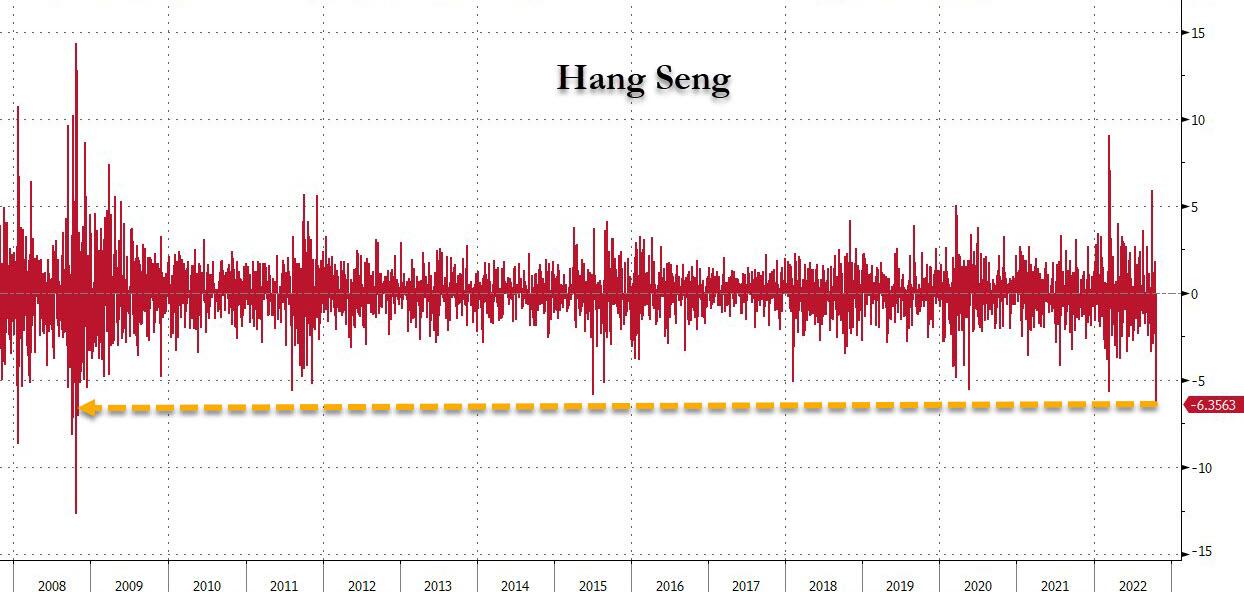

Despite a rollercoaster ride in the futures market overnight, and a plunge in the Chinese stock market of -6.4%, its largest one-day drop since 2008, US sentiment remained positive after the opening bell rang.

It’s all about earnings and forward guidance this week, with 46% of S&P members reporting. However, inflation data and bond yields will always be on centerstage with traders now “whispering” that the Fed might be stepping off the gas pedal regarding their hiking pace with a “pause” to be hopefully on deck.

All the above is not based on facts, but merely wishful thinking, but so far it has had the desired effect of keeping the bullish theme alive. We have seen this pattern numerous times this year, but all prior attempts eventually died on the vine, and new yearly lows were subsequently made. Only time will tell if this “melt up” has enough legs to eventually generate a new “Buy” signal (section 3).

Economically, things looked pretty dire as Manufactu9irng and Service PMIs, tumbled into contraction, as ZeroHedge reported:

US Manufacturing 49.9 (contraction), below 51.0 exp and down from 52.0 prior

US Services 46.6 (contraction), below 49.5 exp and down from 49.3 prior.

Of course, nobody calls it a recession anymore, so we’re in tune with the fact that bad news is good news for the markets, as the eventual “Powell Pivot” hope (from hawkish to dovish) is all that matters. Go figure…

Even higher bond yields could not keep equities down, as the 10-year swung wildly and closed at 4.255%, near its recent highs. The US Dollar meandered aimlessly and so did Gold, with neither having much to show for in the end.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}