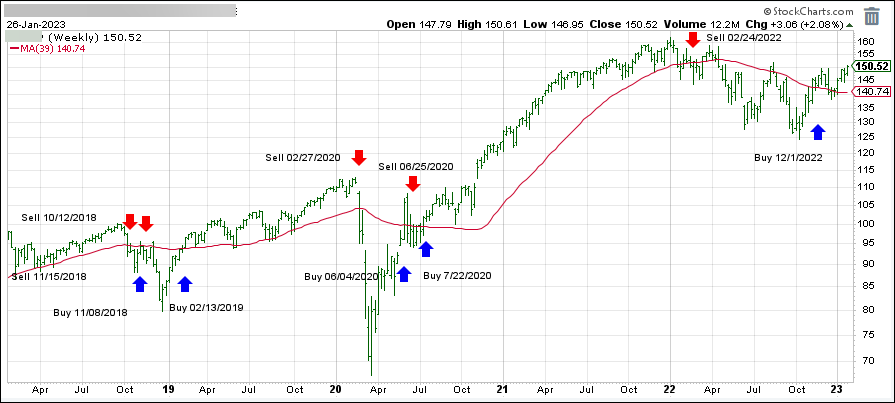

- Moving the markets

Anxiety reigned supreme ahead of the Fed’s decision on interest rates, with the markets having priced in a meager 0.25% hike. That is despite the countless announcements by a host of speakers that “higher rates for longer” are the current policy theme, yet traders have battled the Fed every step of the way.

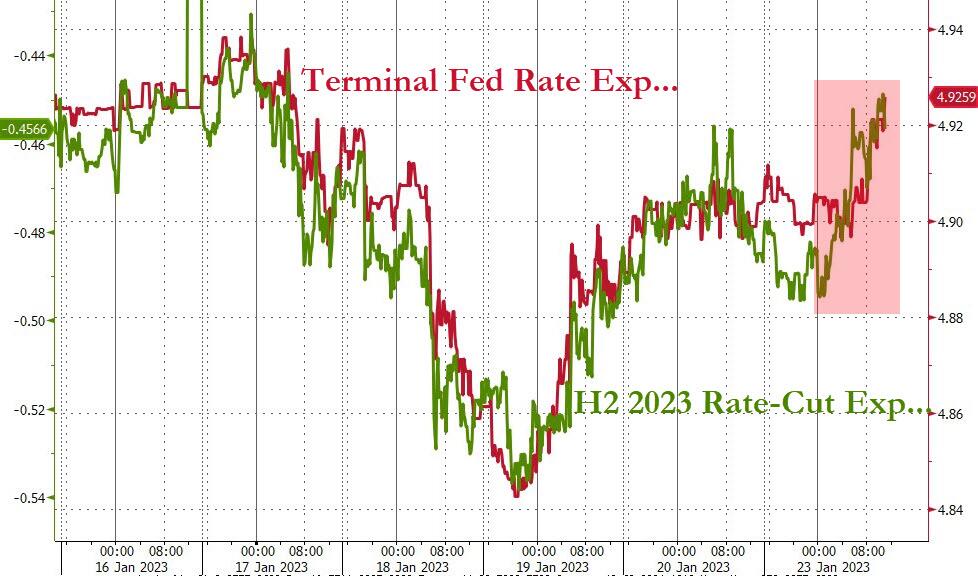

It’s likely that the Fed eventually will reverse its tightening schedule, but it’s questionable whether that point in time has been reached already. Wednesday’s release of their decision will shed some light on where they are at with their policies. Will the hawkishness continue? The H2 2023 Rate Cut Expectations seem to indicate so.

Adding to the nervousness in the markets will be the continued earnings barrage with some 20% of the S&P members releasing their report cards this week, including some of the tech giants like Apple, Amazon, Meta, and Alphabet.

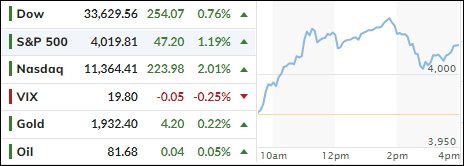

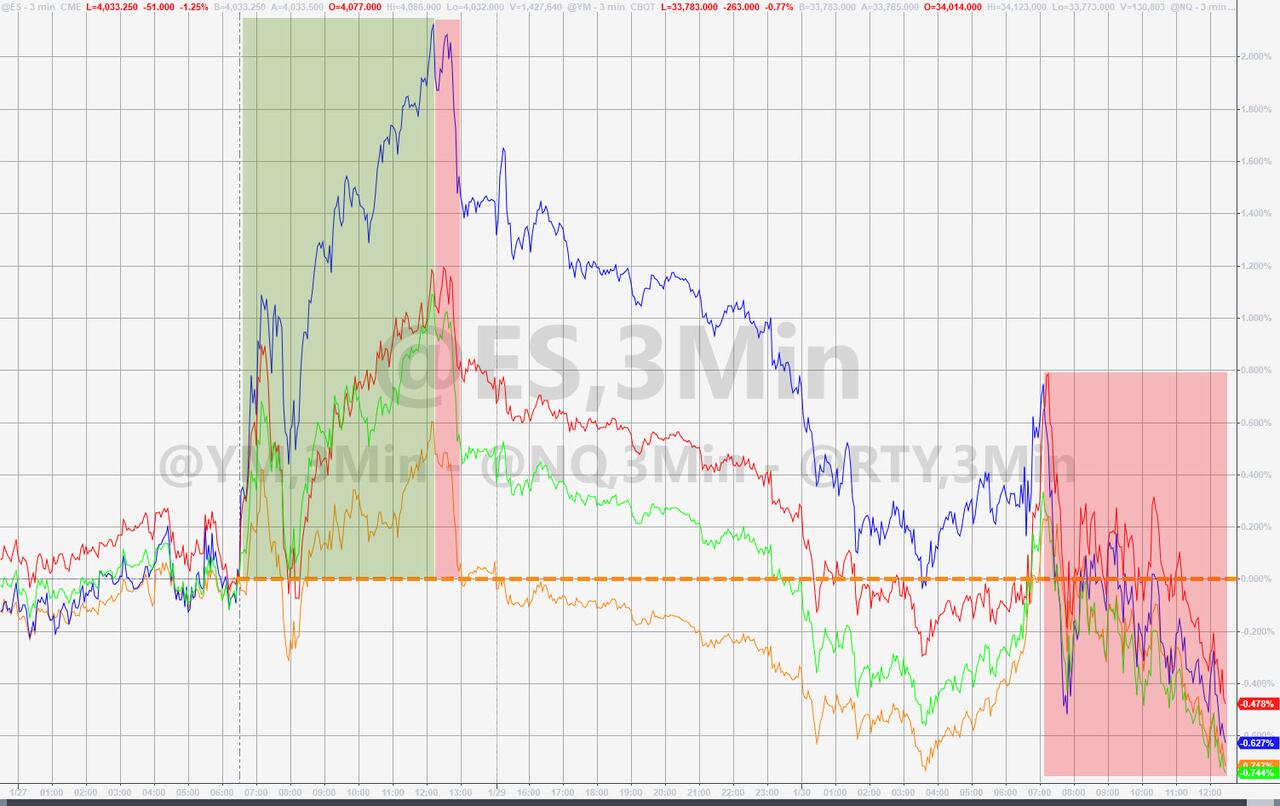

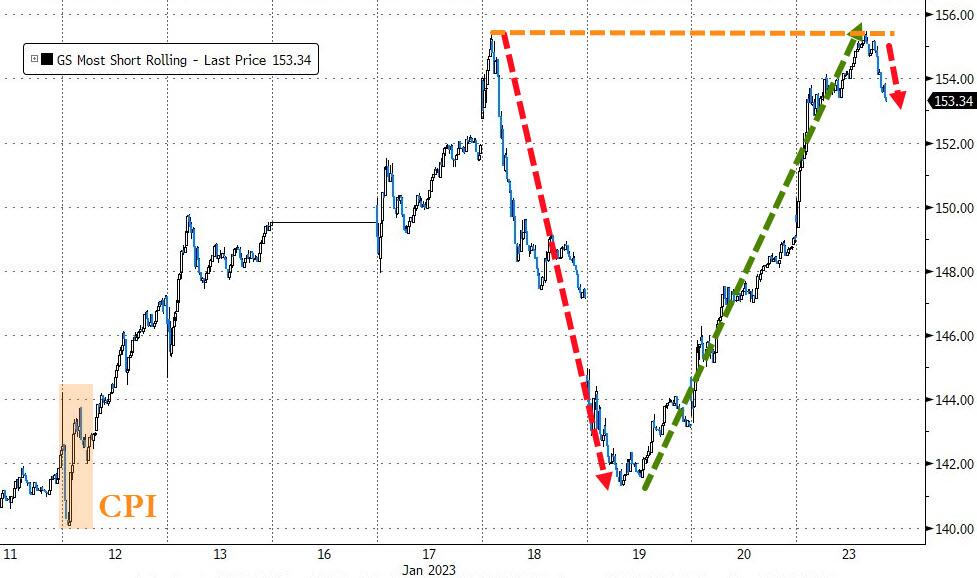

At session’s end, today’s reality check erased all of Friday’s gains and then some, as the short squeeze ran out of ammo again.

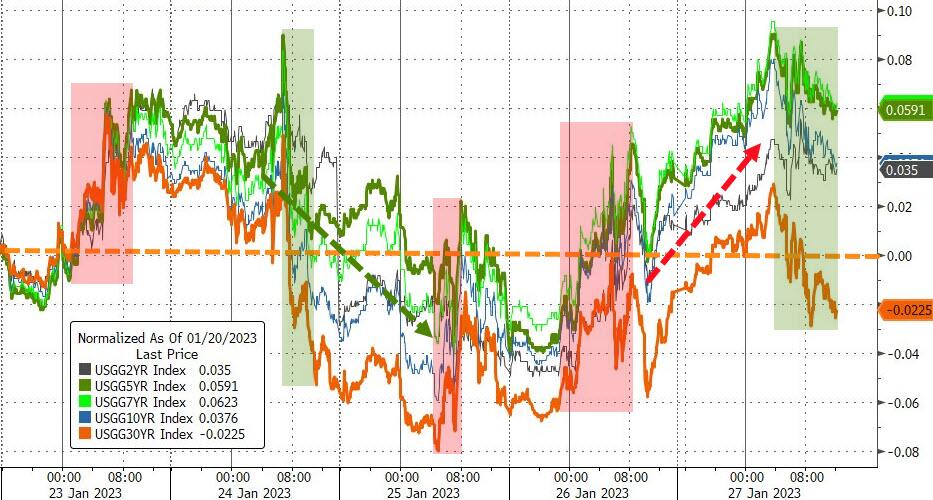

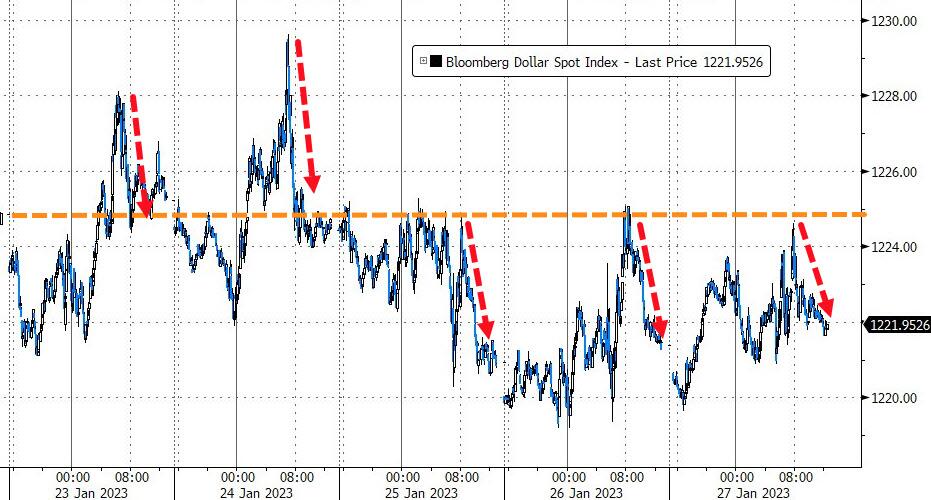

Bond yields rose due to uncertainty about the Fed’s policy decision, the US Dollar dipped and ripped, which caused Gold to drift modestly lower yet remain firmly anchored above its $1,900 level.

We might see more of the same tomorrow.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}