- Moving the markets

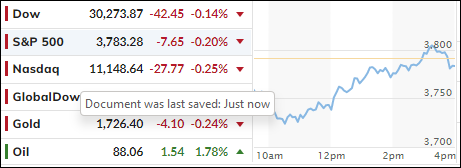

Overnight weakness, followed by an early dump, with the Dow dropping some 400 points, was reversed as bullish sentiment prevailed causing traders and algos to pull the major indexes out of a hole and back to within striking distance of their respective unchanged lines.

{kind=link}

After two days of strong gains, the widely followed S&P 500 closed lower by a moderate amount, as the index gave back -0.19%, which was a nice recovery off the session’s lows. However, the S&P was not able to hang on to its 3,800 level, which it had crossed intra-day.

{kind=link}

Today’s action reflected a moment of pause and deliberation as to how durable the current advance might be. After all, this rebound was based on nothing but hope that the Fed will make, or be forced to, a dovish pivot. So far, there have been no indications.

Bloomberg elaborated on the turnaround:

One giant options transaction may have sparked the S&P 500’s bounce on Wednesday, according to Wells Fargo & Co. The trade, which involved buying and selling call options tied to the index at a cost of around $31 million, probably helped fuel a recovery that saw the benchmark gauge erase a 1.8% decline.

A better-than-expected jump in jobs, as per ADP, showed an increase of 208k jobs vs. an expected 200k, but more important will be Friday’s non-farm payroll report.

{kind=link}

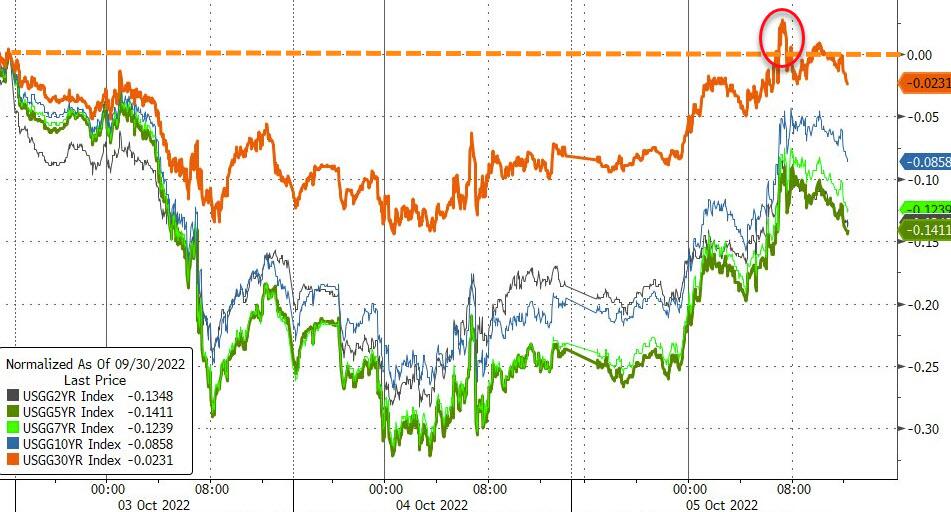

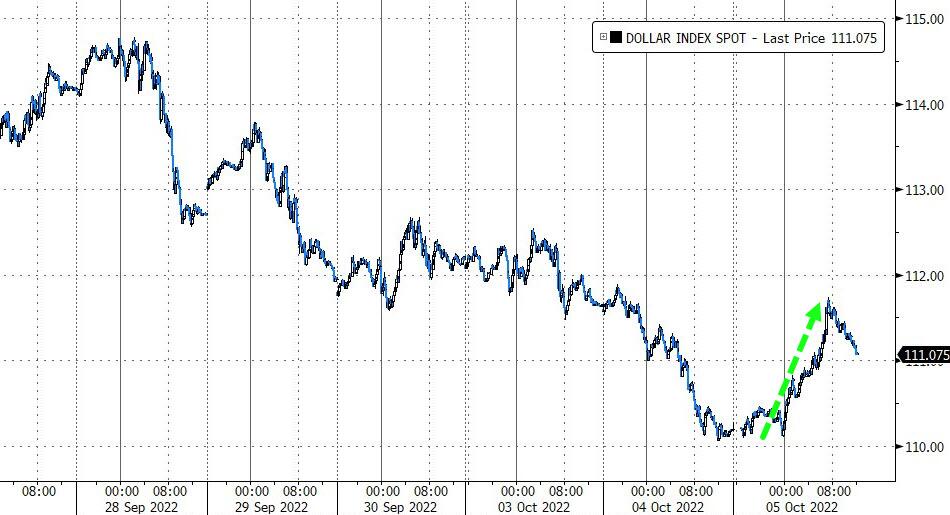

Bond yields jumped but did not affect equities negatively, despite the 10-year climbing 12bps to end the session at 3.754%. The US dollar, after a 5-day down streak, showed signs of life again and rebounded almost 1%.

{kind=link}

{kind=link}

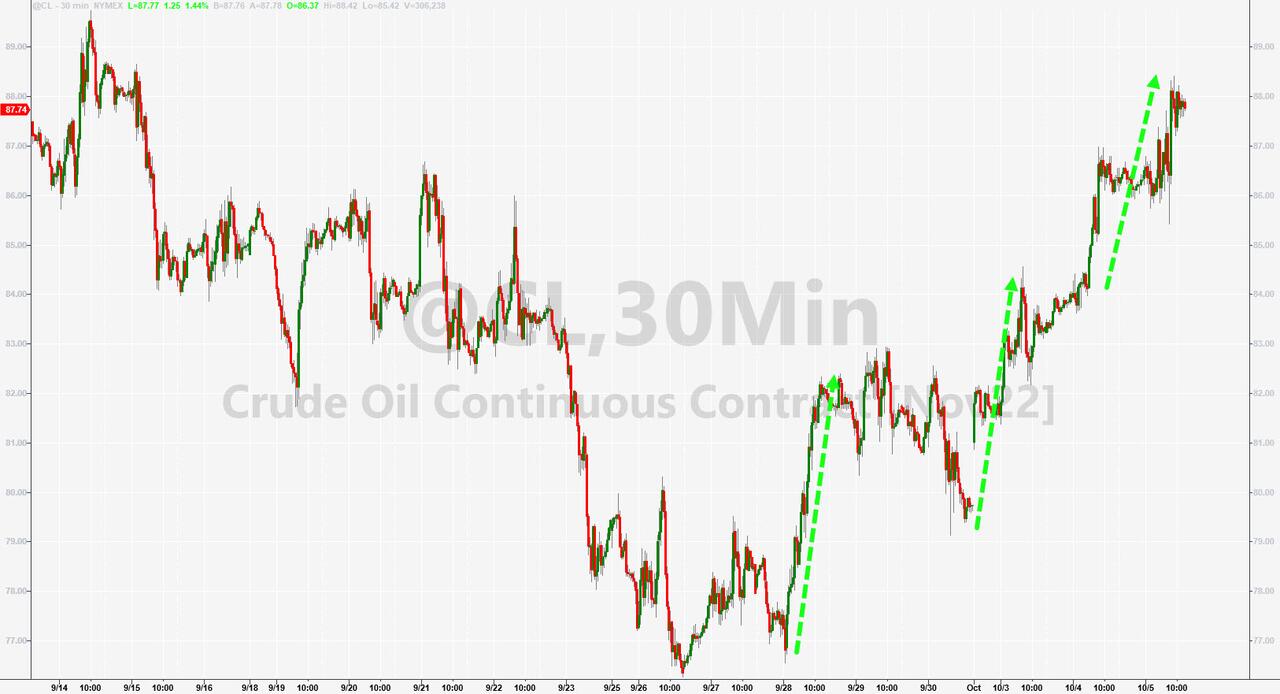

Crude Oil jumped as well, due OPEC now being in the process of reducing daily production. Ouch!

{kind=link}

Gold bounced erratically but managed to defend its $1,700 level.

{kind=link}

As ZeroHedge noted, financial conditions have eased notably over the last 3 days, which is not what the Fed wants to see. My conclusion is that they are not ready to pivot anytime in the very near future.

{kind=link}

2. ETFs in the Spotlight

In case you missed the announcement and description of this section, you can read it here again.

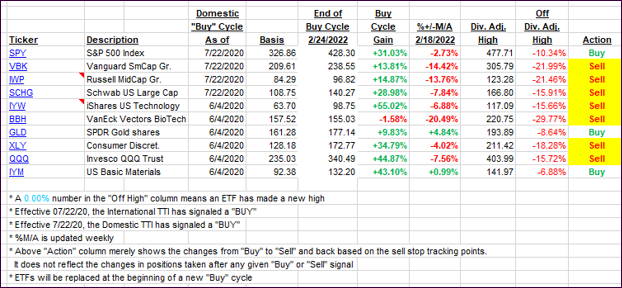

It features some of the 10 broadly diversified domestic and sector ETFs from my HighVolume list as posted every Saturday. Furthermore, they are screened for the lowest MaxDD% number meaning they have been showing better resistance to temporary sell offs than all others over the past year.

The below table simply demonstrates the magnitude with which these ETFs are fluctuating above or below their respective individual trend lines (%+/-M/A). A break below, represented by a negative number, shows weakness, while a break above, represented by a positive percentage, shows strength.

For hundreds of ETF choices, be sure to reference Thursday’s StatSheet.

For this closed-out domestic “Buy” cycle (2/24/2022), here’s how some of our candidates have fared. Keep in mind that our Domestic Trend Tracking Index (TTI) signaled a “Sell” on that date, which overrode the existing “Buys” shown for SPY and IYM:

Click image to enlarge.

Again, the %+/-M/A column above shows the position of the various ETFs in relation to their respective long-term trend lines, while the trailing sell stops are being tracked in the “Off High” column. The “Action” column will signal a “Sell” once the -12% point has been taken out in the “Off High” column, which has replaced the prior -8% to -10% limits.

3. Trend Tracking Indexes (TTIs)

Our TTIs pulled back a tad, as the major indexes did not manage a green close.

This is how we closed 10/05/2022:

Domestic TTI: -7.70% below its M/A (prior close -7.34%)—Sell signal effective 02/24/2022.

International TTI: -12.68% below its M/A (prior close -12.07%)—Sell signal effective 03/08/2022.

Disclosure: I am obliged to inform you that I, as well as my advisory clients, own some of the ETFs listed in the above table. Furthermore, they do not represent a specific investment recommendation for you, they merely show which ETFs from the universe I track are falling within the specified guidelines.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

Contact Ulli