- Moving the markets

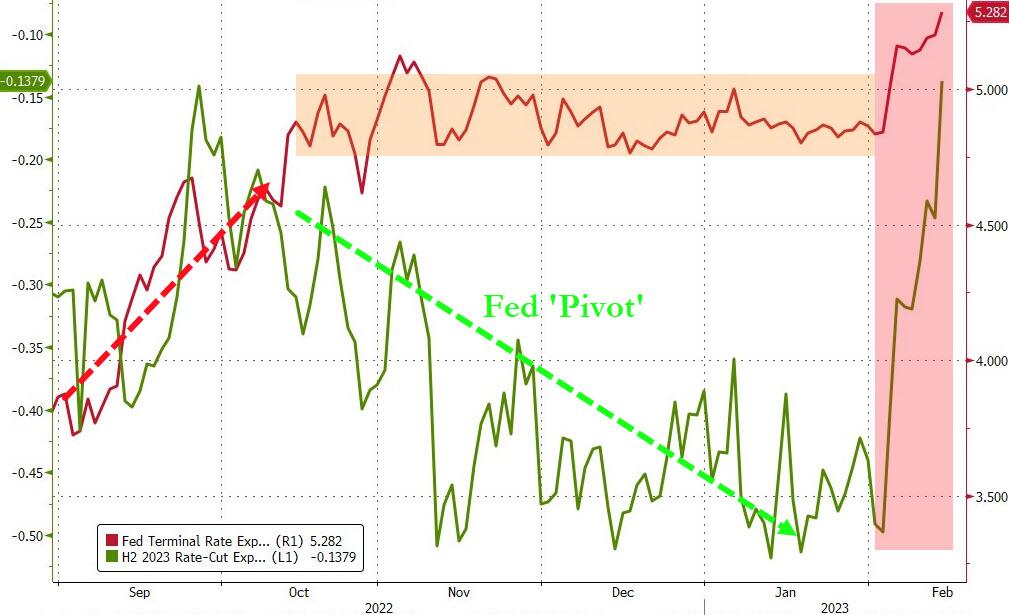

It appeared that traders and algos alike finally were confronted with a reality check, namely that interest rates will not retreat and likely move considerably higher. This has been the consistent theme of the Fed and its mouthpieces, and I have repeatedly suggested that front running and hopeful thinking does not change underlying facts.

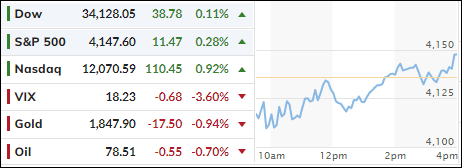

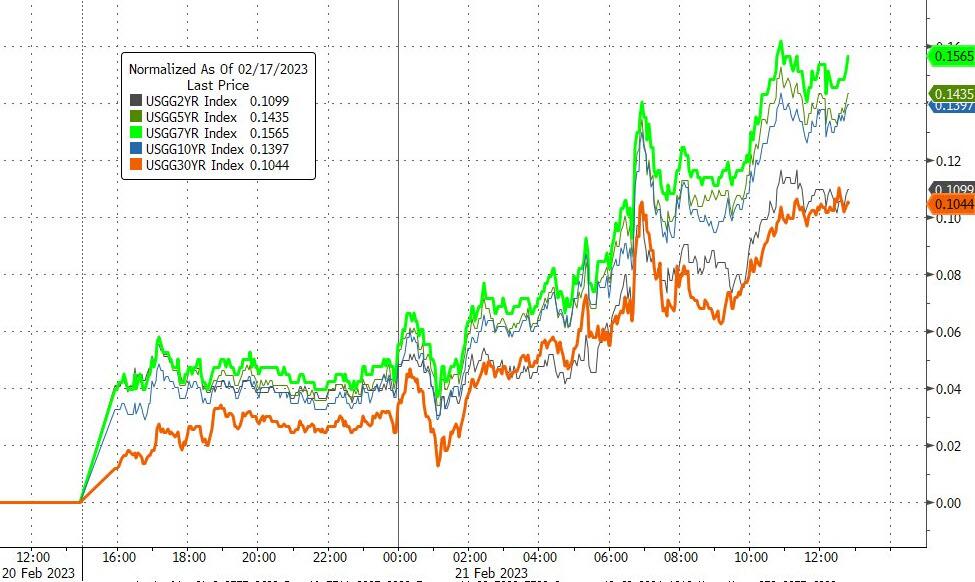

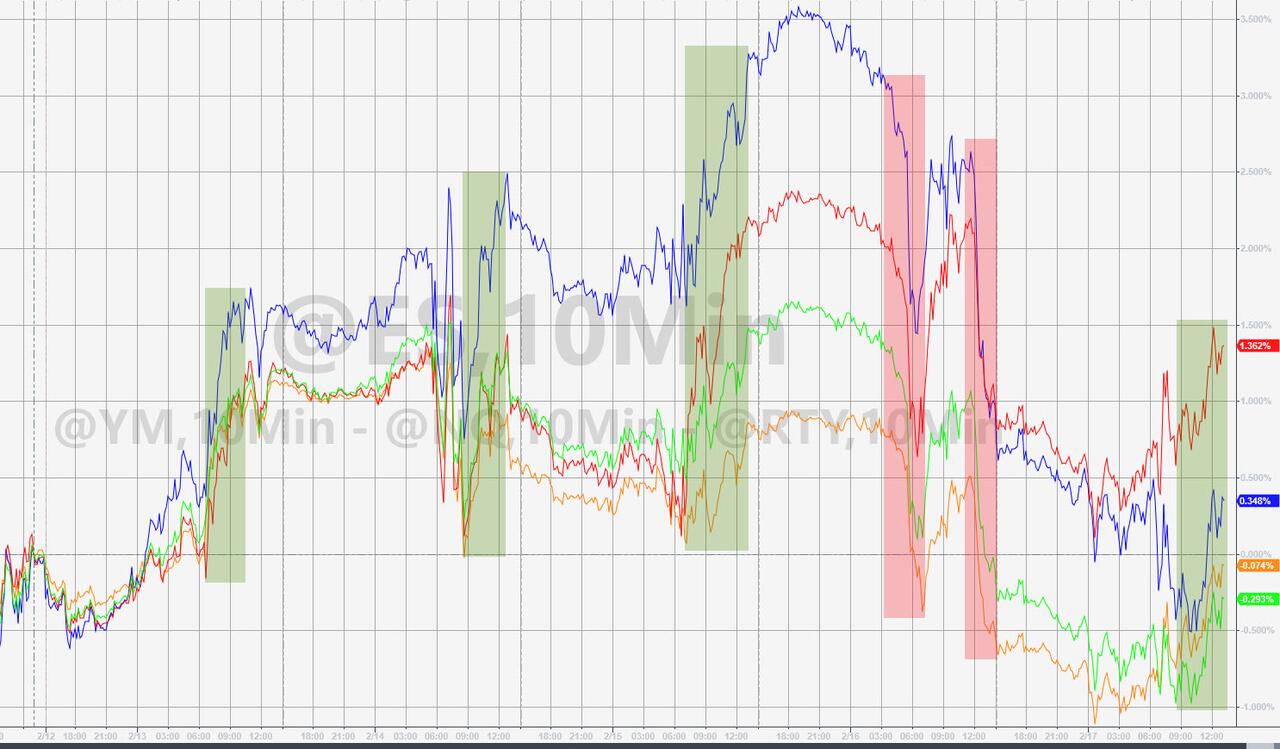

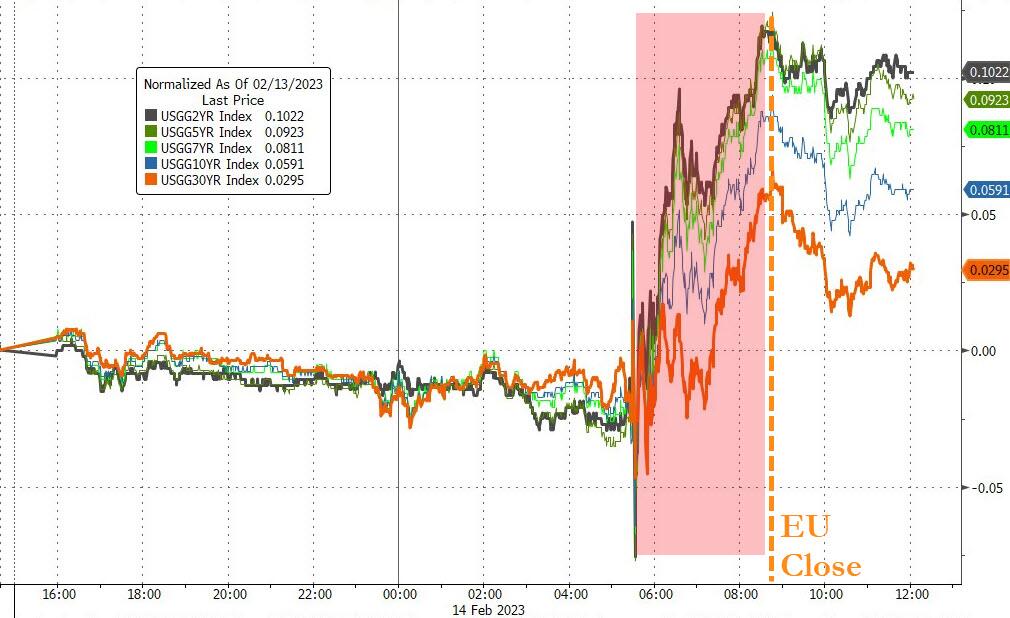

That’s what we saw today, as the markets experienced a phenomenon that I call “hammer time,” meaning that all asset classes were slammed and there was no place to hide. Especially not bonds, as all yields rose sharply with the 10-year propelling to its highest level this year (3.96%).

The widely held bond ETF TLT dropped over 2% on the day and has now lost some 6.3% for the month of February. So much for the perceived security of this asset class in times of turmoil.

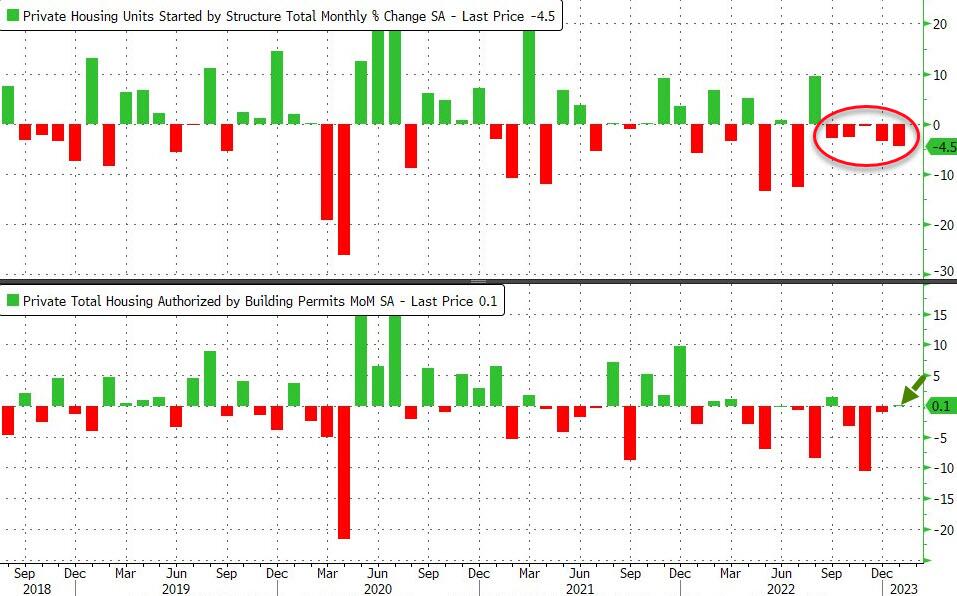

Surging rates obviously pressured the bullish theme, while retail earnings rang alarm bells regarding the health of the consumer and his ability to keep spending. After all, some 67% of all economic activity is consumer generated. News in the econ arena was poor, with Walmart issuing disappointing guidance, while Existing Home Sales unexpectedly declined in January and collapsed YoY by 37%. Ouch!

The Fed’s terminal rate exploded to over 5.3% and the usual dovish voices, counting on any rate cuts in 2023, disappeared mysteriously. This means, for the time being, that the consistently promoted “Fed pivot” narrative has died.

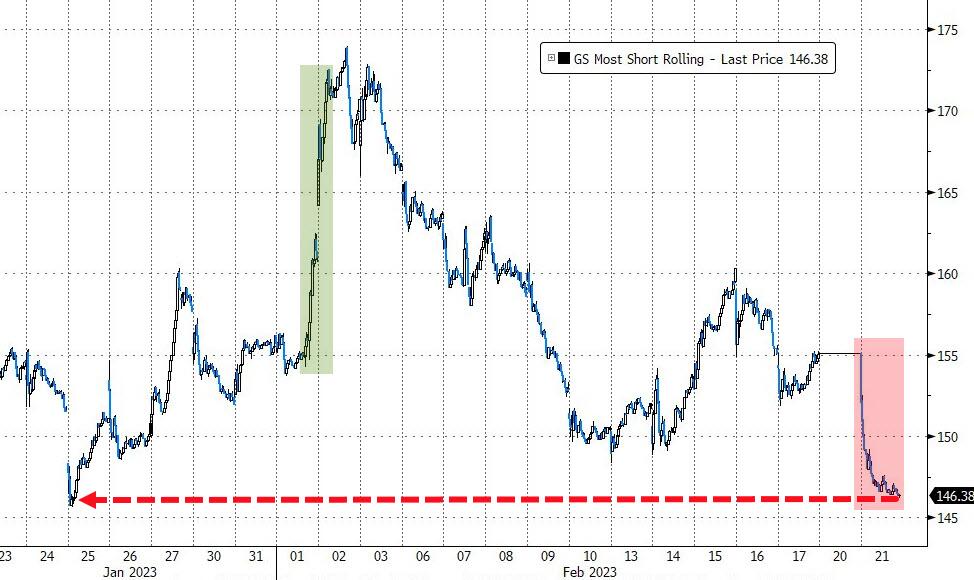

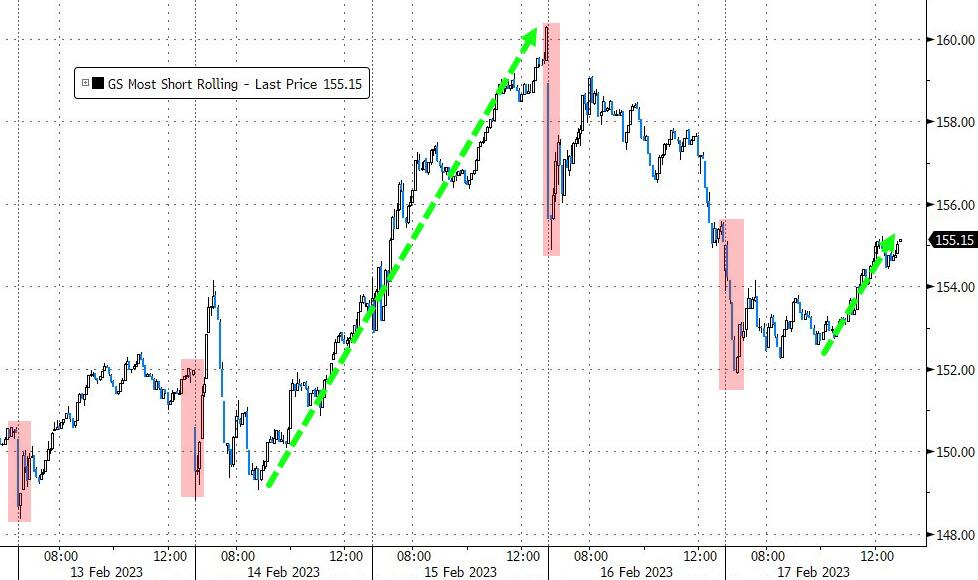

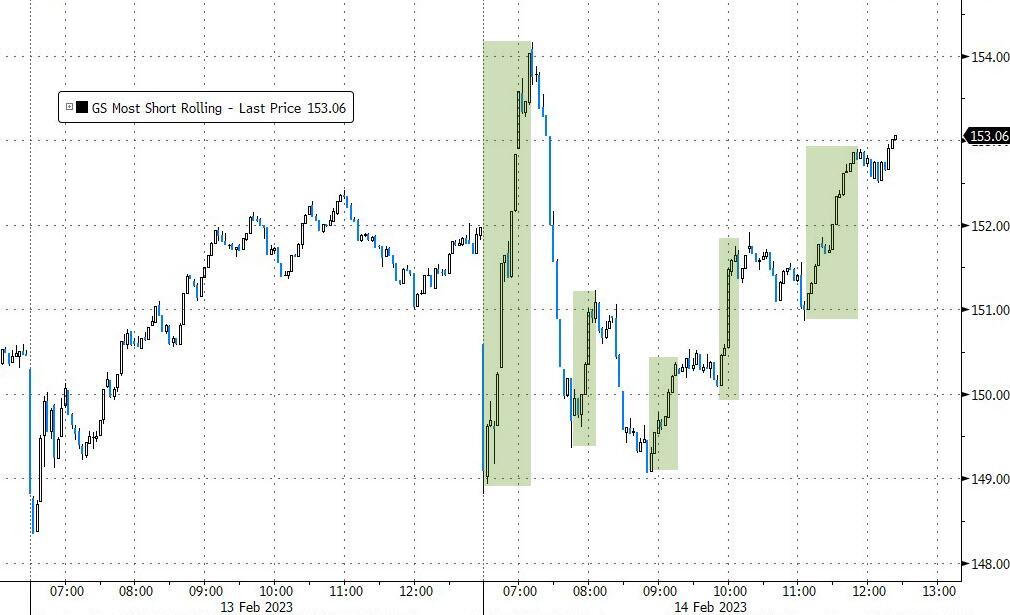

The most shorted stocks were clubbed like a baby seal, according to ZeroHedge, and saw their biggest single day decline since June 2022.

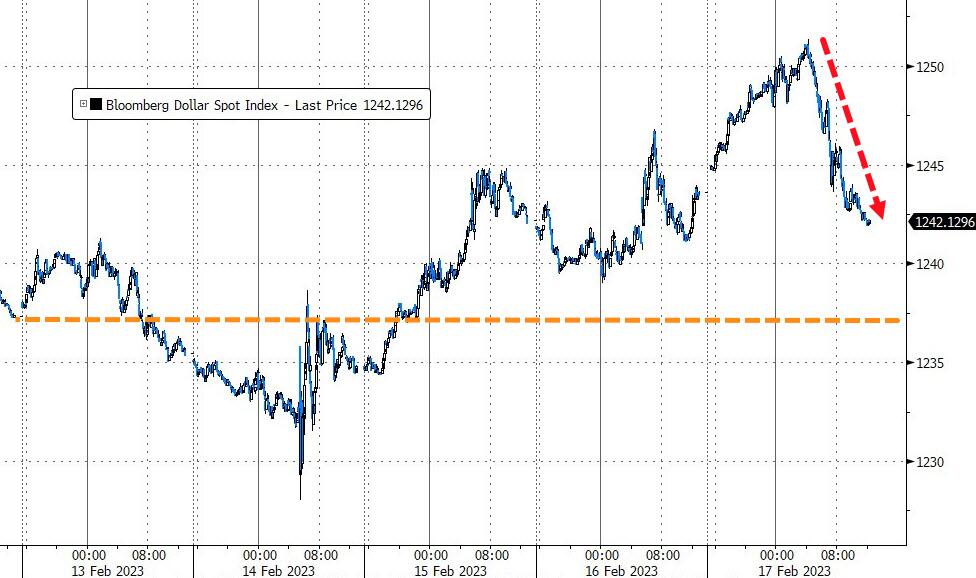

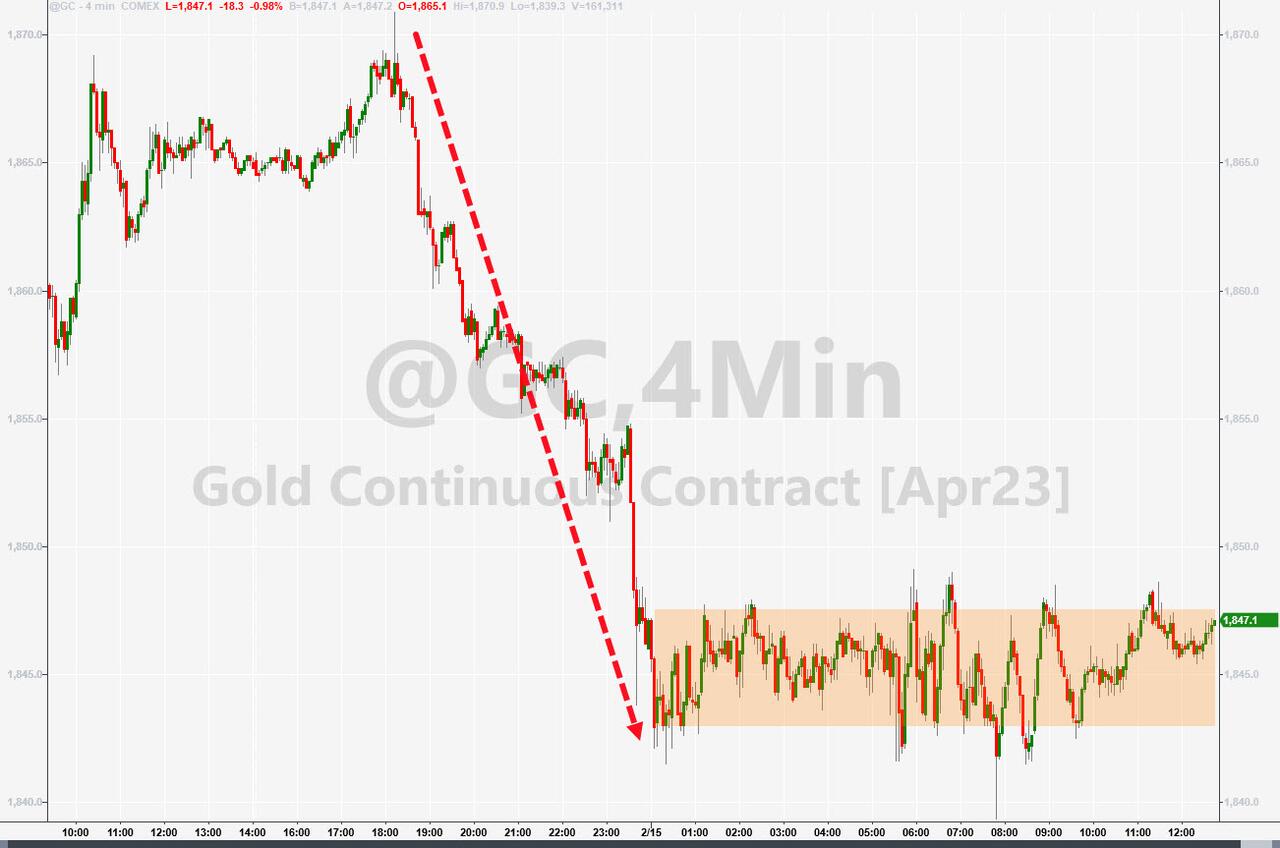

The US Dollar gained a little on the day, causing Gold to drop a tad.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}