- Moving the market

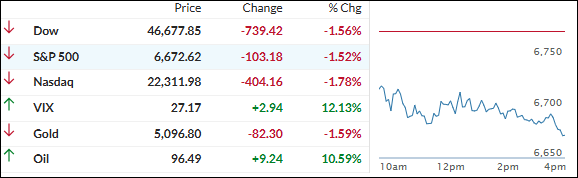

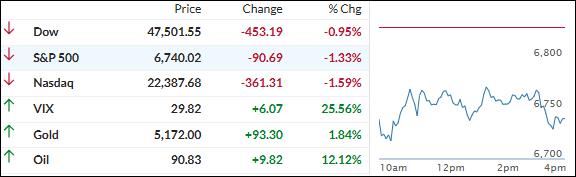

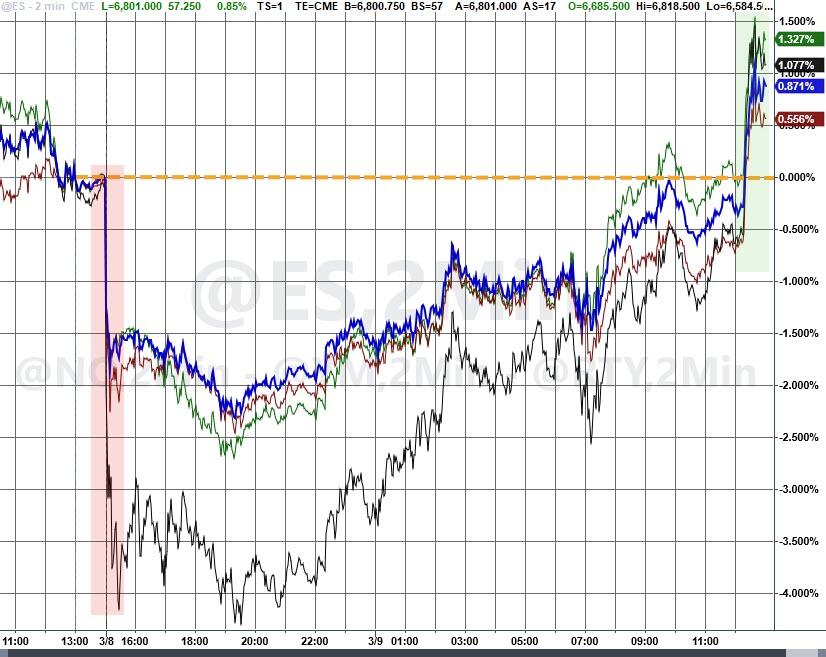

The major indexes opened under pressure and stayed there for most of the day, as oil prices kept surging on supply disruption fears from the ongoing U.S.-Iran war.

West Texas Intermediate crude jumped 9% to around $95 a barrel, while Brent climbed 8% to roughly $100.

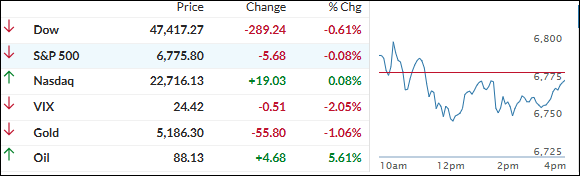

Iran’s new Supreme Leader Mojtaba Khamenei (appointed March 9) doubled down, saying the Strait of Hormuz should stay closed as a “tool to pressure the enemy.”

Energy Secretary Chris Wright added that the U.S. Navy isn’t ready yet to escort tankers through the Strait but should be by month’s end. Overnight, three more foreign vessels were hit in the Persian Gulf—traffic there is basically at a standstill.

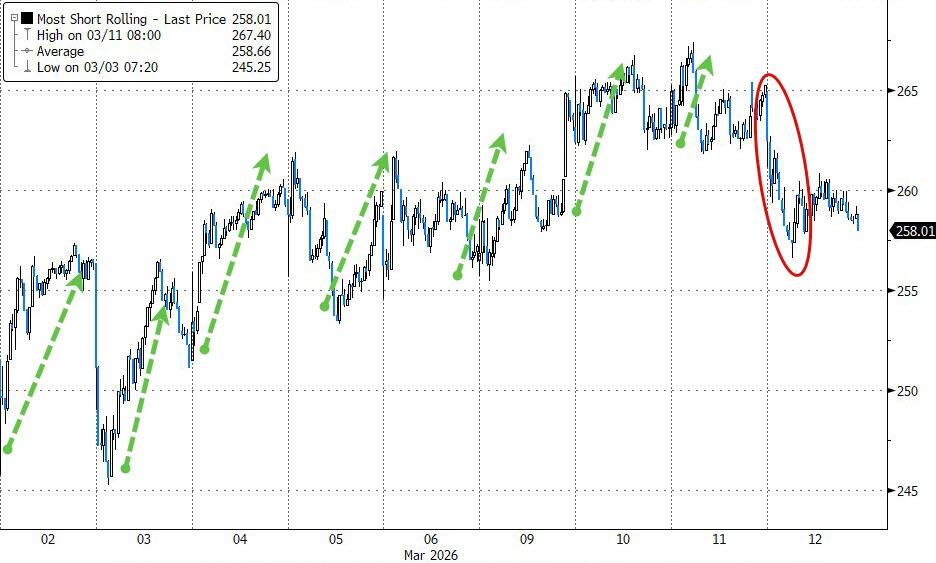

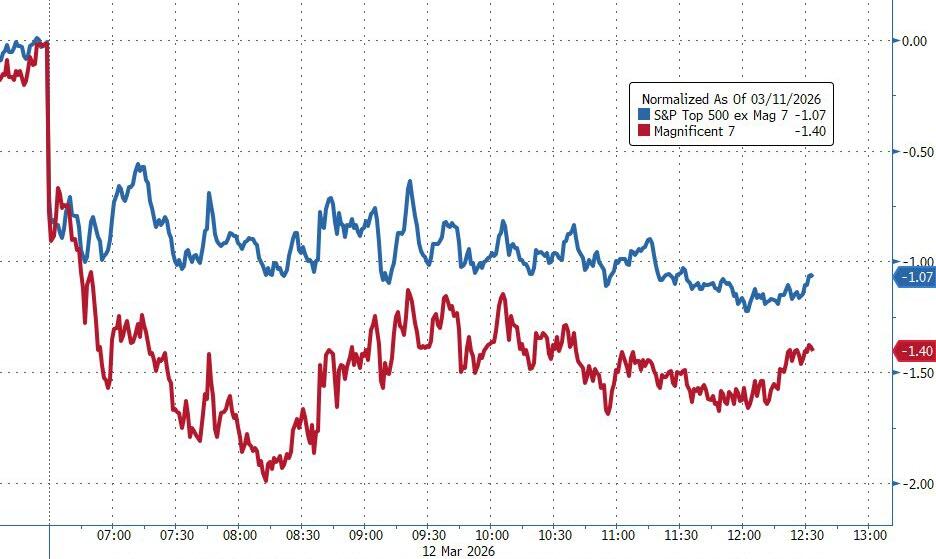

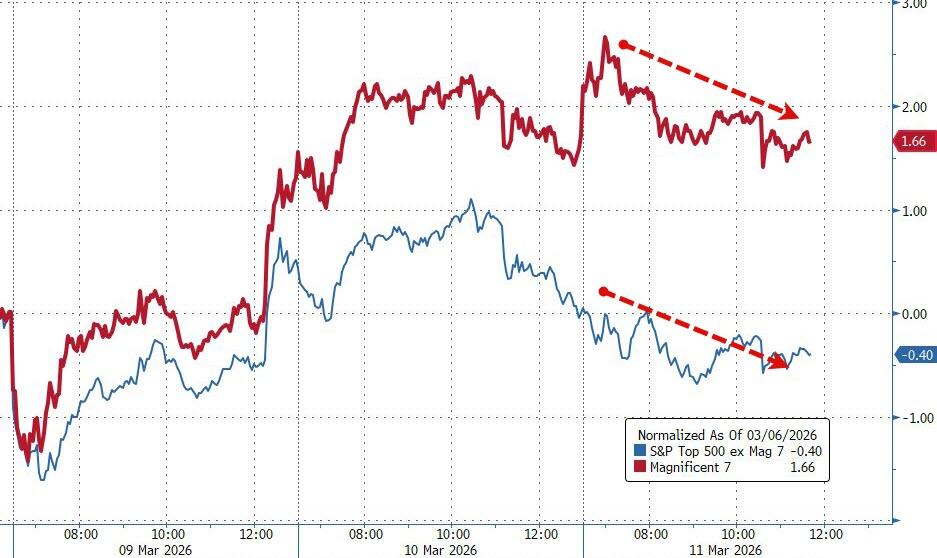

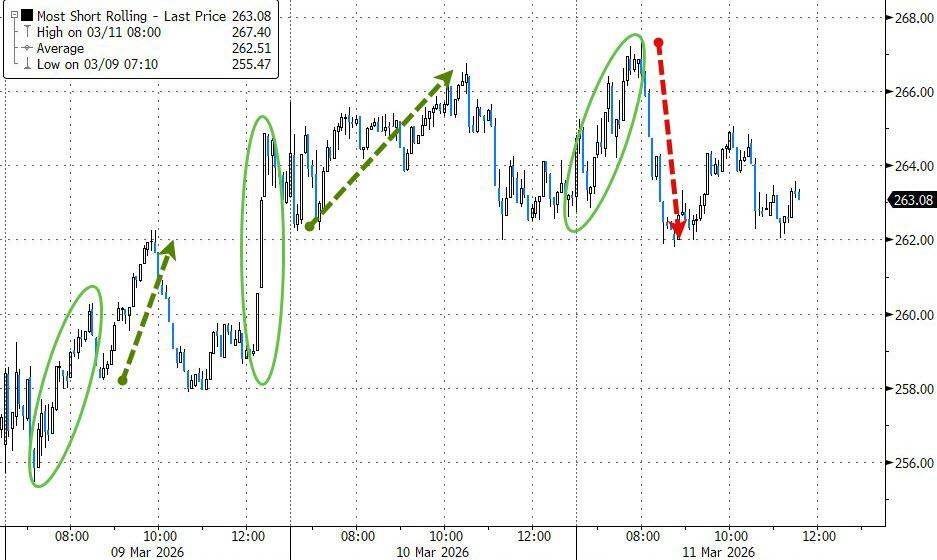

That oil spike fueled inflation worries and kept risk-off sentiment in charge. The S&P 500 and Dow closed sharply lower, with the Nasdaq also in the red. Small Caps were the day’s biggest loser (no short squeeze help), and the Mag 7 underperformed the rest of the S&P.

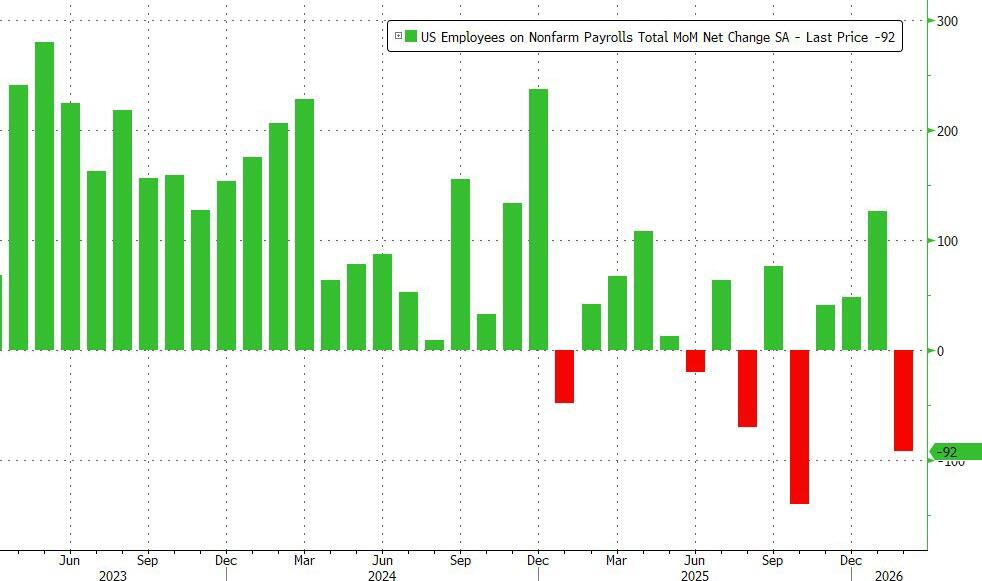

On the macro side, things were actually upbeat: January trade deficit narrowed, housing starts rose 7.2% (beating expectations), initial jobless claims edged down, and GDP tracking now sits at 3.3% annualized. But the oil and war headlines drowned it all out.

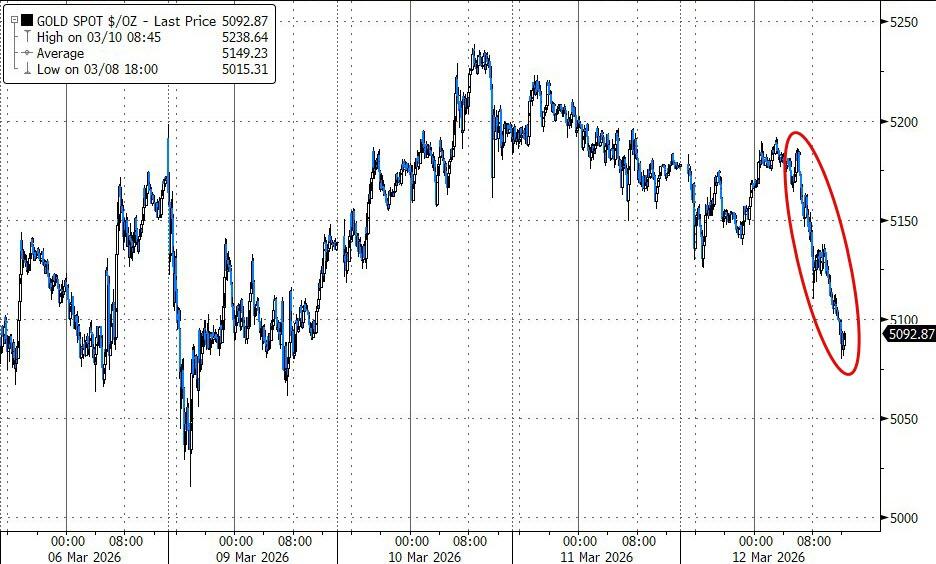

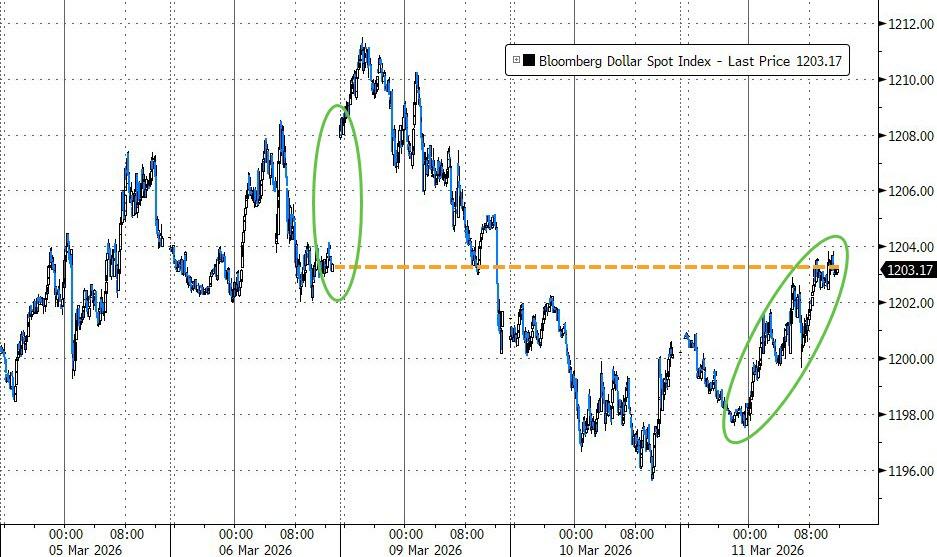

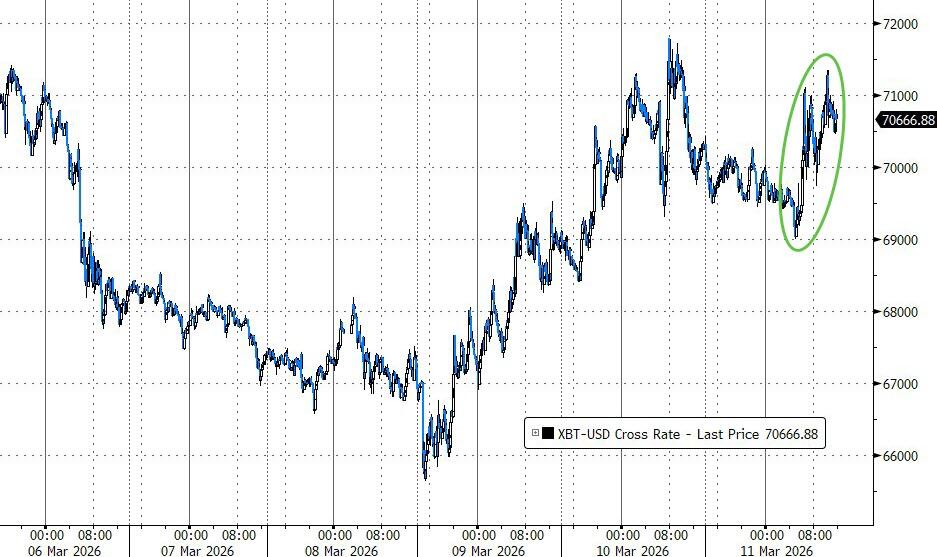

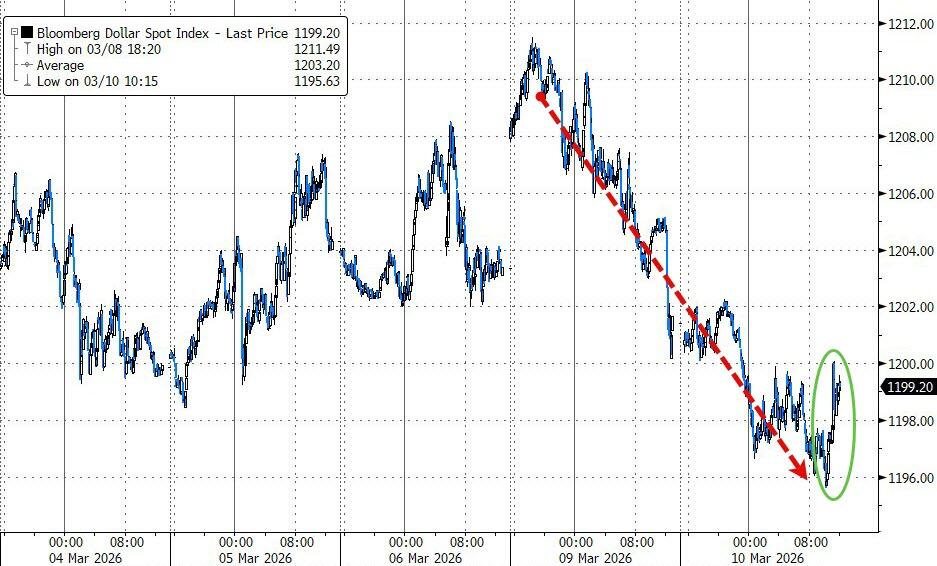

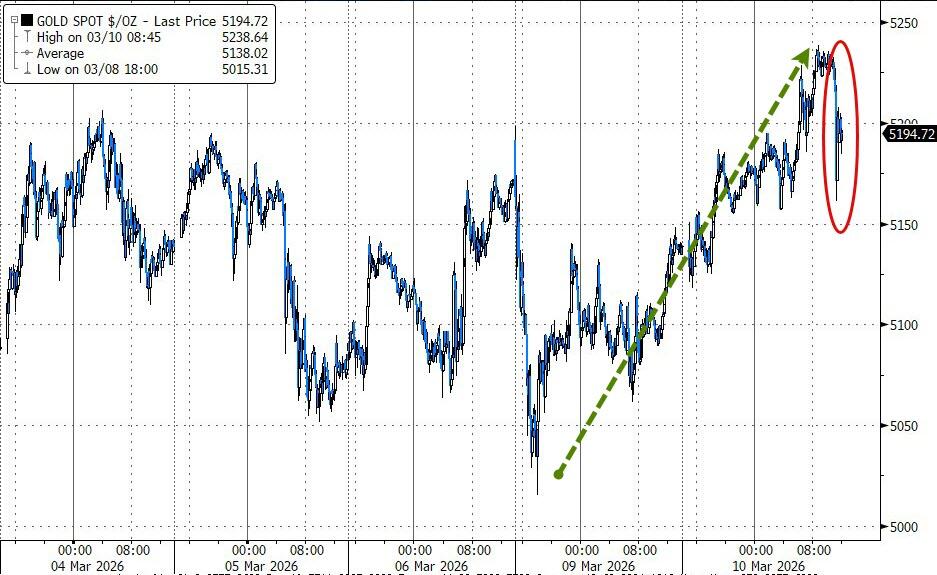

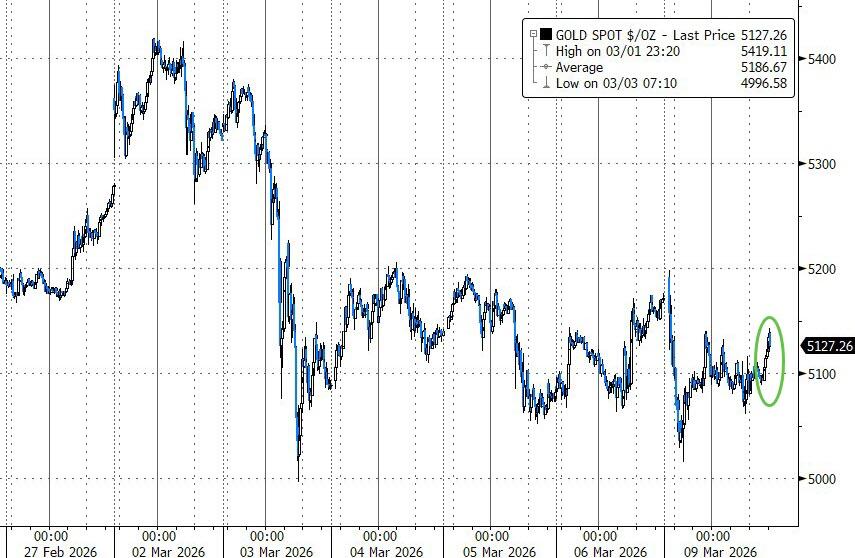

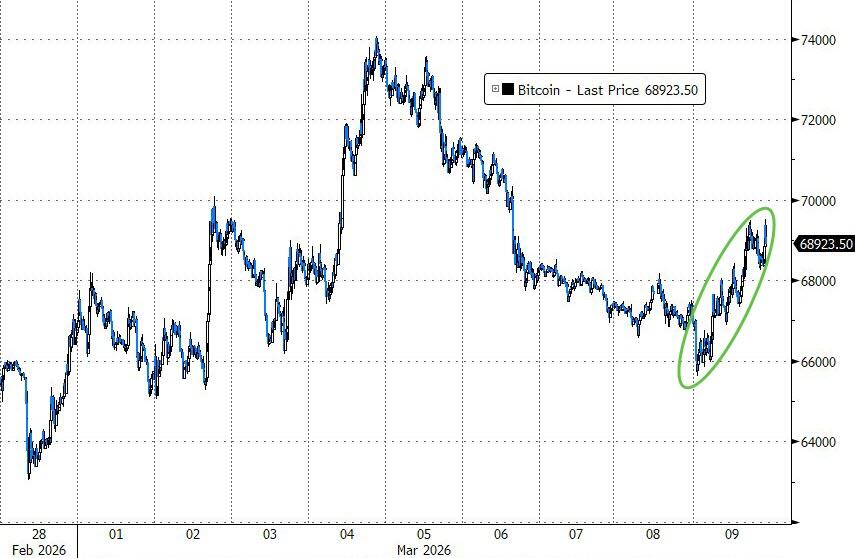

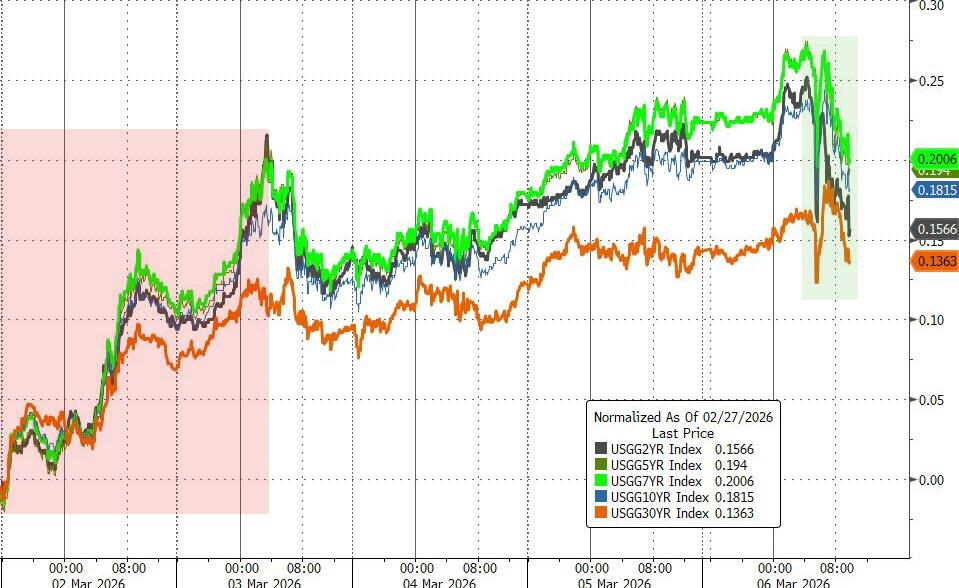

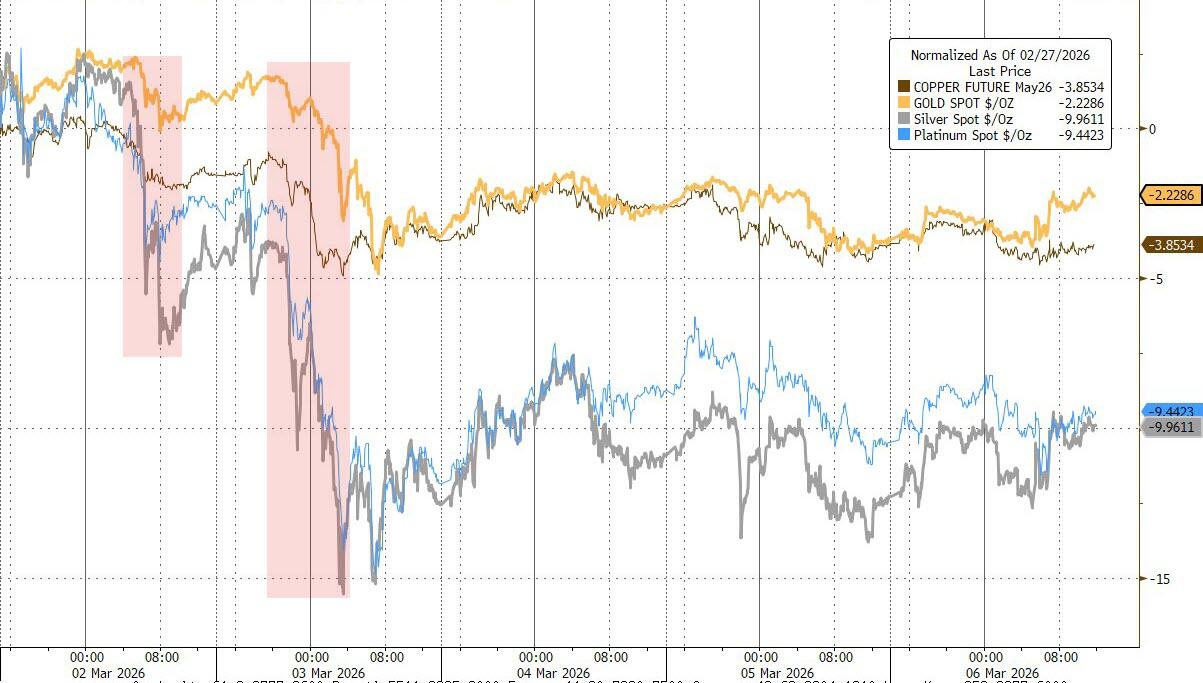

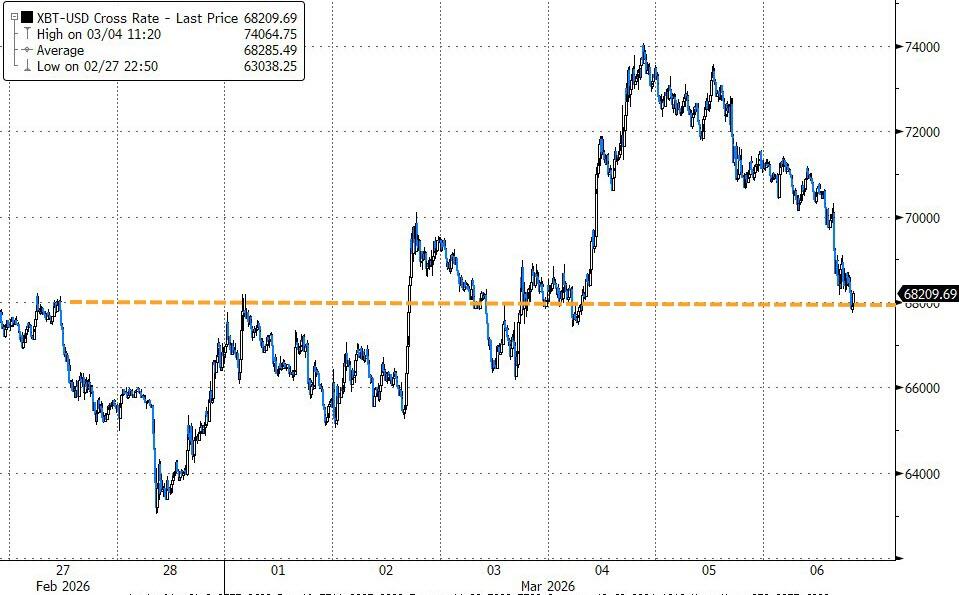

Bond yields rose across the board (rate-cut expectations collapsed), the dollar rallied for the second day in a row, gold broke back below $5,100, and Bitcoin stayed coiled in a tight range around $70,000—breakout coming, but direction unclear.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}